As the sodium-ion battery scaling and commercialization process continues to accelerate, industry dividends are being released at a faster pace in 2026. April, as a key period at the start of Q2, saw a notable recovery in the sodium-ion battery cathode and anode materials market. Demand-side stockpiling willingness increased, capacity expansion pace accelerated, product mix differentiation became more prominent, and the industry as a whole moved toward a positive supply-demand synergy.

I. Cathode Materials: Stockpiling Heats Up Ahead of Peak Season, NFPP Becomes Core Growth Driver

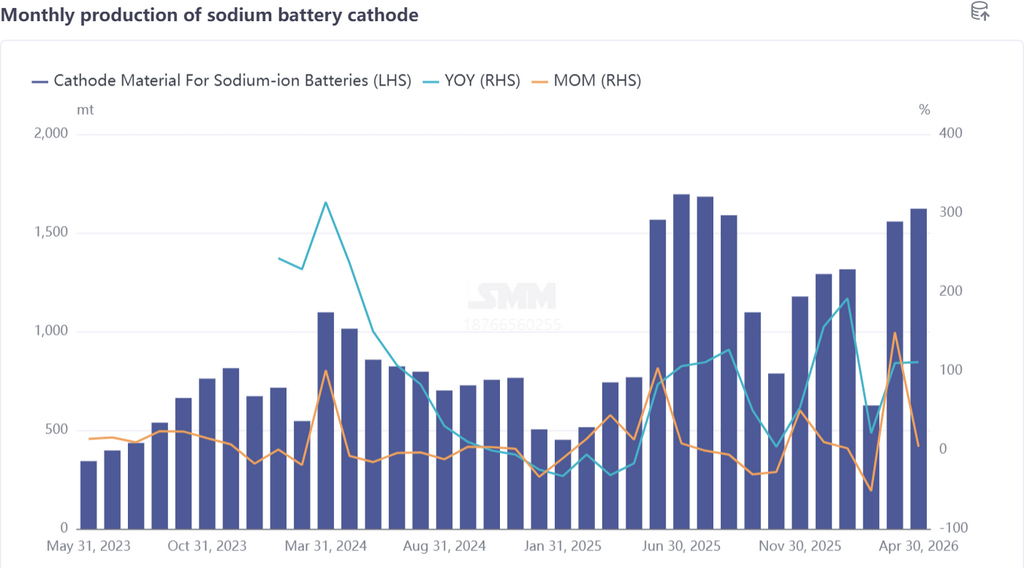

In April, sodium-ion battery cathode material demand recovered with a strong stockpiling atmosphere, and production achieved growth both YoY and MoM. SMM data showed that monthly production edged up 4% MoM and was up 111% YoY, demonstrating strong growth momentum.

In terms of product mix, polyanion materials held an absolute dominant position, accounting for nearly 82% of the total, up 5 percentage points MoM, with their excellent performance meeting the needs of energy storage and start-stop systems. Among them, NFPP (sodium iron phosphate pyrophosphate) performed outstandingly, becoming the core growth driver.

Demand side, NFPP pre-purchase intent orders increased significantly in April, mostly for May-June delivery. Shipments had already begun by month-end April, and NFPP enterprises are expected to see a mini shipments peak in Q2. In contrast, layered oxide cathode production declined. Except for integrated enterprises, most enterprises faced precursor undersupply — previously, due to weak layered oxide demand and insufficient cost-effectiveness, most precursor enterprises had switched their production lines back to ternary materials, making it difficult to quickly fill the supply gap.

Notably, high-compaction NFPP products are highly dependent on precursors, but current NFPP precursor capacity is severely insufficient and prices have been raised, driving up high-compaction NFPP costs. As the sodium-ion battery market is still in its development phase, downstream battery cell manufacturers maintain strict cost control, and NFPP price raises may face resistance. In April, demand was released from start-stop, two-wheeled vehicle, and ESS sectors, supporting the cathode market. Looking ahead to May, cathode production is entering peak season, and new battery cell capacity release is expected to drive dual growth in supply and demand, with production forecast to increase 19% MoM and 23% YoY.

