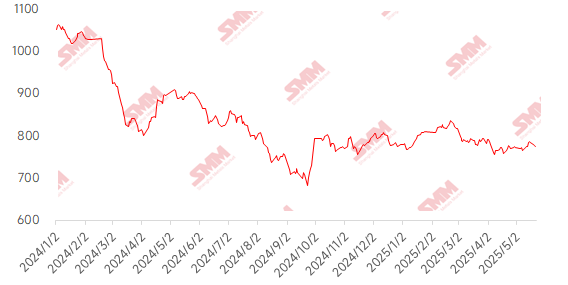

This week, the imported iron ore market exhibited a fluctuating trend, with the price center gradually shifting downward. Early in the week, market sentiment improved on expectations of demand growth, fueled by monetary easing signals such as the LPR cut. However, the State Council meeting on Thursday focused on the technology sector, providing limited support to ferrous metals. Market sentiment remained weak. Supply-side disruptions, including adjustments to mining rights in Guinea and a port accident in Peru, briefly pushed up ore prices. However, seasonal weakness in end-use demand and a continuous decline in apparent consumption ultimately suppressed prices, causing them to weaken again. The spot market performed relatively steadily. Taking PB fines at Shandong ports as an example, the weekly average price fell by 8 yuan/mt WoW.

Chart-: SMM 62% Imported Ore MMi Index

Source: SMM

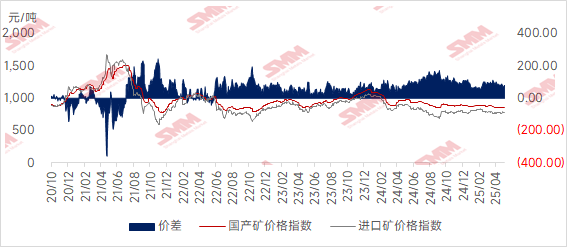

This week, domestic ore prices showed mixed performance. It is expected that domestic ore prices may decline slightly next week. In Hebei's Tangshan, Qian'an, and Qianxi regions, prices fell slightly by 1-5 yuan/mt. In west Liaoning, prices in Chaoyang, Beipiao, and Jianping remained basically stable. In east China, prices increased by 20-30 yuan/mt.

In Tangshan, Hebei, iron ore concentrate prices remained relatively stable. The dry-basis, tax-inclusive delivery-to-factory price for 66% grade ore was 935-940 yuan/mt. Overall market transactions were sluggish, with traders operating cautiously. Coupled with steel mills driving down prices, their operating space was extremely limited, resulting in a strong wait-and-see sentiment. In beneficiation, operations did not improve, with this being particularly evident in Zunhua and Qianxi. Some beneficiation plants halted production due to difficulties in sourcing raw materials and high costs, leading to a low supply of concentrates and strong support for local prices.

In west Liaoning, the domestic ore market remained generally stable. The wet-basis, tax-excluded ex-factory price for 66% grade ore was 705-710 yuan/mt. Most producers refused to budge on prices, but weak downstream demand and recent weakness in steel prices made traders cautious about inquiries and more inclined to offer low prices. In beneficiation, recent land and safety inspections have affected production at some beneficiation plants. Local iron ore concentrate resources remain tight, providing some support for local ore prices. Steel mills are also mainly purchasing as needed, with ongoing competition between sellers and buyers in the market.

In east China, most beneficiation plants are operating normally as planned. However, overall market transactions are relatively sluggish, with some beneficiation plants facing inventory accumulation issues and formulating relevant sales promotions. Currently, steel mills are maintaining low inventory levels, with overall purchases mainly made as needed.

Chart-: Price Spread Between Imported and Domestic Ores

Source: SMM

Looking ahead to next week

For imported ore: The iron ore market will maintain a pattern of weak supply and demand. On the supply side, weather disruptions in Australia have limited shipments from Port Hedland, but a slight rebound in port arrivals has kept overall supply stable. On the demand side, with an increase in regular maintenance at steel mills, the daily average pig iron production is expected to continue to decline by 10,000 mt. It is worth noting that the high level of steel exports has partially offset the weakness in domestic demand. Coupled with the expectation of coke price cuts, which has improved the profit margins of steel mills, there is insufficient motivation for voluntary production cuts, providing some support for ore prices. Overall, under the influence of weak industry expectations, ore prices are expected to continue facing downward pressure next week, exhibiting a narrow and fluctuating trend in the doldrums.

From the perspective of domestic ore: In general, the resources of domestic iron ore concentrates remain in a tight supply trend, providing some support for overall ore prices. Given the current profit margins of steel mills, their desire to bargain down prices remains strong. It is expected that the prices of domestic iron ore concentrates may decline slightly next week.

》Click to view the SMM Metal Industry Chain Database

![[SMM Steel] Indian rupee steadies amid hedging demand and geopolitical risks](https://imgqn.smm.cn/usercenter/QMaot20251217171719.jpg)

![[SMM Steel] EUROFER calls for CBAM refinements ahead of CO₂ price announcement](https://imgqn.smm.cn/usercenter/JSngP20251217171719.jpg)

![[SMM Steel] EU semi-finished steel imports jump in 2025, led by China](https://imgqn.smm.cn/usercenter/VgxkU20251217171719.jpg)