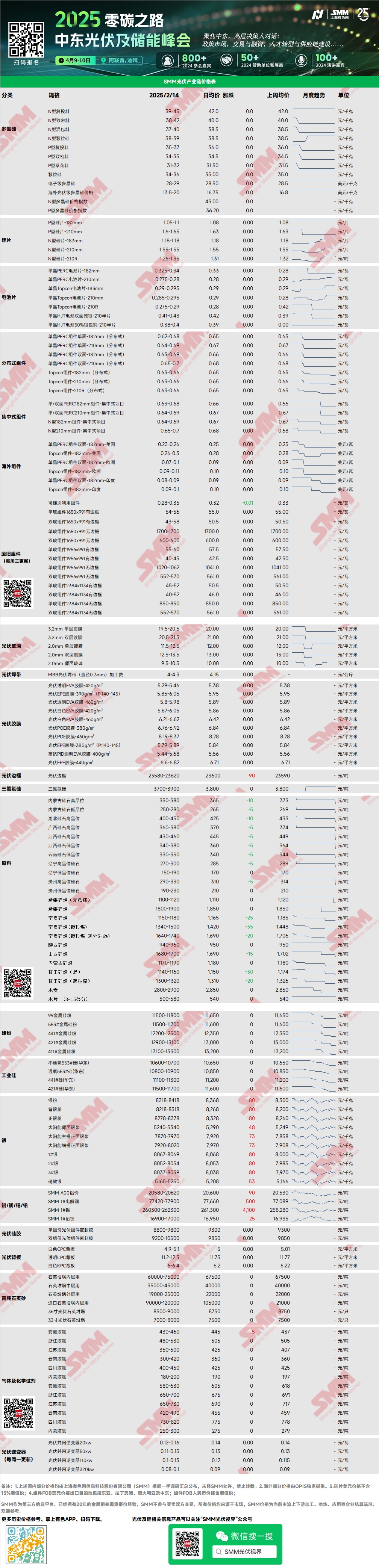

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon were 39-45 yuan/kg, and for N-type dense polysilicon were 38-42 yuan/kg. The transaction range for silicon materials remained unchanged, but some manufacturers saw a slight increase in actual transaction prices with crystal pulling plants, rising from the previous 41-42 yuan/kg to 42-43 yuan/kg. The slight upward movement in market prices was mainly due to top-tier enterprises standing firm on quotes and optimism about H1 installation demand. For the future, the market is temporarily stable and observing, focusing on the upcoming capacity launches and self-regulation of silicon wafer production.

Silicon Wafer: This week, domestic N-type 18Xmm silicon wafers were priced at 1.18-1.18 yuan/piece, N-type 210R wafers at 1.26-1.35 yuan/piece, and N-type 210mm wafers at 1.55-1.55 yuan/piece. Silicon wafer prices saw a slight decline this week, mainly reflected in the drop in 210R prices, with some small manufacturers quoting below 1.26 yuan/piece. This model continued the weak demand trend seen before the holiday. Currently, downstream buyers are strongly resistant to high-priced resources, and the 183 model also saw sporadic price reductions, with room for further decreases. Prices are likely to weaken overall.

Solar Cell: This week, prices for various Topcon solar cells successfully stabilized at high levels. As the Chinese New Year approached, Topcon cells were sold at high price ranges, increasing cost pressure on downstream buyers. However, with pre-holiday stockpiling completed, market sentiment pulled back, and there is a risk of price declines for Topcon cells in the future. Prices for Topcon 183 solar cells (efficiency of 25% and above) were around 0.285-0.295 yuan/W; Topcon 210RN cells were 0.285-0.29 yuan/W; and Topcon 210 cells were 0.285-0.295 yuan/W. PERC cell prices rose to 0.325-0.34 yuan/W, mainly supported by overseas demand and tight supply. Prices are expected to remain firm in the coming months.

PV Module: This week, in the module market, mainstream transaction prices for centralized PERC 182mm modules were 0.63-0.68 yuan/W, PERC 210mm modules were 0.64-0.69 yuan/W, N-type 182mm modules were 0.64-0.7 yuan/W, and N-type 210mm modules were 0.65-0.72 yuan/W. Winning bid prices showed a clear upward trend, but actual execution prices for ground-mounted power stations remained in the low range, with most transactions below 0.66 yuan/W. In February, module manufacturers produced based on demand, with planned production down 13.88% MoM to 35GW. Module production is expected to increase in March-April, with most companies planning significant production increases.