II. Hard Carbon Anode: Production Surge Fills Gap, Accelerated Expansion Breaks Bottleneck

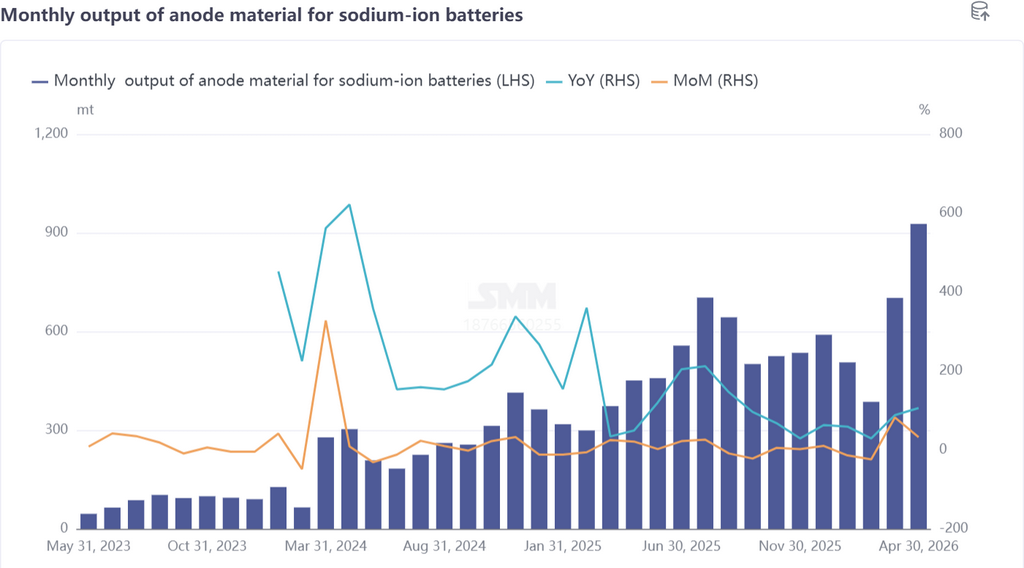

The sodium-ion battery hard carbon anode market delivered a strong performance in April, with production growing significantly as enterprises accelerated expansion to fill the supply-demand gap. According to SMM data, sodium-ion battery anode production was up 32% MoM and up 108% YoY, with hard carbon as the mainstream material seeing particularly notable production growth. Recently, new hard carbon capacity has come online, and subsequent capacity ramp-up is expected to gradually alleviate the capacity shortage that previously constrained sodium-ion battery development.

Previously, hard carbon had become a core bottleneck for sodium-ion battery development due to insufficient capacity and inconsistent product quality. Currently, downstream demand is concentrated among leading major

manufacturers, with the large-scale energy storage sector seeing rapid demand growth and imposing stringent requirements on hard carbon performance (long cycle life and low-temperature performance), driving up high performance hard carbon prices. Robust demand has fueled rapid growth in intended hard carbon orders, with some enterprises in the capacity ramp-up stage and others planning new capacity. Production schedule for hard carbon is expected to further increase in May, with production up 16% MoM and up 134% YoY.

III. Market Summary and Outlook: Improving Supply and Demand, Q2 Entering a Key Growth Period

Overall, the sodium-ion battery cathode and anode markets in April exhibited a pattern of "recovering demand, accelerating capacity, and structural differentiation." On the cathode side, polyanion materials maintained a solid dominant position, with NFPP leading growth, while layered oxide declined due to cost-performance constraints. Meanwhile, insufficient NFPP precursor capacity and rising costs remained short-term pain points. On the anode side, hard carbon production surged, new capacity coming online alleviated supply gaps, large-scale energy storage demand boosted high-end product demand, and accelerated expansion broke through bottlenecks, confirming the continued advancement of sodium-ion battery commercialization.

Q2 is expected to usher in a key growth period for the industry. Cathode side, the peak season arrives in May, with new battery cell capacity release driving demand growth. NFPP is expected to see a minor shipments peak, though attention should be paid to precursor supply and cost pressure. Anode side, hard carbon capacity ramp-up continues, the supply-demand pattern keeps improving, and product performance iteration is accelerating to adapt to high-end scenarios.

In the long term, as sodium-ion battery commercialization accelerates and downstream application scenarios continue to expand, cathode and anode demand will sustain capacity expansion. The industry is expected to gradually resolve capacity and cost pain points, optimize product structure, and consolidate the mainstream positions of polyanion cathodes and hard carbon anodes, driving the sodium-ion battery industry toward large-scale, high-quality development.

![[Energy Storage: General Motors And US Energy Storage Company Develop Sodium-Ion Battery Technology]](https://imgqn.smm.cn/usercenter/wzbHd20251217171731.jpg)