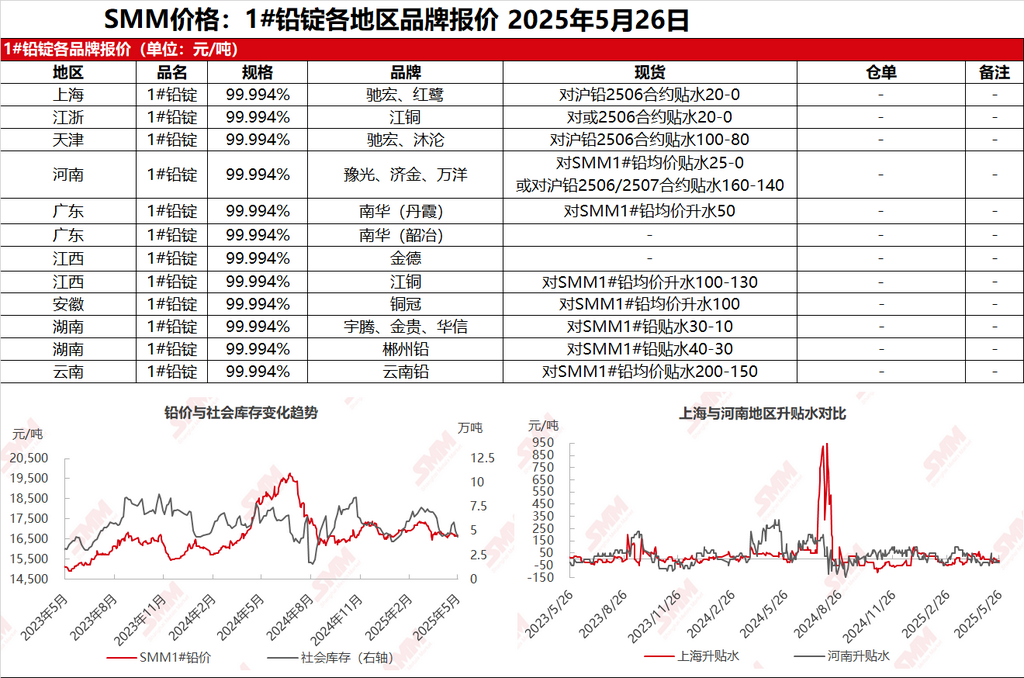

SMM reported on May 26: In the Shanghai market, Chihong and Honglu lead were quoted at 16,790-16,825 yuan/mt, with quotations against the SHFE lead 2506 contract at a contango of 20-0 yuan/mt. In the Jiangsu-Zhejiang region, JCC lead was quoted at 16,790-16,825 yuan/mt, with quotations against the 2506 contract at a contango of 20-0 yuan/mt. SHFE lead maintained a consolidation trend, with suppliers adjusting their quotations accordingly. The contango in quotations remained largely unchanged. Specifically, for cargoes self-picked up from production sites at primary lead smelters in major producing areas, quotations were at a contango of 20 yuan/mt to a premium of 100 yuan/mt against the SMM 1# lead average price on an ex-factory basis. Secondary lead smelters held firm on prices when selling, with secondary refined lead quotations at a contango of 50-0 yuan/mt against the SMM 1# lead price on an ex-factory basis, and some quotations at a premium of 50-75 yuan/mt. Downstream enterprises mainly made just-in-time procurement, with many options available, making it difficult for some smelters to close deals for cargoes self-picked up from production sites.

Other markets: Today, the SMM 1# lead price increased by 25 yuan/mt from the previous trading day. In Henan, suppliers offered quotations at a contango of 25-0 yuan/mt against the SMM 1# lead price, or at a contango of 160-140 yuan/mt against the SHFE lead 2506/2507 contracts on an ex-factory basis, but transactions were sluggish. In Hunan, after the inventory pressure at smelters eased, some enterprises narrowed their contango in quotations. Spot order quotations were at a contango of 20-10 yuan/mt against the SMM 1# lead average price on an ex-factory basis, while supplier quotations were at a contango of 40-30 yuan/mt against the SMM 1# lead average price on an ex-factory basis. In the Guangdong market, quotations for cargoes self-picked up from production sites at smelters were at a slight premium of 0-50 yuan/mt against the SMM 1# lead price. Today, lead prices held up well, with downstream enterprises mainly making just-in-time procurement. Transactions were moderate in some regional markets, but most transactions remained sluggish.

![Lead Price Ran Below Daily Average Line Intraday, Fluctuated Downward and Closed with a Shaven Head Bearish Candlestick [Brief Comment on Lead Futures]](https://imgqn.smm.cn/usercenter/yqTpQ20251217171721.jpeg)

![SMM May 28 Automotive Battery Market Summary [SMM Evening News]](https://imgqn.smm.cn/usercenter/hrxHx20251217171721.jpeg)