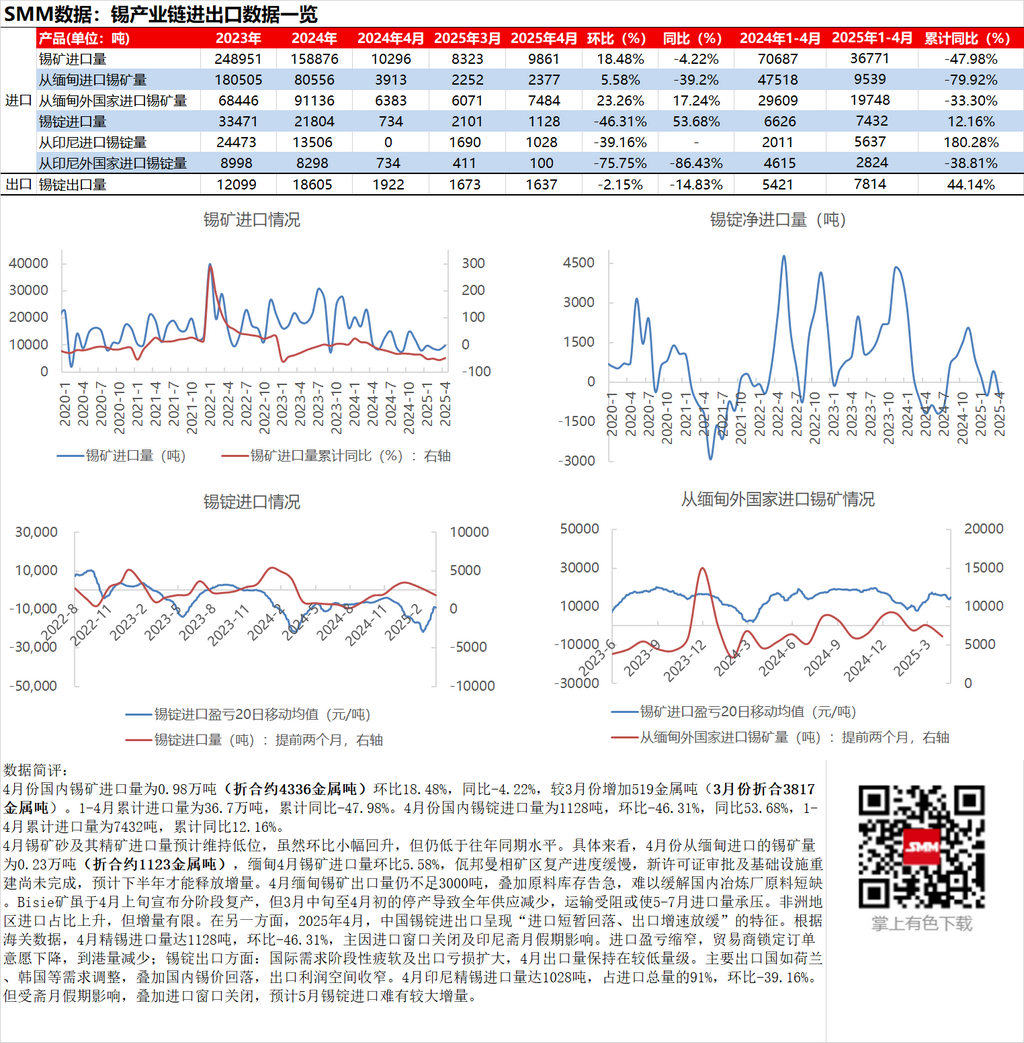

In April, domestic tin ore imports stood at 9,800 mt (equivalent to approximately 4,336 mt (metal content)), up 18.48% MoM and down 4.22% YoY, representing an increase of 519 mt (metal content) compared to March (equivalent to 3,817 mt (metal content) in March). The cumulative imports from January to April reached 367,000 mt, down 47.98% YoY. In April, domestic tin ingot imports amounted to 1,128 mt, down 46.31% MoM and up 53.68% YoY. The cumulative imports from January to April totaled 7,432 mt, up 12.16% YoY.

The import volume of tin ores and concentrates in April is expected to remain low. Although there was a slight MoM rebound, it was still below the level of the same period in previous years. Specifically, tin ore imports from Myanmar in April were 2,300 mt (equivalent to approximately 1,123 mt (metal content)), up 5.58% MoM. The production resumptions at the Manxiang mining area in Wa State, Myanmar, have been slow, with new license approvals and infrastructure reconstruction yet to be completed. Incremental supply is expected to be released only in H2. Myanmar's tin ore exports in April remained below 3,000 mt. Coupled with critically low inventories of raw materials, it is difficult to alleviate the shortage of raw materials for domestic smelters. Although the Bisie mine announced phased production resumptions in early April, the production halt from mid-March to early April led to a reduction in annual supply, and hindered transportation may put pressure on import volumes from May to July. The proportion of imports from Africa increased, but the increment was limited. On the other hand, in April 2025, China's tin ingot imports and exports exhibited characteristics of "a temporary pullback in imports and a slowdown in export growth." According to customs data, refined tin imports reached 1,128 mt in April, down 46.31% MoM, primarily due to the closure of the import window and the impact of the Ramadan holiday in Indonesia. The narrowing of import profit/loss reduced traders' willingness to lock in orders, leading to a decrease in port arrivals. In terms of tin ingot exports, the international demand was sluggish in phases, and export losses expanded, keeping export volumes at a low level in April. Demand adjustments in major exporting countries such as the Netherlands and South Korea, coupled with the pullback in domestic tin prices, narrowed the export profit margin. Indonesia's refined tin imports reached 1,028 mt in April, accounting for 91% of the total imports, down 39.16% MoM. However, affected by the Ramadan holiday and the closure of the import window, it is expected that there will be no significant increase in tin ingot imports in May.

![[SMM Tin News Flash: Institution: Global Smartphone SoC Shipments Down 8% YoY in Q1, Expected to Rebound in Early 2028]](https://imgqn.smm.cn/usercenter/pLauM20251217171751.jpg)