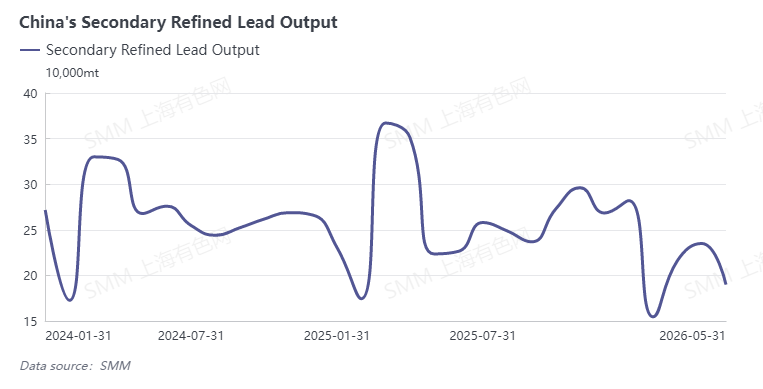

In May 2026, China's secondary lead production declined significantly, down 18.96% MoM and 9.26% YoY, while secondary refined lead pulled back 19.16% MoM and 15.03% YoY.

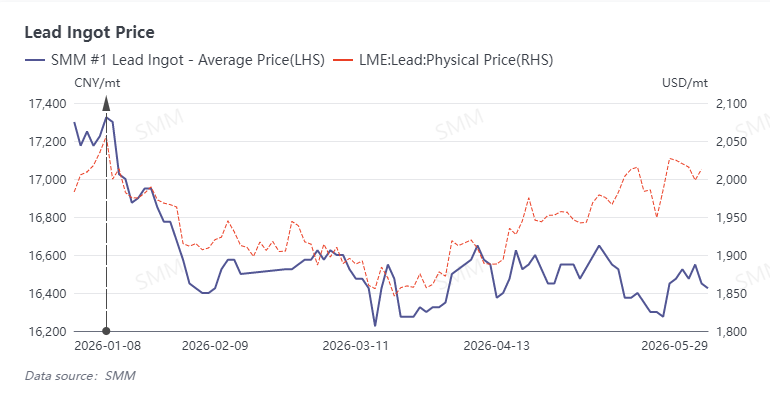

According to SMM data, spot lead prices were in the doldrums in May, with the SMM #1 lead ingot monthly average price at approximately 16,475 yuan/mt. Coupled with the downstream battery sector entering the traditional off-season, just-in-time procurement in the market was sluggish and finished product inventories were piling up, continuously intensifying losses at smelters.

Supply side, four large smelters in east China, north China, and northwest China halted production for maintenance, while seven medium-to-large enterprises also implemented phased production cuts for maintenance. This round of capacity contraction was mainly driven by operating losses, raw material shortages, and sluggish finished product sales, with only a few enterprises shutting down due to equipment failures.

Entering June, enterprises that previously underwent maintenance are gradually returning to normal production. A large smelter in Anhui has already started furnace preheating and is expected to commence production in the first ten days of the month; multiple enterprises in east China and northwest China plan to resume production in mid-to-late June. Based on market analysis, lead prices in June are expected to move sideways within the range of 16,400–16,900 yuan/mt, with high scrap battery prices underpinning lead prices, though weak off-season demand will still cap upside potential. SMM estimates that secondary lead production in June will increase by approximately 40,000 mt, but whether this incremental volume can be fully realized will depend on raw material supply and the impact of lead price trends on production willingness.

![Rising China Supply Combined with Ex-China Inventories at 13-Year High Limits Upside Momentum for Lead Prices [SMM Lead Market Weekly Forecast]](https://imgqn.smm.cn/usercenter/msNEk20251217171722.jpg)

![Intraday lead prices edged up before fluctuating and pulling back, eventually closing with a doji [Lead Futures Brief]](https://imgqn.smm.cn/usercenter/qnyHQ20251217171721.jpeg)

![As the Half-Year Period Approaches, Some Battery Enterprises Intend to Increase Production [SMM Lead-Acid Battery Weekly Operating Rate Comment]](https://imgqn.smm.cn/usercenter/bAjSC20251217171721.jpg)