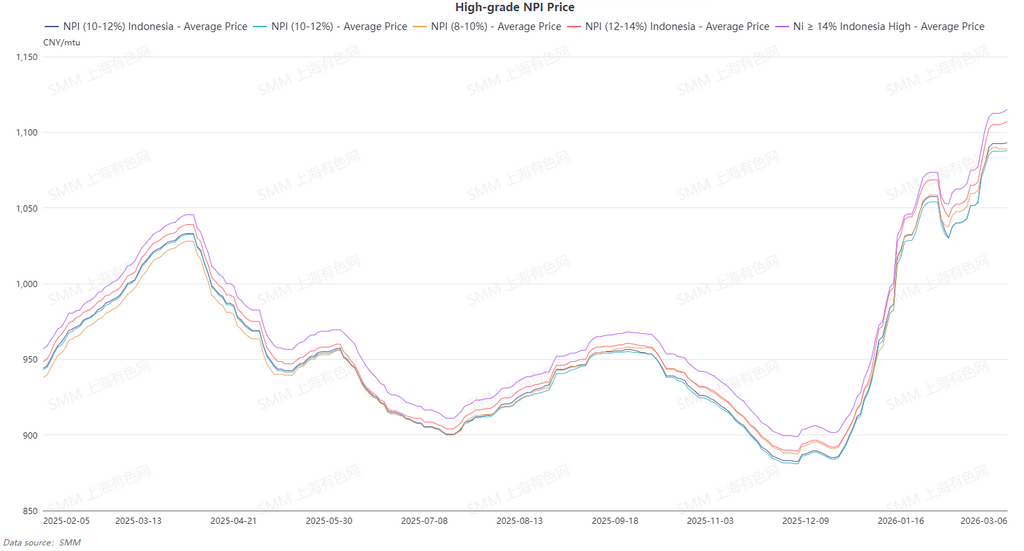

The average price of SMM 10-12% high-grade NPI rose 21.1 yuan/nickel unit WoW to 1,092.6 yuan/nickel unit (ex-factory, tax included). The average price of the Indonesia NPI FOB Index rose $2.22/nickel unit WoW to $138.54/nickel unit. As the holiday atmosphere gradually faded, downstream steel mills resumed operations one after another, and high-grade NPI trading volume gradually increased.

Supply side, supported by strong costs this week, smelters kept their offers firm; however, a small number of traders shipped at low prices to recover cash, resulting in wide differences in market quotations. Demand side, after the holiday, gains in stainless steel finished-product prices were limited, and steel mills showed weak acceptance of high-priced high-grade NPI. The economic substitutability of steel scrap strengthened, and most steel mills only maintained small volumes of just-in-time procurement. Overall, strong cost support combined with still-tight deliverable supply—especially the clear scarcity of high nickel unit material—kept high-grade NPI prices rising. Looking ahead, as costs are unlikely to fall and demand is expected to recover, high-grade NPI prices are expected to still have upside room.

