As can be seen from the chart, due to the continuous growth of iron ore supply in recent days, the supply and demand has shifted from tight to loose and then to surplus. This has led to a continuous downward shift in the price center of iron ore. The average price of Platts 62% in 2022 was $120/mt. In 2023, despite a slight supply surplus, the price remained around $119/mt due to supply-demand mismatch and other factors. However, in 2024, the supply surplus became more pronounced, causing ore prices to drop by around $10/mt to $109/mt. In 2025, domestic and overseas mines still have plans to increase production, leading to greater global iron ore supply pressure. Therefore, we expect the price center of ore to continue to decline by around $10/mt for the whole year of 2025, with an average price of around $95/mt.

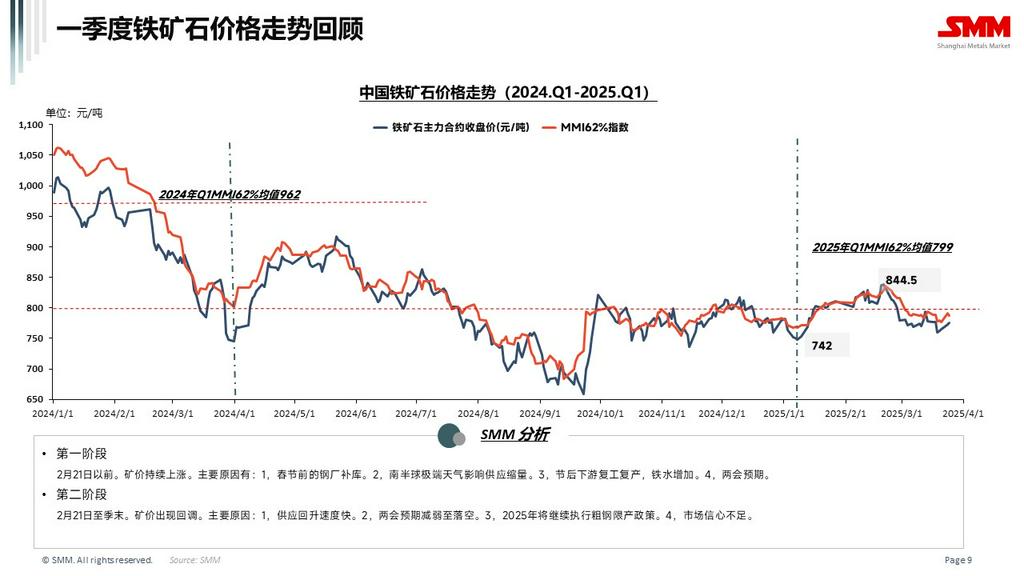

Looking at Q1 2025, iron ore prices first rose and then fell. The price center was slightly higher than in Q4 2024. The average SMM 62% MMI price index increased by 16 points. The price range of the most-traded contract I2505 was 742-844 yuan/mt. The Platts 62% index ranged from 97.6 to 109.5, with an average of $103.75/mt.

The high point in Q1 occurred on February 21. The reasons for the initial rise and subsequent fall are analyzed in the chart.

Currently, although tariff policies have been a constant interference, their actual impact on steel exports has not yet materialized. Domestic demand has entered the peak season and continues to grow. Will the peak season end the fluctuating trend and ignite a new market trend?

