On June 9, data from the General Administration of Customs showed that China exported 10.578 million mt of steel in May 2025, up 1.1% MoM. From January to May, China's cumulative steel exports reached 48.469 million mt, up 8.9% YoY.

In May, China imported 481,000 mt of steel, down 7.9% MoM. From January to May, China's cumulative steel imports stood at 2.553 million mt, down 16.1% YoY.

• China's Steel Exports Surpass 10 Million mt for Three Consecutive Months

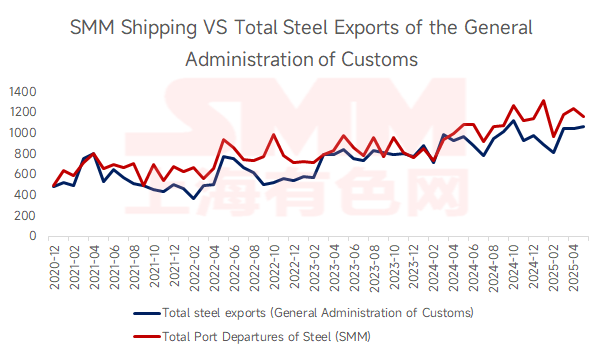

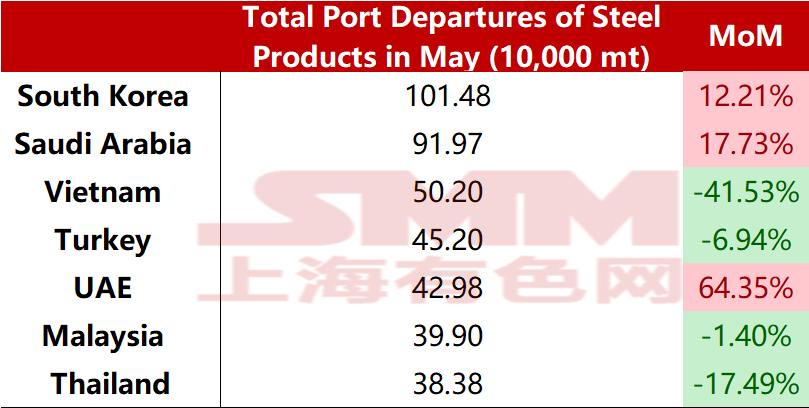

In May, China's total steel exports increased by 1.1% MoM. Following the China-US Geneva Statement on May 12, trade frictions between the two sides eased somewhat, and the investigation into false export declarations had not yet erupted. As a result, the "rush to export" and "export rush" phenomena continued. According to the SMM survey, the planned export volume of HRC from steel mills in May increased by 3.2% MoM from April. Overall, China's total steel exports remained at a high level in May. According to SMM shipping data, the top six countries for China's steel port departures in May were South Korea, Saudi Arabia, Vietnam, Turkey, the UAE, and Malaysia. As South Korea may impose anti-dumping duties on China in H2, the current "rush to export" phenomenon remains evident there. Meanwhile, countries like Saudi Arabia, with relatively small demand fluctuations and fewer anti-dumping measures against China, have become major destinations for domestic export traders.

Top 6 Countries for China's Steel Imports in May 2025

Data Source: SMM Shipping Data

• China's Steel Imports Remain at a Low Level in May

On the import side, China imported 481,000 mt of steel in May, down 24.49% YoY, maintaining an overall net export situation. In the first five months, China's net steel exports reached 45.916 million mt.

• Short-Term Outlook for Steel Exports

According to data released by the China Federation of Logistics and Purchasing, the global manufacturing PMI in May 2025 was 49.2%, up 0.1% MoM. Global manufacturing fluctuations were relatively small, operating in contraction territory for three consecutive months, and the global economy's recovery capacity weakened somewhat in the short term. According to China's manufacturing PMI data, the new export orders index for China's manufacturing sector in May was 47.5%, rebounding by 2.8 percentage points MoM, indicating a significant improvement in China's current overseas order-taking situation compared to April. Data monitored by the World Steel Association shows that in April 2025, the global crude steel production of 69 countries included in the World Steel Association's statistics was 155.7 million mt, a 0.3% YoY decrease. China's production remained flat YoY, while the production in the rest of the world (excluding China) was 69.7 million mt, a 0.57% YoY decrease.

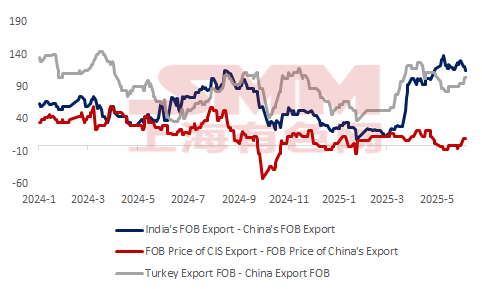

As of June 6, 2025, the export offers (FOB) for hot-rolled coil (HRC) from India, Turkey, and the CIS were $560/mt, $550/mt, and $445/mt, respectively. China's HRC export offer (FOB) was $445/mt. Currently, China's HRC export offers are $115/mt, $105/mt, and $10/mt lower than those of other countries, respectively, with price advantages of -6.5%, +7.14%, and +233.33% MoM compared to May.

According to the latest steel mill export order scheduling from SMM, the planned HRC export volume in June is expected to increase by 9.37% compared to the actual export volume in May. Meanwhile, China's steel export prices still maintain a relative advantage. Therefore, it is expected that steel exports in June will remain at a high level YoY.

However, the risks faced by China's steel exports are also increasing. Firstly, HRC, as the largest category in China's total steel exports, has two of its top five export destinations initiating anti-dumping investigations against China, with more anti-dumping categories expected to follow. On the other hand, Trump announced on May 30 that starting from June 4, the 25% tariff on foreign-made steel and aluminum products imported into the US would be significantly increased to 50%. Although the direct volume of Chinese steel exports to the US is limited, the main importing countries of US steel are also major destinations for China's steel exports, such as South Korea. According to data, after the official implementation of the 25% tariff, South Korea's steel exports to the US dropped by 20.6% in May this year. With the implementation of the 50% tariff, a significant decline in South Korea's steel exports to the US is inevitable. This also poses a crisis for domestic steel re-export trade.

According to SMM shipping data, as of May 31, the total port departures from Chinese ports in May were 11.6071 million mt, a 6.52% MoM decrease from April. The main reason for the discrepancy with customs data may be the decrease in billet exports MoM in May. Considering that major export traders and steel mills often set annual export targets, even in adverse external conditions, there may be instances of volume discounts. Therefore, SMM expects that steel export volume in June will still maintain high growth YoY, but MoM data may face a slight decline risk after three consecutive months of exceeding 10 million mt. The uncertainty of steel exports in H2 will increase.