》View SMM metal quotes, data, and market analysis

》Subscribe to view historical price trends of SMM metal spot cargo

In April, copper prices bottomed out and rebounded. At the beginning of the month, due to Trump's ever-changing stance on tariff negotiations, market concerns about a trade war weighed on non-ferrous metals, with copper bearing the brunt. LME copper fell to $8,150/mt, and SHFE copper hit the daily limit down. The price spread between LME and COMEX briefly narrowed, but as market sentiment about tariff "uncertainties" waned, the US continued to siphon off copper cathode.

According to SMM's interactions with the market, when SHFE copper fell below 75,000 yuan/mt, downstream orders significantly exceeded expectations, followed by a rush to buy amid continuous price rise, pushing copper prices back to around 77,000 yuan/mt. Spot transactions were active across the country in April. SMM smelter production reached 1.1257 million mt. Against the backdrop of tight copper scrap supply in April, some enterprises indicated that they had stocked up on copper scrap raw materials in March, and the supplementary imports of copper anode in April boosted copper cathode production at smelters that do not use copper concentrates.

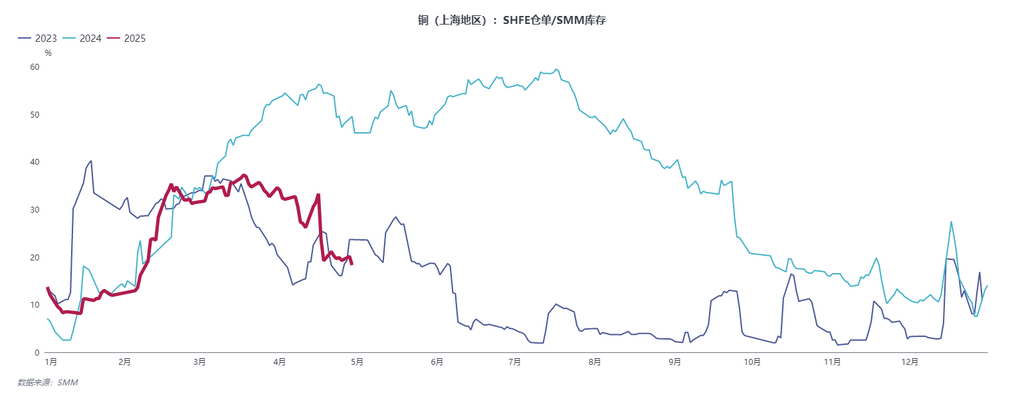

However, the east China market currently mainly trades registered copper cathode cargo and imported non-registered cargo from Africa, Russia, Kazakhstan, etc., with the volume of cargo meeting delivery standards increasingly dwindling. With both domestic arrivals and imports being low, active outflows led to a larger-than-expected decline in inventory. The BACK price spread between nearby and deferred months continued to widen.

- Continuous inventory destocking greatly supported spot premiums and discounts.

According to SMM data, social inventory of copper cathode in China decreased by approximately 200,000 mt in April, with Shanghai accounting for about 110,000 mt of the reduction. Spot premiums rose from 10 yuan/mt at the beginning of the month to over 200 yuan/mt by month-end.

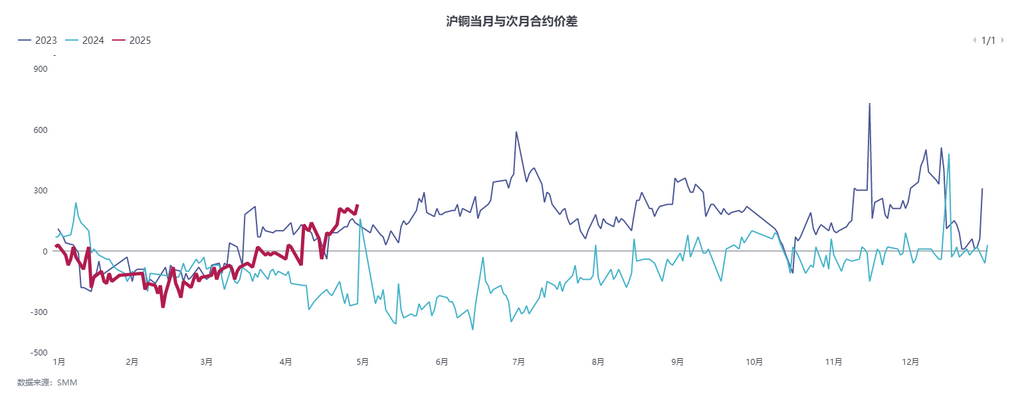

- The price spread between nearby and deferred months widened significantly, with more speculation in deferred months. The annual trend is approaching that of 2023.

