I. Price Review

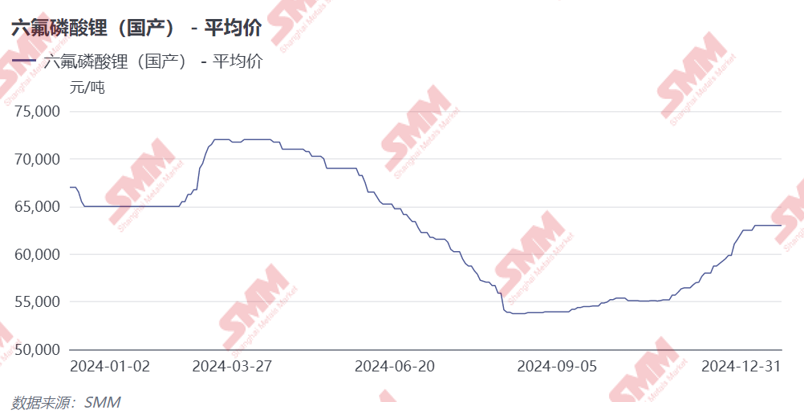

In terms of prices, according to historical quotations from the SMM survey, the spot price of LiPF6 showed an overall downward trend in 2024, with occasional increases in Q1 and Q4.

From late February to March, LiPF6 prices rose significantly. The main reasons for this were the rising costs of LiPF6's raw materials—lithium carbonate and lithium fluoride—which provided strong cost support, as well as the gradual recovery in demand after the Chinese New Year. The sharp increase in costs significantly boosted LiPF6 prices. During this period, downstream lithium battery enterprises experienced robust demand, with strong sentiment for stockpiling. The operating rate of LiPF6 enterprises increased significantly, and production continued to rise.

Starting from mid-to-late April, as lithium carbonate prices continued to decline, cost support weakened. Coupled with the gradual saturation of downstream stocking demand and the release of production capacity by producers, the market gradually shifted to an oversupply situation, and LiPF6 prices entered a downward trajectory.

From May to August, lithium carbonate prices continued to decline due to the slowing growth in downstream demand and the persistent oversupply situation. As a key raw material for LiPF6, the falling price of lithium carbonate continued to drag down LiPF6 prices. Additionally, the continuous release of new LiPF6 capacity and some enterprises' strategies to expand market share exacerbated the oversupply of LiPF6, leading to further price declines.

In September, the lithium carbonate market was significantly affected by substantial production cuts by top-tier lithium chemical plants in Jiangxi, which led to a notable impact on downstream supply. Combined with the continuous increase in downstream production schedules and widespread pre-holiday stockpiling for the National Day, the decline in spot prices slowed, accompanied by fluctuations and rebounds. The rebound in lithium carbonate prices prompted LiPF6 producers to frequently adjust their prices, resulting in an increase in LiPF6 prices.

In October, although lithium carbonate prices fluctuated downward after the National Day holiday, LiPF6 prices were not significantly affected. According to the SMM survey, at the beginning of October, LiPF6 prices slightly increased due to the high prices of lithium fluoride. Although lithium fluoride prices began to decline in mid-October, LiPF6 sellers maintained a strong sentiment to stand firm on quotes, keeping prices relatively stable. By month-end, influenced by the rising prices of anhydrous hydrogen fluoride and phosphorus pentachloride, LiPF6 prices slightly increased. Overall, LiPF6 prices showed an upward trend in October.

In November, the prices of LiPF6's raw materials, lithium carbonate and lithium fluoride, continued to rise, coupled with the strong sentiment of LiPF6 enterprises to stand firm on quotes, leading to a significant rebound in LiPF6 prices. Additionally, downstream demand remained robust in November, with the demand for LiPF6 from the electrolyte sector continuing to increase. The operating rate in this industry also rose accordingly, and the market supply-demand balance improved. Some LiPF6 enterprises reached full-capacity production to meet downstream demand. Against this backdrop of supply-demand balance, combined with the rebound in upstream raw material prices, LiPF6 prices rose sharply, with a 6.7% increase in November.

