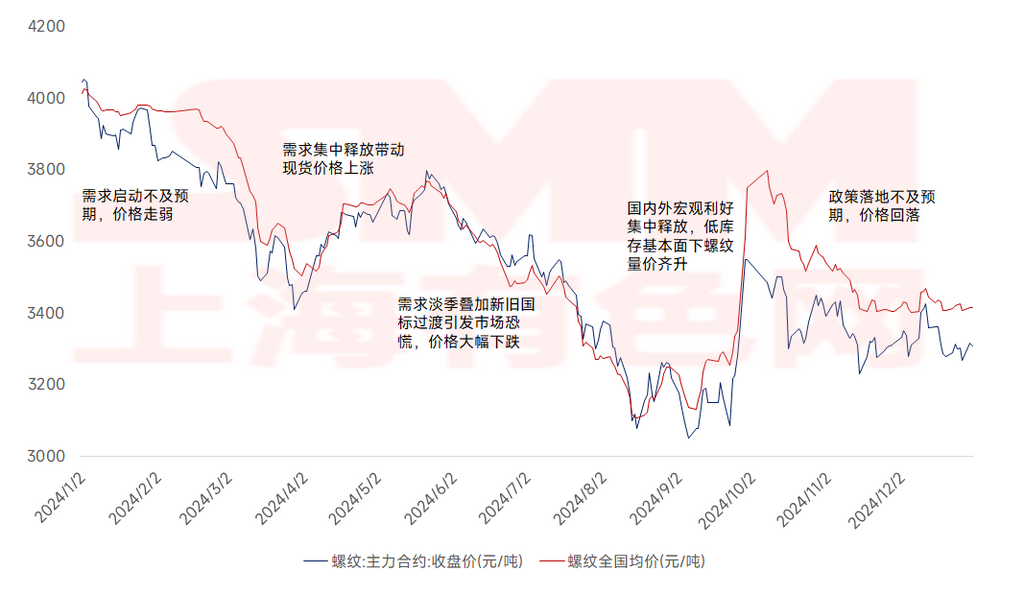

Reviewing 2024, affected by weak end-use demand and overcapacity, the national average rebar price fluctuated downward, with the overall price center shifting lower. Specifically, the national average rebar price in 2024 was 3,575 yuan/mt, down 322 yuan/mt from 2023, representing a YoY decline of 8.26%. The national rebar price trend in 2024 can be roughly divided into five phases: Phase 1 (January-March), demand recovery fell short of expectations, leading to weaker prices; Phase 2 (April-May), concentrated demand release drove spot price increases; Phase 3 (June-mid-September), entering the off-season for demand, coupled with market panic triggered by the transition between old and new national standards, spot prices dropped significantly to the annual low; Phase 4 (late September-early October), concentrated release of domestic and international macro favourable policies, with low inventory fundamentals driving both volume and price increases for rebar; Phase 5 (October-December), policy implementation fell short of expectations, combined with significantly weaker winter stockpiling enthusiasm compared to previous years, prices pulled back and fluctuated rangebound.

Figure 1 National Average Rebar Price Trend in 2024

Phase 1 (January-March): The "Golden March" peak season demand fell short, coupled with Two Sessions policies not exceeding expectations, leading to weaker spot prices. On the macro front, the Two Sessions did not introduce any policies exceeding expectations, resulting in insufficient market confidence. On the fundamentals side, futures prices declined, downstream procurement was cautious, and the resumption of construction in many inland areas was slower than expected, leading to weaker-than-expected demand release. This caused pressure on both in-plant and social inventories, with spot prices under pressure and weakening.

Phase 2 (April-May): Concentrated demand release during the "Silver April" season drove spot price increases. In April, the eighth round of coke price cuts was implemented, steel mills operated profitably, and blast furnace resumption activity increased, providing stronger support for ore prices. Additionally, new real estate projects increased slightly MoM, with funding and demand conditions significantly improving compared to March. This led to effective destocking of construction materials, driving spot price increases.