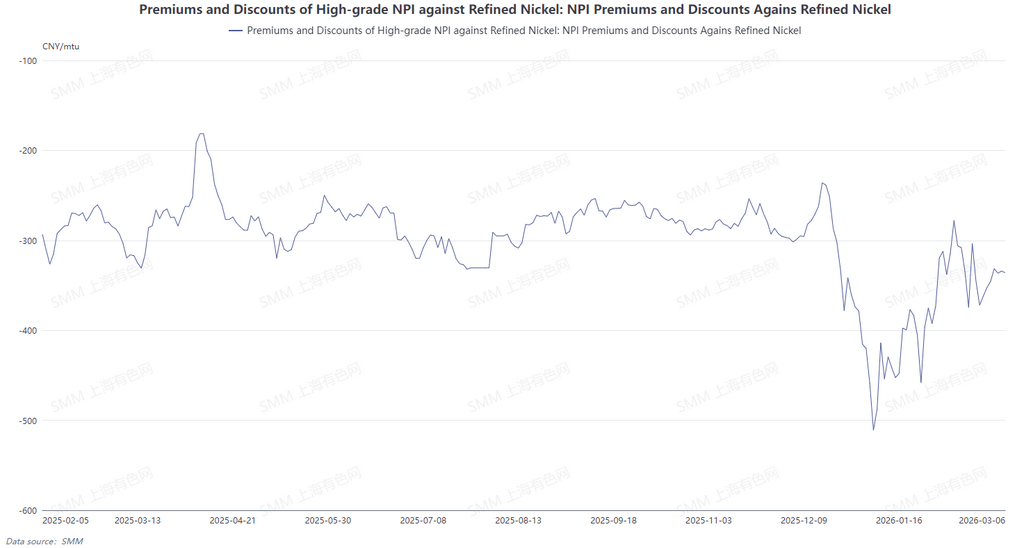

From the perspective of the conversion of NPI to high-grade nickel matte, refined nickel prices pulled back after the holiday while high-grade NPI prices stayed elevated, and the average discount of high-grade NPI versus refined nickel narrowed to 336.7 yuan/nickel unit. High-grade NPI prices are expected to still have upside room next week, while refined nickel prices are expected to decline MoM. The average discount of high-grade NPI versus refined nickel is expected to continue narrowing; however, supported by new energy orders, the conversion of NPI to high-grade nickel matte still has momentum.

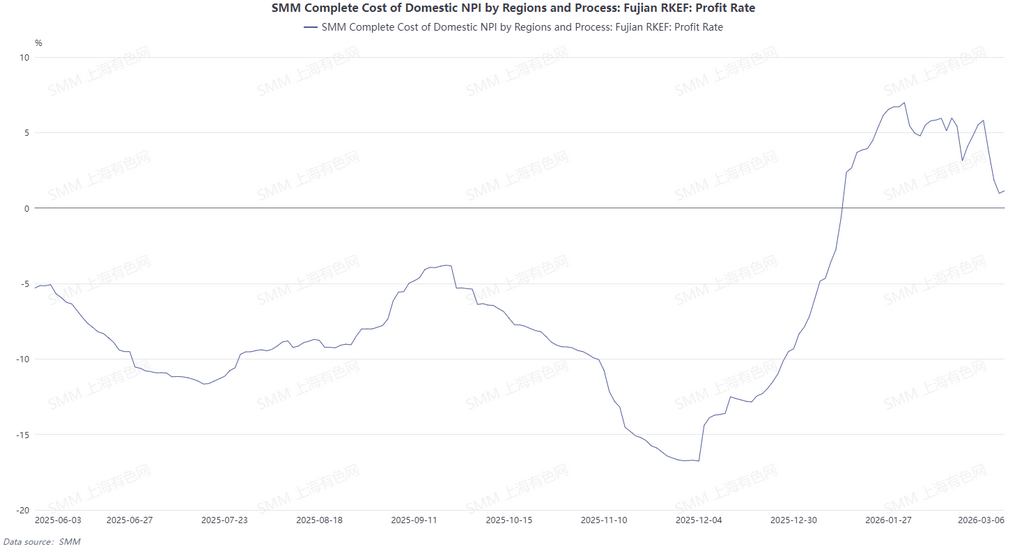

Based on the cash cost of high-grade NPI calculated using ore prices from 25 days ago, smelter profits for high-grade NPI continued to shrink this week. Raw material side, ore costs continued to rise, keeping high-grade NPI production costs on an upward trend. Meanwhile, the pace of high-grade NPI price increases slowed, weighing on smelter margins. Looking ahead, raw material side, ore prices remain more likely to rise than fall, and overall production costs are expected to continue increasing, with smelter cost pressure expected to intensify.

![[SMM Stainless Steel Market Flash] Scrap Surge and Geopolitics Raise Cost Pressure on EU Mills](https://imgqn.smm.cn/usercenter/WYeHX20251217171733.jpg)

![[SMM Stainless Steel Market Flash] European Mills Lift July CRC Offers to €2,700/t Delivered](https://imgqn.smm.cn/usercenter/CjEnN20251217171733.jpg)

![[SMM Stainless Steel Market Flash] European Stainless Flats Keep Rising as Sentiment Stays Cautious](https://imgqn.smm.cn/usercenter/biBGl20251217171733.jpg)