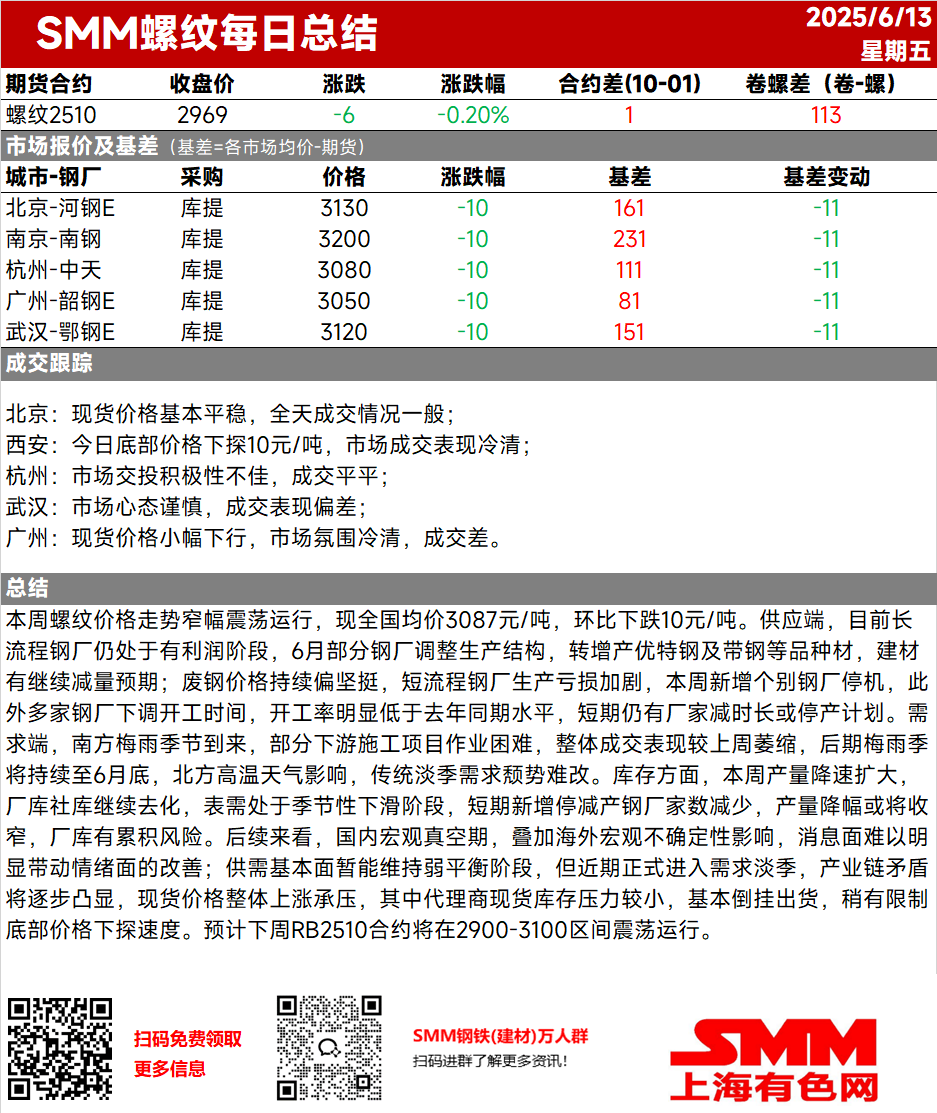

This week, rebar prices fluctuated rangebound, with the current nationwide average price at 3,087 yuan/mt, down 10 yuan/mt MoM. On the supply side, blast furnace steel mills are still in a profitable phase. In June, some steel mills adjusted their production structures, shifting towards increasing output of specialty and high-quality steel, as well as strip steel and other varieties, with expectations of further reductions in construction steel production. Steel scrap prices have remained firm, exacerbating production losses at EAF steel mills. This week, individual steel mills have halted operations, and several others have reduced their operating hours, with operating rates significantly lower than the same period last year. In the short term, there are still plans for some mills to reduce operating hours or suspend production. On the demand side, the arrival of the plum rain season in south China has made it difficult for some downstream construction projects to operate, with overall transaction volumes shrinking compared to last week. The plum rain season is expected to last until the end of June, and combined with the impact of high temperatures in north China, the traditional off-season demand slump is unlikely to change. In terms of inventory, the rate of production decline has widened this week, with in-plant and social inventories continuing to decrease. Apparent demand is in a seasonal decline phase. In the short term, the number of steel mills halting or reducing production has decreased, and the rate of production decline may narrow, with risks of in-plant inventory accumulation. Looking ahead, the domestic macro vacuum period, combined with the impact of overseas macro uncertainties, makes it difficult for news to significantly drive improvements in market sentiment. The supply and demand fundamentals can temporarily maintain a weak balance, but with the official entry into the demand off-season recently, contradictions in the industry chain will gradually become prominent. Overall, spot prices are under upward pressure. Among them, agents face relatively small inventory pressure for spot cargo, and are basically selling at a loss, slightly limiting the speed at which bottom prices decline. It is expected that the RB2510 contract will fluctuate rangebound within the 2,900-3,100 range next week.

![Ferrous Metals May Continue Trading at Elevated Levels in the Short Term [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/yBlDX20251217171747.jpg)