Phase 3 (June-mid-September): The off-season for demand, combined with the transition between old and new national standards, triggered market panic, leading to a significant drop in spot prices. Starting in late May, as the northern farming season and south China's rainy season arrived, the construction materials market entered the traditional off-season for demand. Additionally, construction site restrictions during the national college entrance exams further suppressed end-use demand, resulting in continuous inventory buildup for rebar and significant pressure on spot prices. On June 25, the new national standard for rebar was introduced. In east China, warehouses imposed requirements for the outflows from warehouses of old-standard resources within a limited period, prompting price reductions to avoid the risk of destocking difficulties during the off-season. This exacerbated market panic, accelerating the decline in rebar spot prices to the annual low.

Phase 4 (late September-early October): With low inventory fundamentals and concentrated release of domestic and international macro favourable policies, rebar volume and price increased. On the fundamentals side, the continuous decline in spot prices significantly reduced steel mill profits, with rebar production losses generally ranging from 150-200 yuan/mt. Many steel mills proactively conducted maintenance and production cuts. Thanks to the rapid decline in production and the arrival of the "September-October peak season," rebar destocking accelerated, and fundamentals improved significantly. On the macro front, the US Fed implemented its first interest rate cut, and domestic macro favourable policies were introduced, including lowering central bank policy rates, reducing mortgage rates on existing home loans, and emphasizing "stabilizing the real estate market, strictly controlling new supply, optimizing existing supply, improving quality, and increasing loans for white-listed projects." This series of favourable information shifted market sentiment from pessimistic to highly optimistic. Combined with the support of low inventory fundamentals, rebar prices achieved a strong rebound, recovering nearly half a year's losses within just one week.

Phase 5 (mid-October-December): Policy implementation fell short of expectations, combined with significantly weaker winter stockpiling enthusiasm compared to previous years, leading to price pullbacks and rangebound fluctuations. After the National Day holiday, multiple meetings fell short of expectations, cooling capital market sentiment. Producers were eager to sell and realize profits, causing rebar prices to pull back. After November, the US presidential election and domestic debt resolution policies were successively implemented, shifting market expectations to neutral. The macro perspective temporarily entered a vacuum period, with valuations returning to fundamentals. On the supply side, environmental protection inspections and routine winter maintenance kept steel mill construction material production relatively low, resulting in relatively small overall supply pressure. On the demand side, the construction materials market entered the off-season in Q4. Northern projects nearly halted due to cold wave weather, and winter stockpiling enthusiasm was weaker than in previous years. Overall, the rebar market experienced weak supply and demand, with inventory remaining low. Fundamental imbalances were not prominent, and spot prices fluctuated rangebound.

Looking ahead to 2025, on the demand side, rebar's primary downstream demand comes from construction steel, closely tied to real estate and infrastructure. In 2024, China's real estate policies were further relaxed, but the actual effects were not significant. Real estate market data, from sales to new starts, continued to deteriorate, making it difficult to claim a bottom has been reached, with further downside room. However, considering the low base of new real estate starts this year, the decline in new starts is expected to narrow in 2025. The infrastructure sector, under the pressure of debt resolution and changes in investment structure, is likely to see limited growth, making it difficult to offset the weakness in real estate steel demand. Therefore, in 2025, rebar demand is highly likely to remain weak. Against the backdrop of continued declines in end-use demand, steel mill profits may shrink further, leading to passive production cuts for rebar. Overall, rebar is expected to continue the weak supply and demand pattern in 2025. With ample raw material supply, cost support for rebar is likely to remain unstable, and the price center may shift further downward.

![[SMM Steel] AGSI launches new rebar mill in UAE, adds 600,000 mt capacity](https://imgqn.smm.cn/usercenter/JSngP20251217171719.jpg)

![[SMM Steel] Vietnam domestic demand offsets export weakness amid trade barriers](https://imgqn.smm.cn/usercenter/VhIgs20251217171719.jpg)

![[SMM Steel] Marcegaglia to invest €1 billion in new French steel plant](https://imgqn.smm.cn/usercenter/FFFrV20251217171719.jpg)