India’s steel industry has emerged as one of the fastest-growing major steel markets globally, supported by strong macroeconomic growth, infrastructure expansion, and accelerating industrialization. As the world’s second-largest steel producer and consumer, India continues to expand capacity while domestic demand, driven primarily by construction, manufacturing, and transportation, absorbs most of the incremental supply.

At the same time, trade policies such as safeguard and anti-dumping measures are reshaping import competition, while exports act as a balancing mechanism amid rising production. Looking ahead, the market is expected to remain broadly balanced in the short term, with demand growth largely keeping pace with supply. The long-term outlook remains structurally positive, given low per capita steel consumption and sustained policy support for infrastructure and industrial development.

Macro Environment: High Growth Meets a Structurally Under-Steeled Market

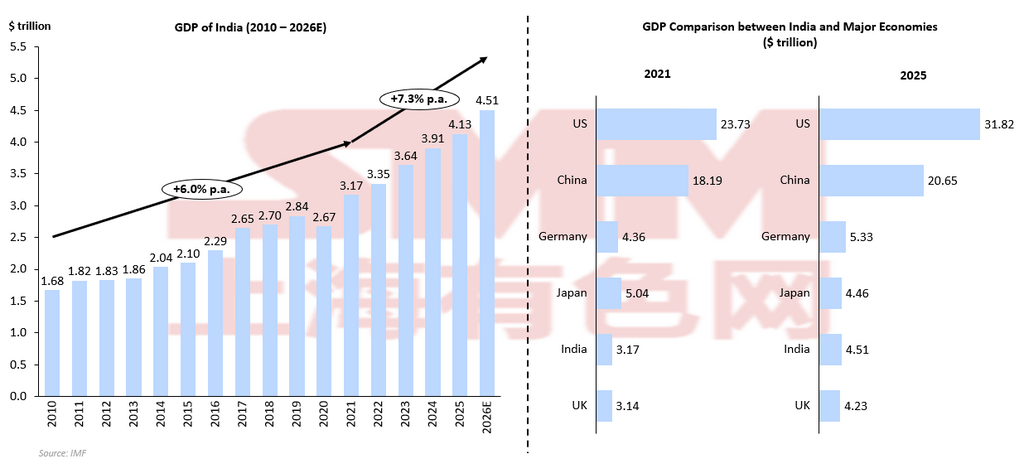

The Indian steel market continues to rest on one of the strongest macro backdrops among major economies, but the real point is not growth alone, it is the combination of high growth and low per-capita finished steel consumption.

Macro growth: India outpacing major economies:

-

India’s GDP is projected to grow ~7% in 2026E, higher than China (4.5%), United States (2.4%), EU (1.3%), and Japan (0.7%).

-

This positions India as one of the fastest-growing major economies and faster than China, the most relevant comparator for steel demand.

-

Strong macro growth provides a solid foundation for sustained steel consumption expansion.

Steel-intensive growth model:

-

India’s economic expansion remains infrastructure- and manufacturing-led, rather than service-driven.

-

Growth is closely tied to urbanization, industrialization, and physical asset creation, all of which are steel-intensive sectors.

-

This means GDP growth in India translates more directly into steel demand growth.

Policy-driven infrastructure spending:

-

The FY2026–27 Union Budget proposed ₹12.2 lakh crore in public capital expenditure, about +9% YoY.

-

Public capex supports steel demand through roads, railways, urban infrastructure, logistics, and industrial projects.

-

Fiscal spending therefore acts as a key transmission channel from macro growth to steel consumption.