The BACK price spread between nearby and deferred months widened to 200 yuan/mt and then hovered, failing to further expand to 300 yuan/mt as expected. Most speculators positioned their holdings in July, August, and September, where the BACK price spread between deferred months offered more arbitrage opportunities.

However, considering the current proportion of warrants to social inventory, this proportion continues to decline amid inventory destocking, raising the risk of a squeeze. It is foreseeable that the BACK price spread between nearby and deferred months of SHFE copper could achieve a profit of 300-400 yuan/mt, with attention needed to extreme changes in the price spread as the final trading day approaches.

3, 4. Tight copper scrap supply in March and April made non-registered copper cathode the preferred choice for downstream procurement

Due to US tariff disruptions combined with policies in the recycling industry, copper scrap shipments tightened, and imported non-registered and non-standard cargo played a substitutive role, while also promoting copper cathode destocking. SMM's price spread between SX-EW and non-registered copper provided clear guidance on the price difference between copper cathode and copper scrap, which generally converged in April.

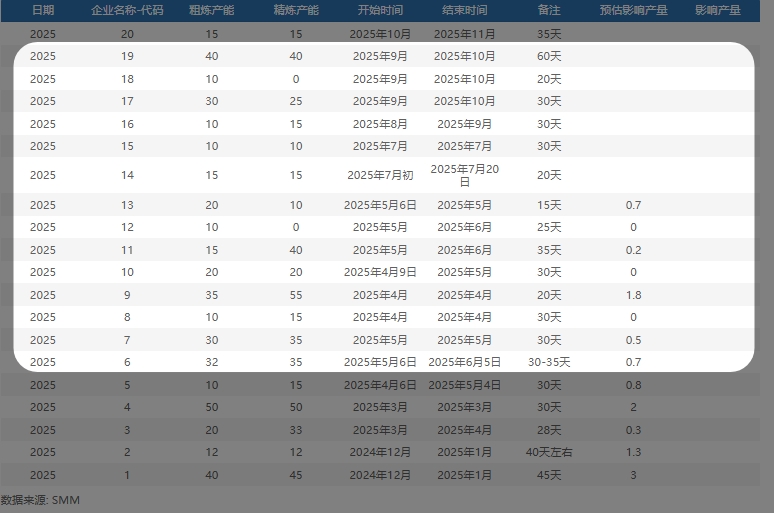

4. Subsequent smelter maintenance both domestically and overseas, coupled with amplified disruptions to overseas copper anode, further weakened copper concentrate TC

At the end of March 2025, Glencore Plc suspended copper shipments from its Altonorte smelter in Chile due to impacts on the smelting furnace. The smelter mainly produces customized copper anode, with an annual copper production capacity of approximately 350,000 mt in metal content. An anode copper smelter in Zambia with a capacity of 350,000 mt in metal content will undergo maintenance from April to June 2025, affecting production during that period. On April 30, the SMM Imported Copper Concentrate Index (weekly) was reported at -$42.61/dmt, a decrease of $0.09/dmt from the previous period's -$42.52/dmt. The pricing coefficient for domestic trade ore with a grade of 20% was 93%-95%.

In May, several domestic smelters have maintenance plans, with an estimated impact of 21,000 mt on copper cathode production. There are still concentrated maintenance plans from July to September.

Overall, supported by April's consumption, the low inventory situation in May supports the nearby month structure and premiums. However, the market is concerned that from late May to late June, tariff uncertainties may lead to a decline in export orders, affecting the continuity and enthusiasm of end-user procurement. As May progresses, while supply issues persist, whether consumption can continue to improve or even maintain remains to be seen. Currently, the price spread between the SHFE copper 2505 and 2506 contracts is expected to widen to 500 yuan/mt before delivery, with the deferred month structure still expected to continue widening.

》View SMM metal industry chain database