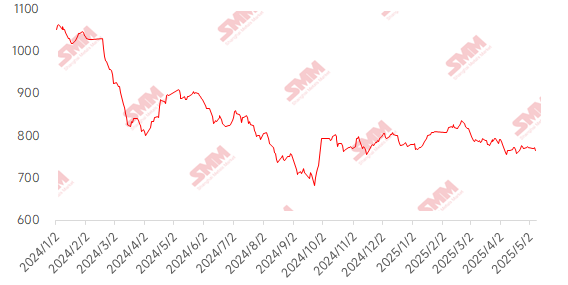

This week, the imported iron ore market showed a trend of jumping initially and then pulling back, mainly influenced by the intertwining of bullish and bearish factors: the post-holiday State Council press conference released a package of financial favorable policies, briefly boosting market sentiment and driving futures prices to rise rapidly; however, subsequently, details emerged that steel mills in multiple provinces received verbal notices of crude steel production reduction, exacerbating demand-side concerns against the backdrop of already loose supply and demand for iron ore, coupled with the obvious weakening of end-use consumption and the expected inflection point of pig iron production, collectively leading to a maximum intraday drop of 2.05% in the most-traded I2509 contract. However, current pig iron production is at a yearly high, and the post-holiday restocking demand from steel mills has been released, keeping port spot cargo transactions active and spot prices strongly supported, causing the spread between futures and spot prices to further widen to 60 yuan/mt. In terms of port prices, the price of PB fines in Shandong dropped by 5 yuan/mt MoM.

Chart: SMM 62% Imported Ore MMi Index

Data source: SMM

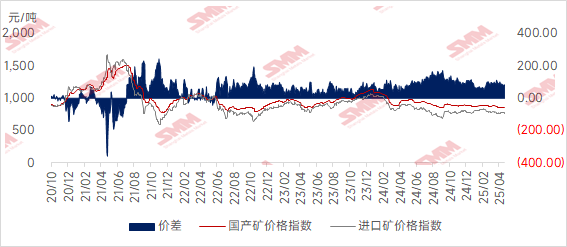

This week, domestic ore prices dropped slightly, and it is expected that domestic ore prices will continue to decline next week. This week, prices in Tangshan, Qian'an, and Qianxi in Hebei dropped by 5-10 yuan/mt MoM compared to pre-holiday levels, while prices in west Liaoning, Chaoyang, Beipiao, and Jianping were lowered by 5-10 yuan/mt; prices in east China were reduced by 10-15 yuan/mt.

The price of Tangshan iron ore concentrates slightly decreased compared to pre-holiday levels, with the 66-grade dry basis tax-included delivery-to-factory price at 930-940 yuan/mt; currently, overall production at mines and beneficiation plants is relatively stable, but the overall resumption of production is slow, and local iron ore concentrate resources remain relatively tight, providing some support to local ore prices. Steel mills currently have no maintenance plans, and pig iron production in blast furnaces remains at a relatively high level, providing some support for the demand for iron ore concentrates, but steel mills are still mainly purchasing as needed, and the overall market transaction is sluggish.

The market price of domestic ore in west Liaoning remained stable, with post-holiday restocking by local steel mills supporting the sentiment to stand firm on quotes at beneficiation plants. Local mines and beneficiation plants are affected by safety inspections, with overall operations at a low level, and the resource shortage situation is quite obvious, with a strong wait-and-see sentiment at mines and beneficiation plants. Steel mills are mainly purchasing as needed, and recently, there have been reports that steel mills in the northeast region have received notices of crude steel production reduction, intensifying market pessimism.

In the east China region, mines and beneficiation plants are mostly producing normally as planned, selling as they produce, with no significant inventory pressure; some individual mines and beneficiation plants that had stopped production have resumed partial production, and production may increase in the later period, potentially alleviating the overall tight supply trend.

Chart: Price Spread Between Domestic and Imported Ore

Looking ahead to next week

For imported ore:The iron ore market is expected to maintain a weak and fluctuating pattern: from a macro perspective, policies are in a window period, and the possibility of repeated negotiations on Sino-US tariffs requires close attention to related developments over the weekend that may affect market sentiment; fundamentally, there is a trend of weakening supply and demand, with overseas shipments entering the peak season cycle, and port arrivals are expected to increase MoM; against the backdrop of weakening end-use demand, steel mill maintenance plans are increasing, and SMM expects daily average pig iron production to pull back by around 10,000 mt.Under the dual pressures of increasing supply and weakening demand, ore prices are expected to remain in the doldrums. Key areas of focus include: 1) changes in apparent consumption; 2) the accumulation rate of inventories for the five major steel products.

From the perspective of domestic ore: Overall, the overall supply of domestic ore remains tight. On the demand side, as the production of pig iron in blast furnaces at steel mills gradually decreases, the demand support for iron ore concentrates may weaken. Coupled with the current impact of tariffs and news about crude steel production cuts, it is expected that domestic iron ore prices will be in the doldrums with volatile movements next week.

》Click to view the SMM Metal Industry Chain Database

![[SMM Steel] Indian rupee steadies amid hedging demand and geopolitical risks](https://imgqn.smm.cn/usercenter/QMaot20251217171719.jpg)

![[SMM Steel] EUROFER calls for CBAM refinements ahead of CO₂ price announcement](https://imgqn.smm.cn/usercenter/JSngP20251217171719.jpg)

![[SMM Steel] EU semi-finished steel imports jump in 2025, led by China](https://imgqn.smm.cn/usercenter/VgxkU20251217171719.jpg)