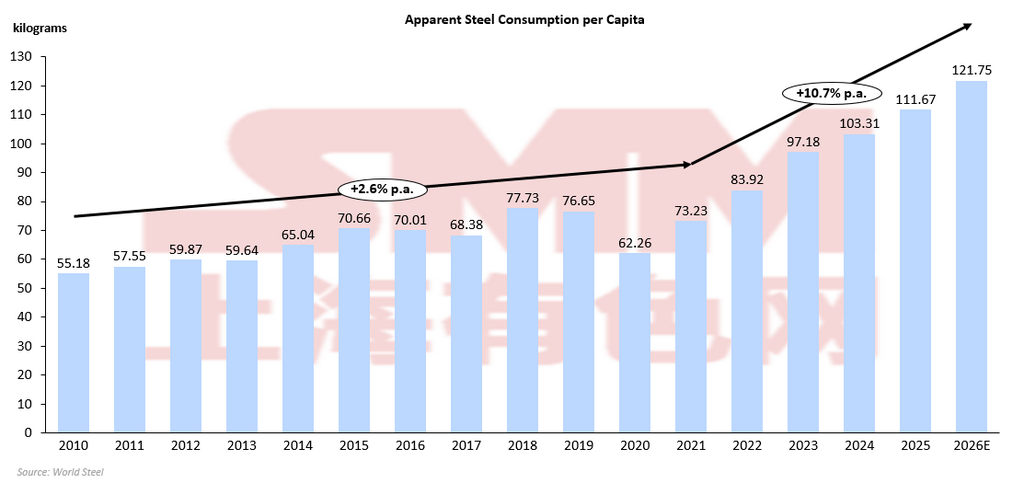

Per capita steel consumption gap:

-

India’s per-capita finished steel consumption was 103.31 kg in 2024, compared with 214.7 kg global average and 601.1 kg in China.

-

This indicates that India remains structurally under-steeled, even after years of growth.

-

The gap highlights significant room for long-term demand expansion.

Therefore, India matters to the global steel industry not simply because its economy is large and fast-growing, but because it combines above-peer GDP growth with still-low per-capita steel use. That gives the country both strong near-term momentum and long-term headroom. For steel producers, traders, and analysts, this means India should be viewed less as a mature cyclical market and more as one of the few large-scale markets where steel demand can continue to expand structurally for years, provided that domestic supply, pricing, and trade conditions remain supportive.

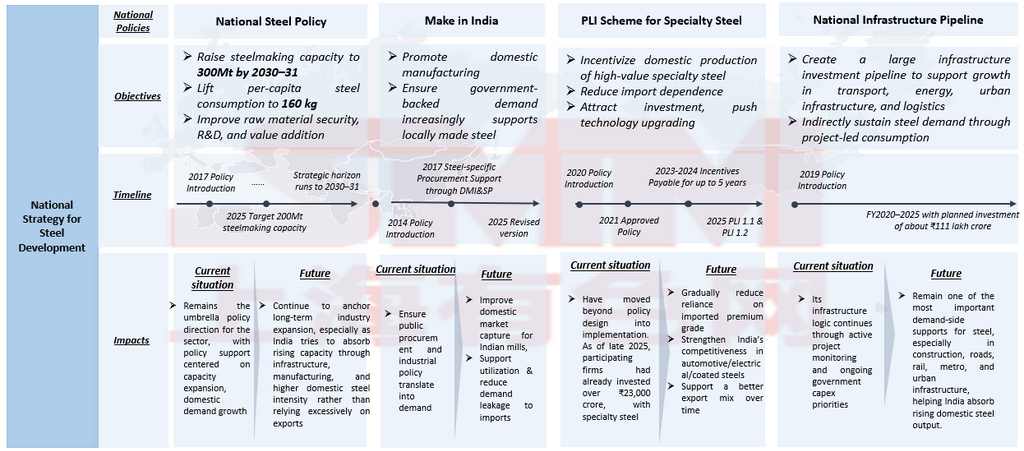

Policy Architecture: Trade Protection and Industrial Strategy Work Together to Support Domestic Steel

The Indian steel market is shaped not by a single policy, but by a layered policy framework combining demand creation, domestic capacity support, and import management. Rather than acting independently, these policies work together to ensure that India’s strong macro-driven steel demand is increasingly captured by domestic producers. The key policy frameworks are presented as the following table.

The national policies show that India’s steel strategy is not built on one lever alone. NSP 2017 sets the long-term industry direction, Make in India tries to ensure domestic demand benefits local producers, PLI for Specialty Steel upgrades the product mix and reduces high-grade import dependence, and NIP creates the steel-intensive demand base needed to absorb expanding capacity. The interaction of these policy layers is critical. Infrastructure and industrial policies increase steel demand, but without trade protection, part of that demand could be captured by imports. Beyond that, safeguard and anti-dumping measures therefore function as market-balancing tools, ensuring that domestic capacity expansion translates into higher utilization rather than intensified price competition from imported steel. In practical market terms, the introduction of safeguard duty reduces import competitiveness across flat steel categories, while anti-dumping measures prevent exporters from redirecting shipments through specific origins. BIS quality requirements further reinforce this framework by limiting entry of lower-grade material. Together, these policies shift the domestic steel market from an import-parity-driven pricing structure to one increasingly determined by domestic supply-demand fundamentals. This policy-driven shift is particularly important heading into 2026, when domestic supply is expected to continue rising. By reducing import pressure, the policy framework allows domestic mills to absorb incremental demand growth, while exports act as a secondary balancing mechanism.

