Weekly Review

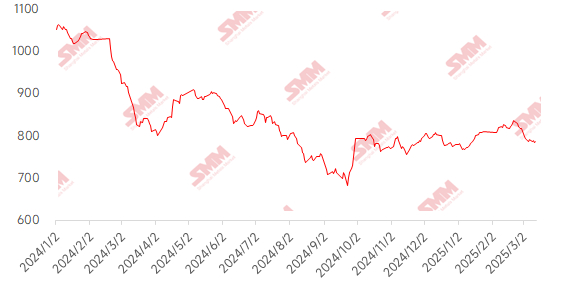

This week, iron ore prices fluctuated repeatedly. From a fundamental perspective, global shipments remained high, but port arrivals dropped significantly, and port inventories continued to decline. On the demand side, in the first half of the week, heavy pollution in Tangshan led to production restrictions on blast furnaces at some steel mills, causing a slight decline in demand. As the weather improved, sintering machines and blast furnaces resumed production, leading to a recovery in demand. Coupled with low iron ore prices, steel mills increased restocking activities. However, frequent news of crude steel production cuts, combined with the expanding impact of anti-dumping measures, resulted in bearish market sentiment, with iron ore prices showing a weak-to-strong trend. In terms of port prices, PB fines in Shandong rose by 1 yuan/mt MoM.

Chart: SMM 62% Imported Ore MMi Index

Data Source: SMM

This week, domestic ore prices saw a slight decline. Domestic ore prices are expected to remain stable with a weak trend next week. This week, prices in Hebei's Tangshan, Qian'an, and Qianxi regions fell by 1-5 yuan/mt, while prices in west Liaoning's Chaoyang, Beipiao, and Jianping dropped by 5-10 yuan/mt. Prices in east China decreased by 30-49 yuan/mt.

After the conclusion of an important meeting this week, some steel mills in the Tangshan area that had undergone maintenance gradually resumed production. Coupled with low raw material inventories, this provided support for local prices. Resources at mines and beneficiation plants remained tight, and the slow progress of resumption of work and production offered some support for local iron ore concentrate prices. On the demand side, as blast furnaces gradually resumed production, local iron ore concentrate prices were further supported.

In west Liaoning, iron ore concentrate prices recently saw a slight decline, with 66% grade wet basis ex-factory prices excluding tax at 720-730 yuan/mt. After the Two Sessions, local mines and beneficiation plants gradually resumed normal production. However, according to local sources, the provincial emergency management department is expected to strengthen safety inspections during its visits to local mines from the 18th to the 20th of this month. On the demand side, local steel mills mainly maintained normal production and purchased as needed.

In east China, mines and beneficiation plants mostly maintained normal production, with production and sales aligned and no significant inventory pressure. In Shandong's Linyi area, mines and beneficiation plants are expected to resume production soon, which may ease the tight supply of local iron ore concentrates.

Outlook for Next Week

For imported ore:Macro policies are in a vacuum period, and price trends mainly depend on fundamentals. With shipments from Australia and Brazil gradually recovering, port arrivals are expected to increase significantly. On the demand side, as the peak season arrives, steel demand still has room to grow. Additionally, falling coke prices and improved steel mill profits are accelerating pig iron production growth, supporting iron ore demand. However, the delayed implementation of crude steel production cut policies is limiting the rebound potential of iron ore prices. Overall, iron ore prices are expected to continue upward next week, but the increase may be limited.

For domestic ore:Overall, the tight supply of domestic iron ore concentrates persists, with a strong sentiment to stand firm on quotes. Recent market rumors about crude steel production cuts have led to bearish market sentiment. In the short term, domestic iron ore concentrate prices are expected to remain stable with weak fluctuations.

Click to View the SMM Metal Industry Chain Database

![Ferrous Metals May Continue Trading at Elevated Levels in the Short Term [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/yBlDX20251217171747.jpg)