SMM February 28 News:

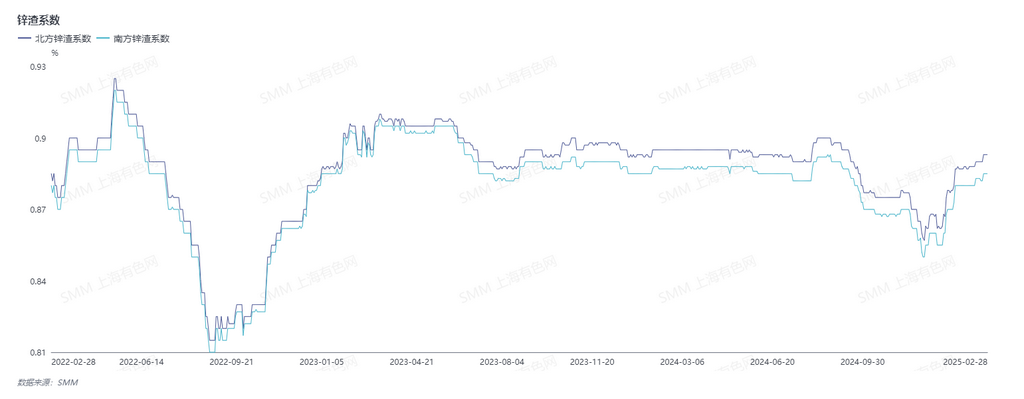

According to SMM, the overall zinc slag coefficient remained high in February. What are the reasons behind this, and how will it evolve in the future?

SMM's analysis identifies the following main reasons:

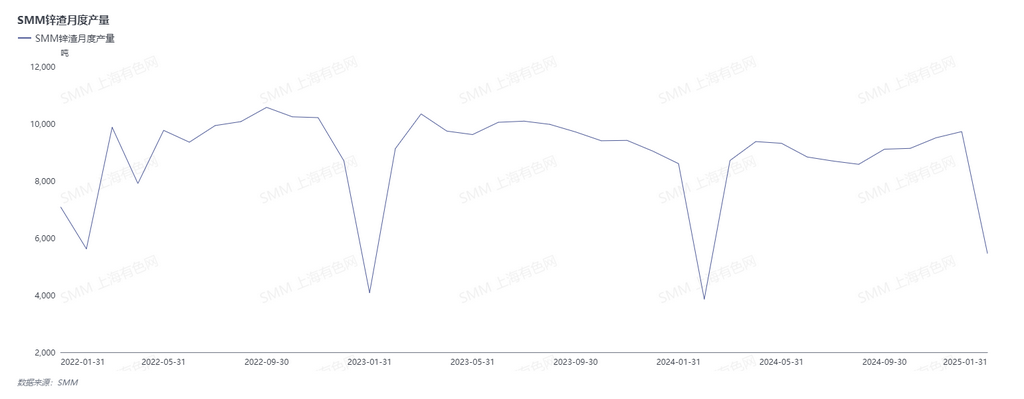

1. End-use consumption recovery fell short of expectations. While the operating rates of galvanising enterprises in February were slightly better than in January, overall operations did not meet expectations. Zinc slag production was not high, and ferrous metals prices also fluctuated downward. Order volumes were average, production enthusiasm among galvanising enterprises was low, competition pressure was significant, and corporate profits were poor. The room for price concessions by galvanising plants was limited, keeping the coefficient relatively firm.

2. Zinc price trends provided some support for the zinc slag coefficient. Macro factors were heavily influenced by tariff disturbances, coupled with relatively loose supply and weak consumption. Zinc prices continued to pull back in February. Considering cost issues, some galvanising enterprises were reluctant to sell, waiting for zinc prices to rebound before selling. Others maintained a stand firm on quotes mentality, keeping the zinc slag coefficient high.

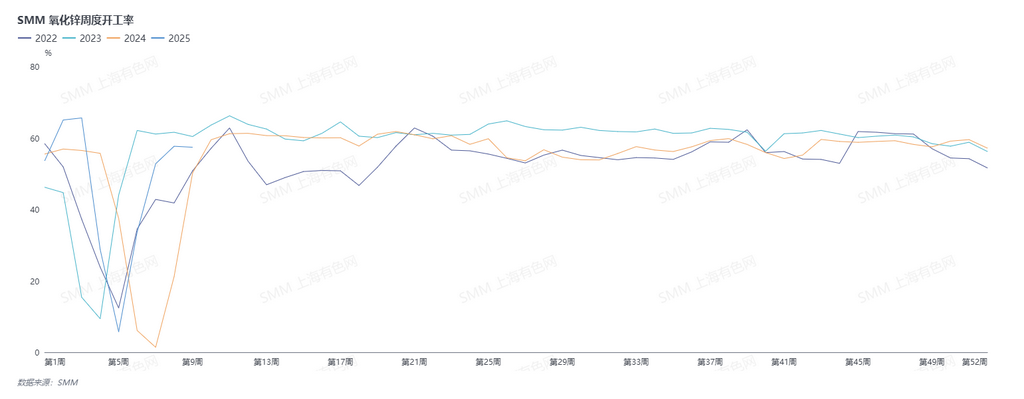

3. Oxidised zinc enterprises performed well in February, leading to an increase in demand for zinc slag. However, due to the low operating rates of galvanising enterprises and the high zinc slag coefficient, zinc slag was difficult to procure. Many oxidised zinc enterprises opted to purchase crude zinc for producing zinc oxide. The increase in demand for zinc slag was limited and not enough to drive the zinc slag coefficient downward.

Looking ahead, zinc prices are expected to continue fluctuating downward. With the increase in galvanising plant operations and marginal improvement in consumption, zinc slag production is expected to increase, leading to relatively loose zinc slag supply. Meanwhile, oxidised zinc operations are likely to remain strong. Based on the current operating rates of galvanising enterprises and future expectations, there may be an opportunity for a downward adjustment in the coefficient.

![Monthly Production Declined: Refined Zinc Faces Dual Pressure from Raw Material Supply and Costs [SMM Analysis]](https://imgqn.smm.cn/usercenter/qdibi20251217171755.jpg)