Domestic Ore Situation

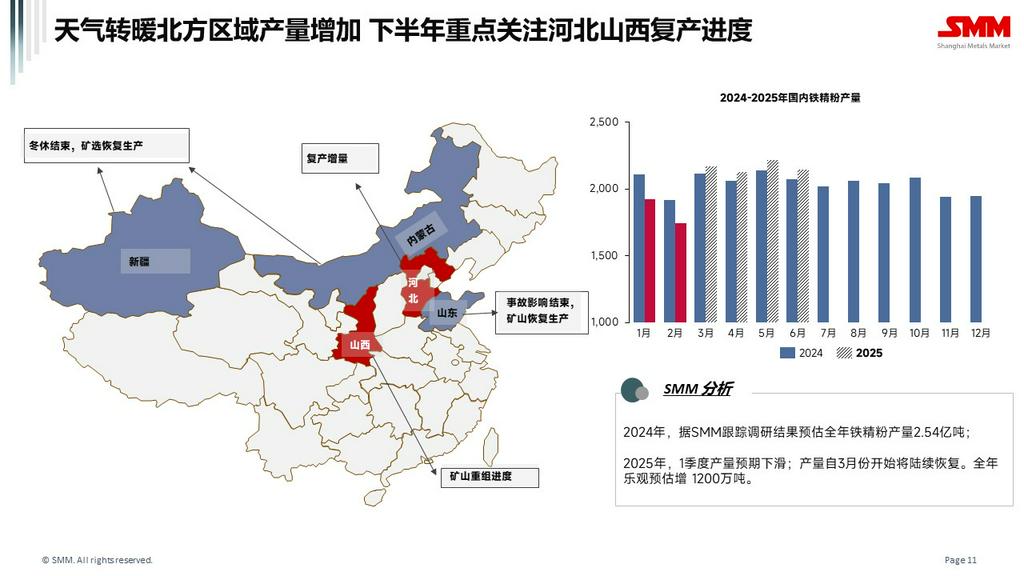

In 2024, SMM estimated domestic concentrate production at 254 million mt. In Q1 this year, production declined due to conventional factors such as the winter break and Chinese New Year, but the impact was greater this year mainly because ore prices were low before the Chinese New Year, leading to longer shutdowns at some mines than in previous years. Additionally, mines in Shandong that were shut down due to a major mining accident in November last year have not fully resumed production, resulting in a significant decline in overall production. However, after March, mines in colder regions such as north-west and north-east China have gradually resumed production, leading to an increase in output. Mines in Linyi, Shandong, which were shut down due to the mining accident in November last year, have also gradually resumed production after the Chinese New Year. However, major local mines such as Jinxita are still in a shutdown state and are expected to resume production in Q2. Additionally, our survey indicates that the restructuring of mines in Shanxi is accelerating, with the earliest resumption of production expected by the end of Q2. The processing speed of mining permits and other procedures in Hebei has also accelerated, and mines are expected to gradually resume production in Q3. Therefore, we estimate that starting from March, the growth rate of domestic concentrate production will accelerate and is expected to be higher than the same period last year. Thus, the overall production in H1 will be on par with last year. Optimistically, annual production is expected to increase by 12 million mt.