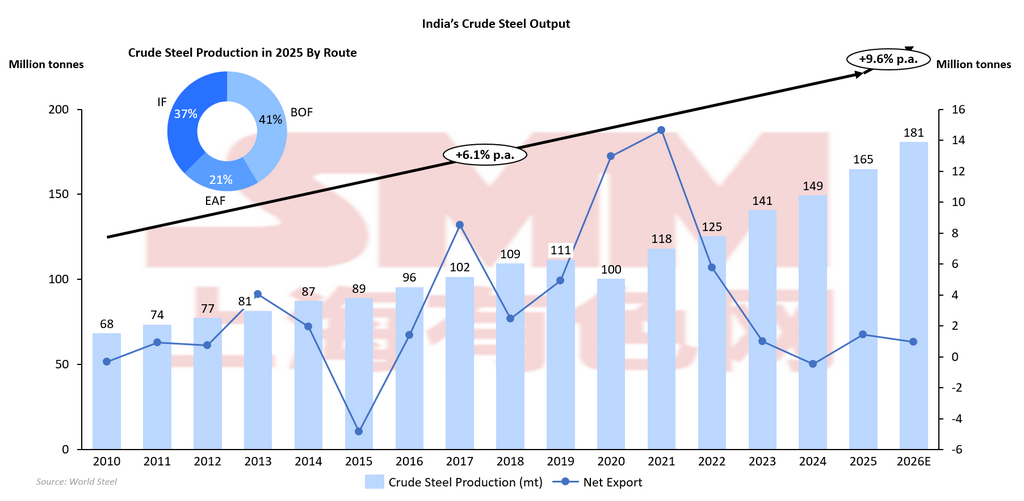

Supply Side: Capacity Expansion Continues, Raising the Importance of Utilization and Market Absorption

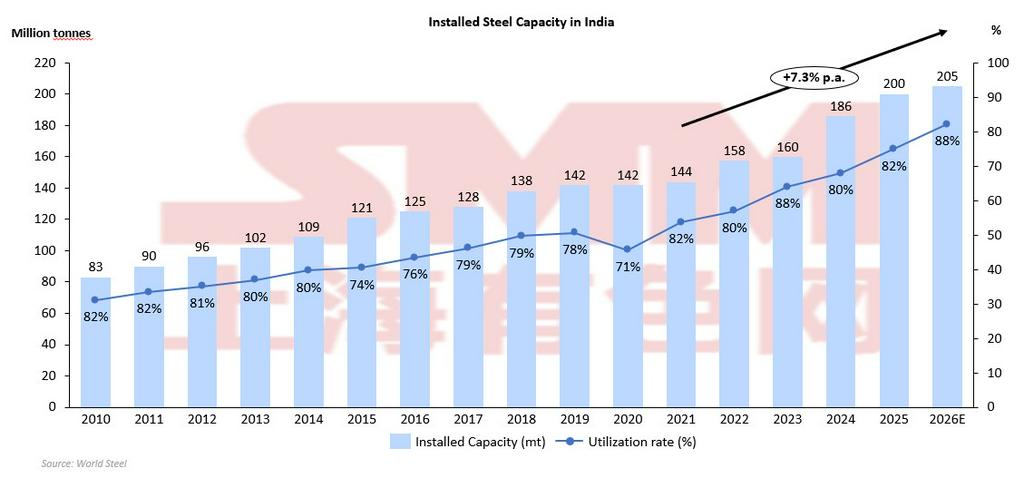

India’s supply-side dynamics are entering a critical phase in 2026E, where production capacity continues to expand steadily while utilization rates improve, reflecting stronger domestic absorption and reduced import pressure. India’s domestic crude steel capacity increased from 118 MTPA in 2021 to more than 205 MTPA by 2026E. At the same time, capacity utilization has trended upward from the low of about 70% range to around 88%, indicating that domestic mills are increasingly able to run at higher operating rates. This dual trend, rising production alongside improving utilization, suggests that supply growth has so far been broadly aligned with demand expansion, rather than creating significant overcapacity. However, the upward trajectory of utilization also highlights a structural shift. Earlier in the decade, capacity expansion often outpaced demand growth, resulting in underutilized assets. The recent improvement reflects stronger domestic demand, reduced import competition, and more disciplined production planning. This means India’s steel industry is transitioning from a phase of capacity buildup toward a phase where maximizing utilization becomes equally important. Higher utilization improves cost efficiency and supports margins, but it also increases the risk that additional supply could exceed demand if growth slows.

