SMM, January 2:

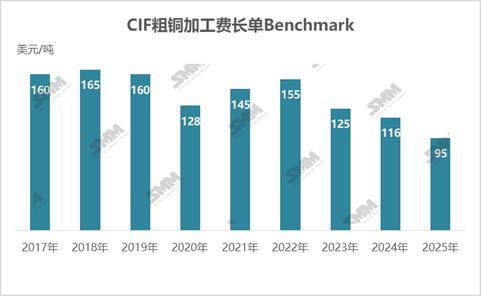

According to SMM, CNMC International Trading Co. Ltd. and Jiangxi Copper Corporation (JCC) finalised the 2025 CIF imported blister copper RC benchmark at $95/mt on the afternoon of December 31, 2024, Beijing time. This RC is $21/mt lower than this year's $116/mt and marks the first time in recent years that it has fallen below the three-digit level.

The decline in the 2025 imported blister copper RC long-term contract benchmark does not seem to surprise the market; however, the drop below the three-digit level highlights concerns about the blister copper market in 2025. Due to tight copper concentrate raw material supply in 2024 and the commissioning of expanded smelting capacity in Southeast Asia, with some supplies diverted overseas, China's cumulative imports of copper anode from January to November 2024 were only 815,800 mt, down 14.23% YoY. The annual import volume is expected to fall below 900,000 mt.

Against the backdrop of a global contraction in copper concentrate supply in 2024, smelters faced tight raw material supply and significant losses in producing with spot copper concentrates. This prompted smelters to actively seek alternative and supplementary raw materials, increasing attention on the copper anode market. On December 6, 2024, Jiangxi Copper Corporation, China Copper, Tongling Nonferrous, Jinchuan Group, and Daye Nonferrous finalised the 2025 copper concentrate long-term contract TC benchmark at $21.25/mt and 2.125¢/lb. The 2024 copper concentrate TC long-term contract benchmark was $80/mt and 8.0¢/lb. This result directly influenced the negotiations for imported blister copper long-term contracts, providing upstream suppliers with sufficient confidence to stand firm on quotes.

From the perspective of overseas copper anode supply, the 500,000 mt blister copper smelting project at the Kamoa-Kakula mine in the DRC is expected to ramp up production gradually in H2 2025. However, fundamentally, this involves the transfer of copper concentrate raw materials. Disruptions caused by further shortages of copper concentrate raw materials make achieving blister copper capacity growth targets challenging, potentially leading to a decline in global blister copper production and an expanded gap with actual refined capacity.

Therefore, the overall raw material situation in 2025 poses significant challenges for smelters, with secondary copper raw materials and recycled anode copper becoming key variables.

![Middle East Conflict Uncertainty Dragged Down Copper Prices, BC Copper Closed Down 0.56% Intraday [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/CaDcj20251217171711.jpg)