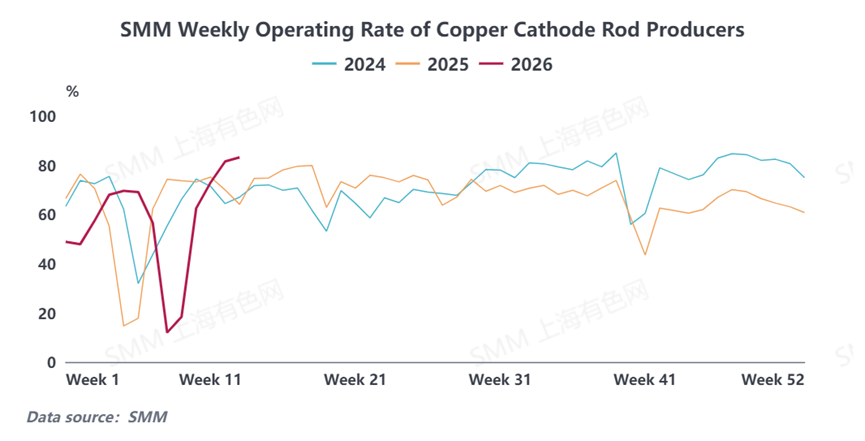

After the Lantern Festival, the operating rate of copper cathode rod was the first to rebound continuously, driving a gradual recovery in downstream consumption and pushing social inventory to officially enter a destocking channel from mid-March. However, as copper prices have recently rebounded and risen, downstream procurement sentiment has become more cautious, the pace of destocking has slowed somewhat, and the growth in the operating rate of copper cathode rod has also narrowed accordingly.

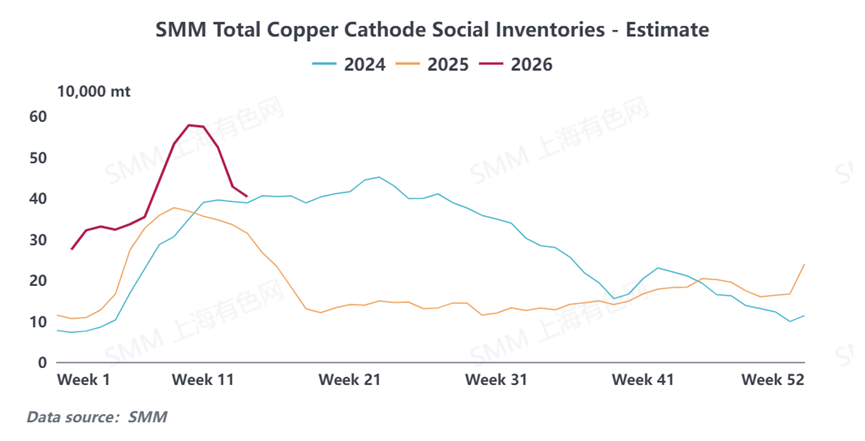

Operating Rates Rose First, and the Inventory Inflection Point Emerged as Expected

After the Chinese New Year, copper prices pulled back in phases, effectively boosting downstream restocking willingness. According to SMM, the operating rate of copper cathode rod enterprises was the first to respond, showing a WoW upward trend for several consecutive weeks. As of the latest data, the operating rate of copper cathode rod enterprises further climbed to 83.17, reflecting the continued release of end-use demand.

Driven by the continued rise in operating rates, downstream procurement gradually increased in volume, and rigid-demand orders were steadily placed. As a result, copper inventories in major regions nationwide ended their sustained inventory buildup on March 12, officially marking an inflection point in inventories. Thereafter, the degree of destocking increased week by week, and as of March 26, inventories had declined for three consecutive weeks. With inventories being digested rapidly, the increase in total inventories compared to the same period last year also gradually narrowed from the post-holiday high to 92,900 mt.

By region, this round of destocking showed broad-based characteristics. Consumption in Guangdong recovered most notably, coupled with localized tightening on the supply side, and the pace of inventory decline was relatively fast, making it the first to establish a destocking trend; driven by downstream consumption, warehouse withdrawals in Shanghai continued to exceed warehouse inflows, and against the backdrop of normal arrivals of imported and domestic cargoes, inventory steadily pulled back; Jiangsu likewise benefited from the recovery in consumption, jointly driving the rapid drawdown of overall inventory.

Copper Price Rebound Curbed Willingness to Chase Gains, Destocking Momentum Weakened Significantly

Entering late March, market sentiment shifted. As copper prices rose, downstream enterprises became more cautious, and the previously more active procurement pace slowed down. As of March 30, copper inventories in major regions nationwide fell 13.81% WoW. Although the destocking trend continued, the single-week decline had narrowed from 14.54% in the previous week.

Regional performance also diverged. In Shanghai, arrivals of imported and domestic cargoes were normal, downstream consumption continued to recover, and inventory steadily destocked; in Guangdong, consumption remained highly robust, and coupled with tight supply, the inventory decline was still considerable; however, in Jiangsu, affected by another rise in copper prices, downstream procurement turned more wait-and-see, the pace of destocking slowed markedly, reflecting that the restraining effect of rebounding prices on demand had begun to emerge.

Meanwhile, the upward momentum in the operating rate of copper cathode rod cooled somewhat. SMM expected the operating rate of copper cathode rod to rise to 83.76% this week, up only 0.59 percentage points WoW, in contrast to the pattern of consecutive sharp increases in previous weeks, indicating insufficient willingness among downstream buyers to chase higher prices, with more shifting to just-in-time procurement and adopting a wait-and-see stance toward subsequent copper prices.

Market Outlook: Short-Term Destocking Continues as Momentum Gradually Weakens

Overall, supply side, imported cargoes continued to arrive, while arrivals of domestic cargoes were relatively limited due to maintenance and other factors, and the overall pattern of tight supply persisted; demand side was more heavily affected by fluctuations in copper prices, with downstream players holding a wait-and-see attitude toward subsequent price trends, making it difficult in the short term to replicate the intensity of the previous concentrated restocking.

Social inventory is expected to continue destocking in the short term, but as copper prices remain at a relatively high level, downstream procurement is turning more rational, and destocking momentum is expected to weaken further. As for subsequent market direction, attention still needs to be paid to copper price trends and the actual fulfillment of end-user orders.

![Active Offerings of Forward-Month Delivery B/Ls, Trading Volume Pulled Back Significantly from the Previous Day [SMM Yangshan Spot Copper]](https://imgqn.smm.cn/usercenter/CJXfS20251217171710.jpg)

![Month-End Trading Was Sluggish, and SHFE Copper Spot Discounts Remained in the Doldrums [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/vcsIC20251217171710.jpg)