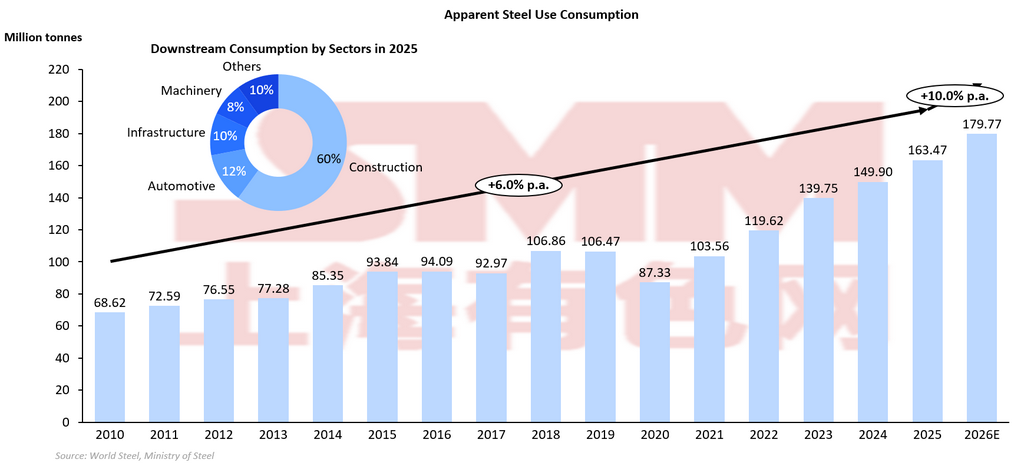

Demand side: Structural Expansion with Temporary Cyclical Interruptions

India’s apparent steel consumption demonstrates a clear long-term structural growth trend rather than a contraction. Demand increased steadily from approximately 68.6 Mt in 2010 to around 163.5 Mt in 2025, implying roughly +6.2% YoY growth, and is projected to reach about 179.8 Mt in 2026E. This expansion reflects a sustained demand-driven cycle supported by infrastructure investment, construction activity, and manufacturing growth. Importantly, the growth trajectory is not linear; short-term dips, such as the decline observed in 2017 and the sharp drop in 2020, are cyclical interruptions rather than structural downturns, with demand quickly rebounding afterward. The most notable feature of the demand trend is the acceleration after 2020, where consumption rose from 87.3 Mt in 2020 to nearly 180 Mt in 2026E, effectively doubling within six years. This rapid expansion indicates that India’s steel demand is entering a high-growth phase driven by urbanization and infrastructure expansion. Construction remains the dominant consumption sector, accounting for roughly 60% of downstream demand, meaning that infrastructure and real estate activity directly shape overall steel consumption trends. As government-led capital expenditure continues, baseline demand remains resilient even during short-term market adjustments.

From a market balance perspective, the projected +10% demand growth in 2026E slightly outpaces supply growth, suggesting that incremental production will be largely absorbed domestically. This reinforces the view that India’s steel market is structurally demand-led rather than export-driven. Instead of signaling a slowdown, the 2026 outlook points to continued expansion with moderated volatility, where demand growth stabilizes after a rapid post-pandemic acceleration. Consequently, the demand side is expected to provide underlying support to domestic prices while maintaining high capacity utilization across steel producers.