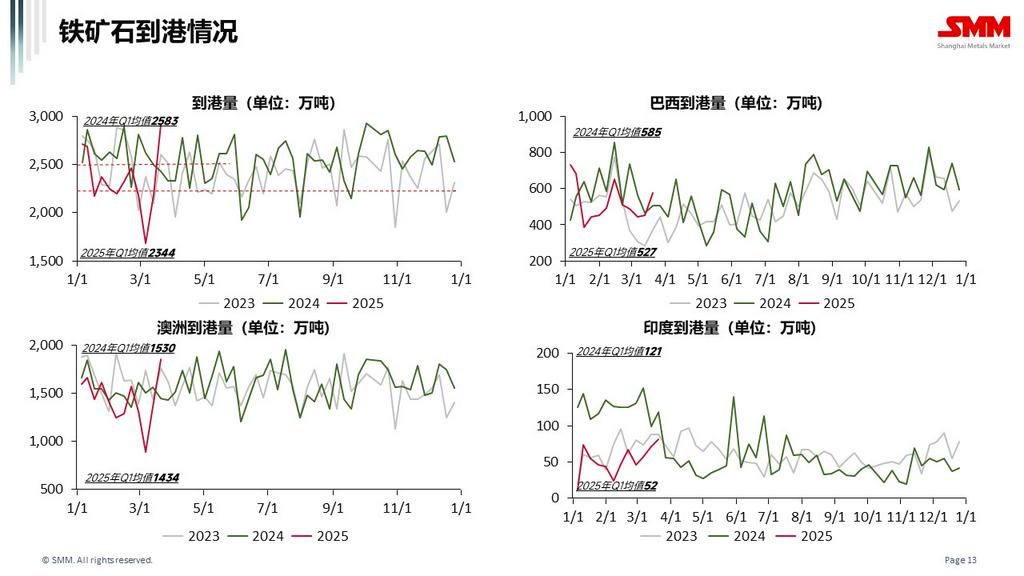

Imported Ore Section

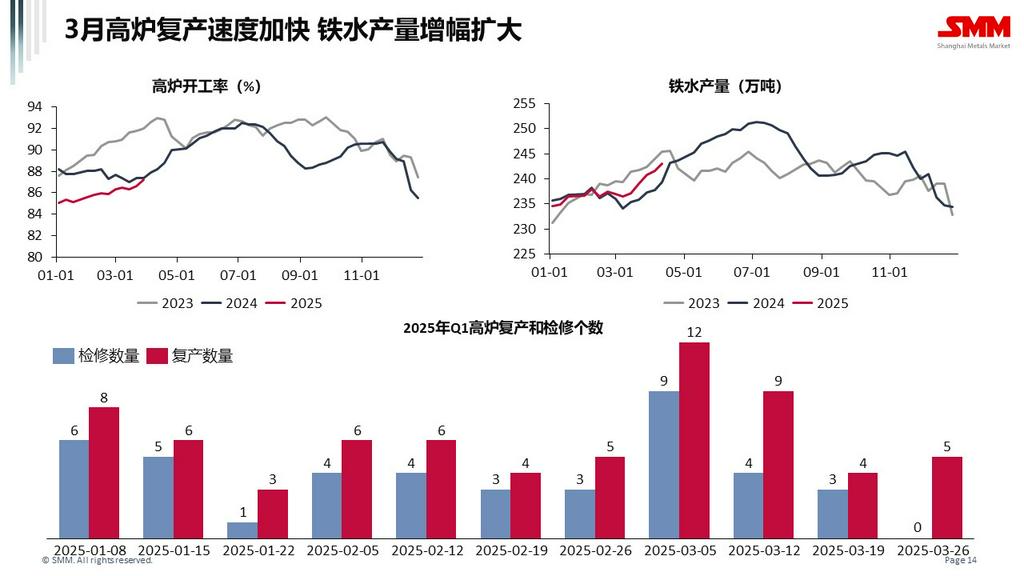

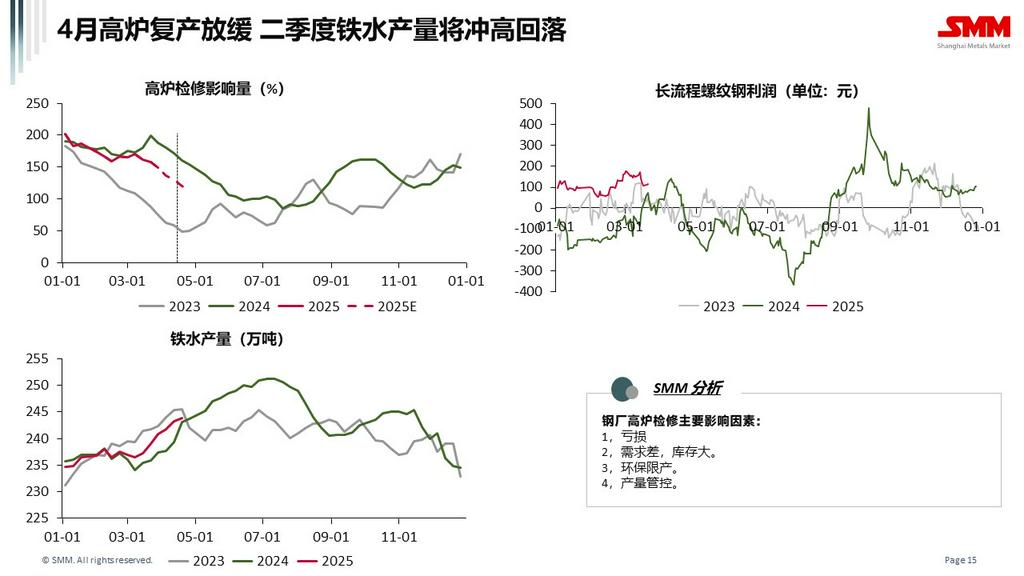

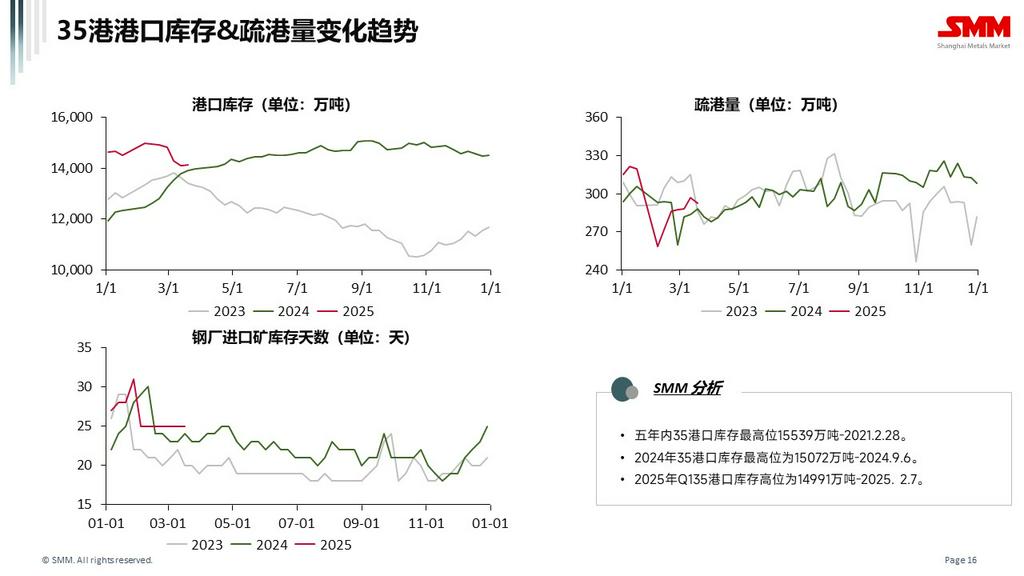

Iron Ore Demand Situation

Iron Ore Demand Situation

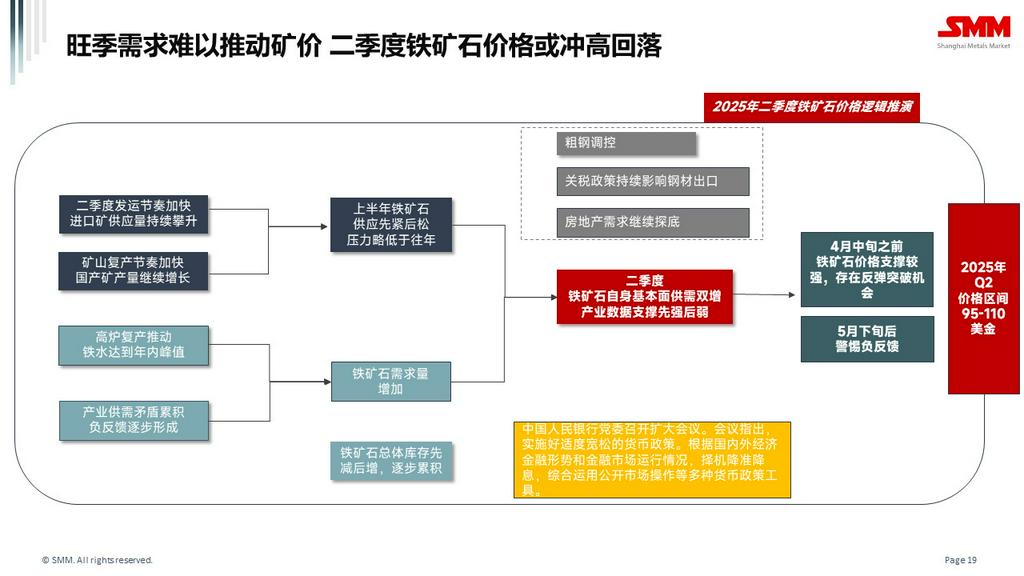

Peak Season Demand Fails to Drive Ore Prices

Iron Ore Prices May Jump Initially and Then Pull Back in Q2

SMM Black Industry Data Introduction

SMM Black Industry Data Introduction

Click to View SMM Metal Industry Chain Database

![Ferrous Metals May Continue Trading at Elevated Levels in the Short Term [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/yBlDX20251217171747.jpg)