In December, although the price of lithium carbonate, one of the raw materials for LiPF6, began to pull back, lithium fluoride prices remained high, providing continued cost support for LiPF6. Additionally, downstream demand remained robust, driving increased demand for LiPF6. As a result, LiPF6 spot prices continued to rise MoM in December. As of December 31, 2024, the spot price of LiPF6 rose to 62,000–64,000 yuan/mt, with an average price of 63,000 yuan/mt, down 4,000 yuan/mt from the year-end price of 67,000 yuan/mt in 2024, representing an annual decline of 6.35%.

II. Production Review

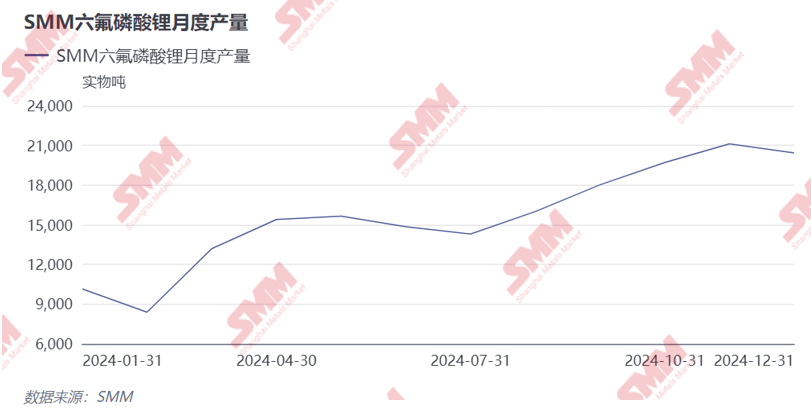

In 2024, China's LiPF6 production reached 187,000 mt, up 45% YoY.

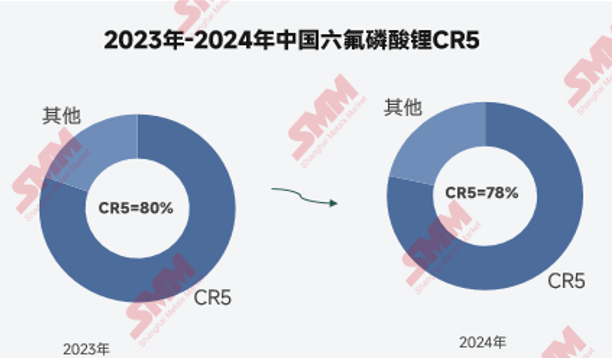

Due to the continuous capacity expansion and production increase by small and medium-sized enterprises over the past year, which entered the market with lower prices, market competition became more intense. As a result, the market share of top-tier enterprises slightly declined under the impact of these aggressively entering SMEs. However, the top five structure in the electrolyte market did not undergo significant changes.

III. 2025 Outlook

Demand side, China remains the main driving force in the power and ESS sectors. In the power market, the Central Political Bureau held a meeting on December 9, indicating that the policy environment will remain favorable through 2025, which will benefit the healthy and sustainable development of the automotive industry. Additionally, as 2025 marks the final year of the 14th Five-Year Plan, consumer car purchase demand is expected to further increase. Therefore, SMM expects a relatively optimistic outlook for car sales in 2025. Meanwhile, supported by policies, the ESS market is also expected to continue achieving significant progress.

Supply side, as the end-use market is expected to maintain growth, LiPF6 prices are likely to receive some support. It is anticipated that LiPF6 production will gradually increase with the release of capacity from LiPF6 plants, maintaining a slightly surplus outlook, with a growth rate of approximately 26%.

Note: For any additional details or corrections regarding the content mentioned in this article, please feel free to contact us at the following:

Tel: 021-20707842 (or add WeChat as below) Ren Xiaoxuan, thank you!

SMM New Energy Research Team

Cong Wang 021-51666838

Lingying Zhang 021-51666775

Xiaodan Yu 021-20707870

Rui Ma 021-51595780

Ying Xu 021-51666707

Disheng Feng 021-51666714

Yujun Liu 021-20707895

Yanlin Lv 021-20707875

Xianjue Sun 021-51666757

Ye Yuan 021-51595792

Chensi Lin 021-51666836

Zhicheng Zhou 021-51666711

![[SMM Weekly Manganese Ore Review] Initial Overseas Market Offers Raised, Intensifying the Tug-of-War Between Strong Expectations and Weak Reality in the Manganese Ore Market](https://imgqn.smm.cn/usercenter/IpglC20251217171727.jpg)