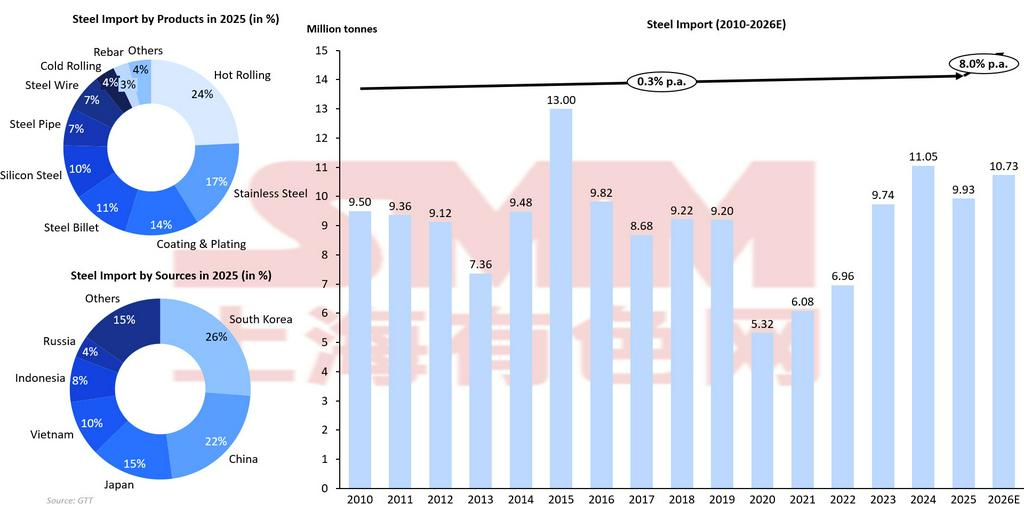

Imports: Overall Decline Continues, but Niche Finished Steel Imports Show Resilience

India’s steel import trend reflects a gradual structural decline in import dependence, but with continued selective reliance on finished steel products. As illustrated in the chart, imports fluctuated around 9-10 Mt during 2010-2019, peaked at 13.0 Mt in 2015, and then declined sharply to 5.3 Mt in 2020 amid pandemic-related disruptions. Imports subsequently rebounded, reaching around 11.0 Mt in 2024, before stabilizing at approximately 10.7 Mt in 2026E, implying a moderating but slightly downward long-term trend. This pattern suggests that while India is reducing reliance on imports, it is not eliminating them, reflecting structural gaps in product mix rather than overall supply shortages.

From a policy perspective, safeguard duties, anti-dumping measures, and domestic capacity expansion are key drivers of the declining trend. These measures discourage low-priced imports and support domestic producers, particularly in commodity-grade steel. However, the import composition reveals that finished steel products continue to dominate import demand, indicating that imports are increasingly concentrated in specialized segments. In 2025, hot-rolled products accounted for 24% of imports, followed by stainless steel (17%), coated and plated steel (14%), and steel billets (11%). This distribution suggests that imports are less about volume substitution and more about quality differentiation and product-specific demand. Source diversification further reinforces this interpretation. South Korea (26%) and China (22%) remain the largest suppliers, followed by Japan (15%) and Vietnam (10%). These countries typically export higher-grade flat steel, specialty steel, or technologically advanced products. Their continued presence in India’s import structure implies that domestic producers have yet to fully close the gap in certain high-end segments. As a result, even when total import volumes decline, finished steel imports in specific categories may remain stable or even increase.

This selective import resilience is consistent with India’s demand-driven growth model. Rising domestic demand for infrastructure, automotive, and manufacturing requires diverse steel grades, some of which are not yet fully produced domestically. Therefore, imports serve as a supplementary mechanism to fill product-specific gaps, rather than a sign of oversupply or weak domestic production. Overall, India’s import dynamics indicate a structural shift from volume-driven imports to niche, quality-driven imports. While total import dependence is gradually declining due to policy protection and capacity expansion, finished steel imports remain necessary in selected segments. This suggests that India is moving toward greater self-sufficiency, but the transition will be gradual, with imports continuing to play a targeted and complementary role in balancing product availability.