End-User: From January 20 to February 9, 2025, SMM statistics showed that domestic enterprises won bids for 45 PV module projects, with winning bid prices concentrated in the range of 0.61-0.71 yuan/W. The weighted average price for the week was 0.7 yuan/W, and the total awarded procurement capacity was 12,015.38MW, an increase of 7,333.4MW from the previous week. The increase was mainly due to the centralised procurement packages (sections 1-5) of CGN PV modules. After the holiday, a large number of bidding projects are expected to continue, preparing for the launch of new domestic and overseas projects in Q2. The peak installation season in Europe is approaching, with active procurement and stockpiling in most European markets.

EVA: This week, the mainstream transaction prices for PV-grade EVA remained at 11,000-11,400 yuan/mt, while prices for foam-grade and cable-grade EVA saw slight increases. The market's spot supply was tight, and the undersupply situation pushed the overall transaction price center for domestic EVA upward. For EVA film, top-tier enterprises maintained stable prices, with mainstream transaction prices at 12,600-12,800 yuan/mt. Due to the incomplete consumption of low-cost raw material inventory before the holiday, film prices have not yet increased. However, with the cost side of PV-grade EVA showing an upward trend, film prices are also expected to rise accordingly.

PV Glass: This week, PV glass quotations remained stable. As of now, the mainstream quotations for 2.0mm single-layer coating glass were 12.0 yuan/m², for 3.2mm single-layer coating glass were 19.5 yuan/m², and for 2.0mm back glass were 10.0 yuan/m². This week, the module sector officially began market inquiries and purchases. Current February order prices remained stable, with glass companies prioritizing destocking. In February, domestic module companies are expected to stockpile glass volumes exceeding planned production by approximately 15GW. This is mainly due to favorable domestic end-use demand, especially for distributed systems, leading to increased module production, and the shift in H1 domestic supply-demand balance towards tight supply. Modules stockpiled at low prices, resulting in a rapid increase in trading volume. Glass prices are expected to fluctuate upward in the future.

High-Purity Quartz Sand: This week, domestic high-purity quartz sand prices remained stable. Current market quotations are as follows: inner layer sand at 65,000-75,000 yuan/mt, middle layer sand at 35,000-45,000 yuan/mt, and outer layer sand at 19,000-25,000 yuan/mt. Prices remained steady. After the holiday, domestic market transactions were limited this week, as some sand enterprises had not fully resumed operations. Downstream crucible enterprises mainly consumed their own quartz sand inventory, resulting in average market transaction performance. With the improvement in PV demand, quartz sand demand is expected to rise slightly. However, imported sand prices may see negotiated reductions, weakening support for domestic sand prices, which are expected to remain stable for now.

Backsheet Weekly Review: This week, the price range for PV backsheets narrowed. The market price for white CPC backsheets with double fluorine coating was around 4.9-5.1 yuan/m², while transparent CPC backsheets with double fluorine coating were priced at 11.2-12.3 yuan/m². Backsheet orders were limited this week, and most manufacturers maintained firm quotations, with most prices stable at 5 yuan or above. Some manufacturers even quoted as high as 5.5 yuan, but transaction prices remained at the low level of around 5 yuan. By mid-February, backsheet manufacturers had limited orders on hand, and the expected monthly production schedule for February was low. Most manufacturers anticipated a production schedule over 30% lower than in January. The overall industry production and operation continued to weaken, with February's industry operating rate expected to be only around 6%, down from January's 10%. Pessimistic sentiment among backsheet manufacturers persisted.

》View SMM PV Industry Chain Database

![Silicon Metal Market in Stagnant Consolidation, Wafer In-Factory Inventory Gradually Accumulating [SMM Silicon-Based PV Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/rgviL20251217171740.jpg)

![[SMM PV Flash News] SEG Solar's Third Manufacturing Facility Bringing Annual Manufacturing Capacity to 10.6 GW](https://imgqn.smm.cn/usercenter/HKFoG20251217171742.jpg)

![[SMM PV] A Sneak Peek at SNEC PV Materials Exhibition Booths!](https://imgqn.smm.cn/usercenter/WUJtg20251217171743.jpg)