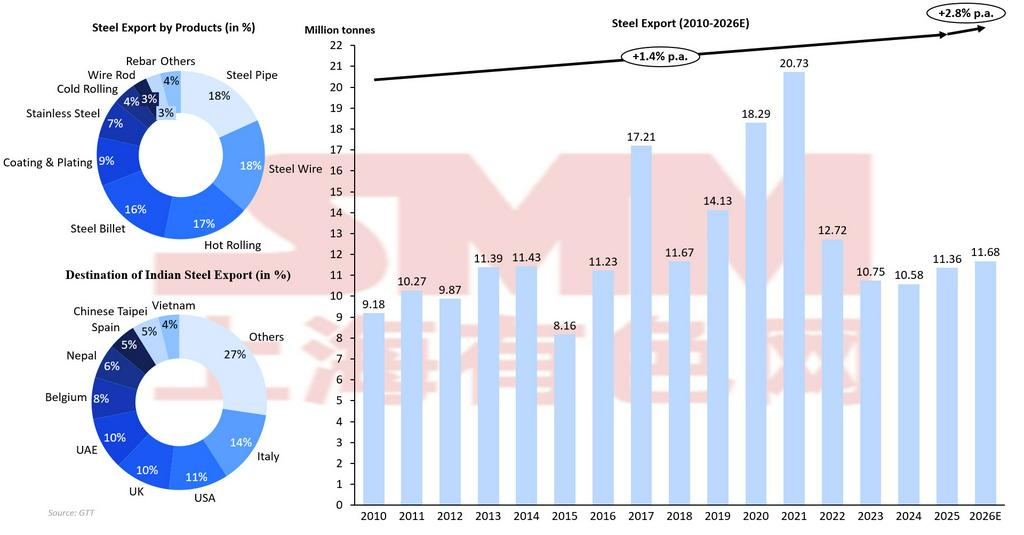

Exports: A Balancing Mechanism in 2026

India’s steel export trend reflects a transition from opportunistic export surges to a more domestically absorbed production structure. As shown in the chart, exports increased from approximately 9.2 Mt in 2010 to a peak of 20.7 Mt in 2021, before declining sharply to around 10.6-11.7 Mt during 2023-2026E, implying only +2.8% YoY growth in the near-term outlook. This pattern suggests that exports are no longer the primary outlet for incremental supply, but rather a balancing mechanism responding to domestic demand conditions and global price competitiveness. The surge during 2017-2021 coincided with favorable global steel prices and temporary domestic supply expansions. During that period, exports functioned as a pressure valve, allowing Indian mills to clear excess production into international markets. However, the subsequent decline after 2021 indicates a structural reorientation toward domestic demand absorption, rather than a loss of competitiveness. As India’s internal consumption expanded rapidly, the need to export surplus volumes diminished, resulting in lower export volumes despite rising production.

Product composition also highlights India’s export positioning. A significant share of exports consists of semi-finished and intermediate products such as billets (16%), hot rolling (17%), and steel wire (18%), alongside pipes and coated products. This mix suggests India often exports flexible, price-sensitive products that can be redirected depending on domestic demand conditions. Even as domestic consumption remains strong, these products still allow mills to increase exports in 2026E, as producers balance incremental supply between local absorption and opportunistic overseas sales. This flexibility supports a modest rise in export volumes rather than a sharp decline. Destination distribution reinforces the diversification strategy. With no single dominant export market, shipments are spread across Europe, the Middle East, Southeast Asia, and neighboring Asian markets. This diversification reduces geopolitical risk but also implies that exports are highly price-sensitive, flowing to whichever region offers arbitrage opportunities. Consequently, India’s export volumes fluctuate with global pricing cycles rather than being anchored to long-term supply commitments.

The modest export growth projected for 2026E despite rising output is a critical signal. If supply growth significantly exceeded domestic demand, exports would typically expand aggressively. Instead, limited export growth indicates that domestic demand is expected to absorb most incremental production. This confirms that India is transitioning into a demand-led steel economy, where exports play a secondary stabilizing role. In practical terms, exports are likely to remain opportunistic rather than structural. Mills may increase shipments temporarily when global prices strengthen or domestic demand softens, but sustained export-led growth is unlikely. This implies that export markets will provide downside protection, but not the primary driver of industry expansion. Overall, India’s export dynamics suggest a structurally stronger domestic market, with exports functioning mainly as a balancing mechanism within a demand-driven growth cycle.

CBAM and Carbon Cost: Emerging Structural Constraint on India’s Steel Exports

Beyond traditional trade remedies such as safeguard and anti-dumping duties, India’s steel exports are increasingly exposed to carbon-related trade measures, particularly the Carbon Border Adjustment Mechanism. As the European Union gradually implements CBAM, importers of steel will be required to pay a carbon cost based on the embedded emissions of exported products. This creates a structural competitiveness challenge for Indian steel, which is still largely produced through the blast furnace–basic oxygen furnace (BF-BOF) route, a more carbon-intensive production method compared to electric arc furnace (EAF)-based production in some other regions.

In the short term, the impact may remain limited because India’s steel exports are diversified across regions such as Southeast Asia, the Middle East, and Africa. However, in the medium to long term, CBAM could increase export costs to the EU market, reducing India’s price competitiveness. This is particularly relevant as India’s export prices typically sit between low-cost producers and premium markets. Additional carbon costs could push Indian offers closer to higher-priced suppliers, potentially weakening export volumes to carbon-regulated destinations.

From a strategic perspective, CBAM also reinforces the importance of India’s domestic demand-driven growth model. As exports face rising carbon-related barriers, domestic consumption becomes even more critical in absorbing capacity expansion. At the same time, Indian steelmakers are expected to accelerate investments in green steel technologies, including scrap-based EAF production, renewable energy integration, and hydrogen-based ironmaking, to maintain long-term export competitiveness.

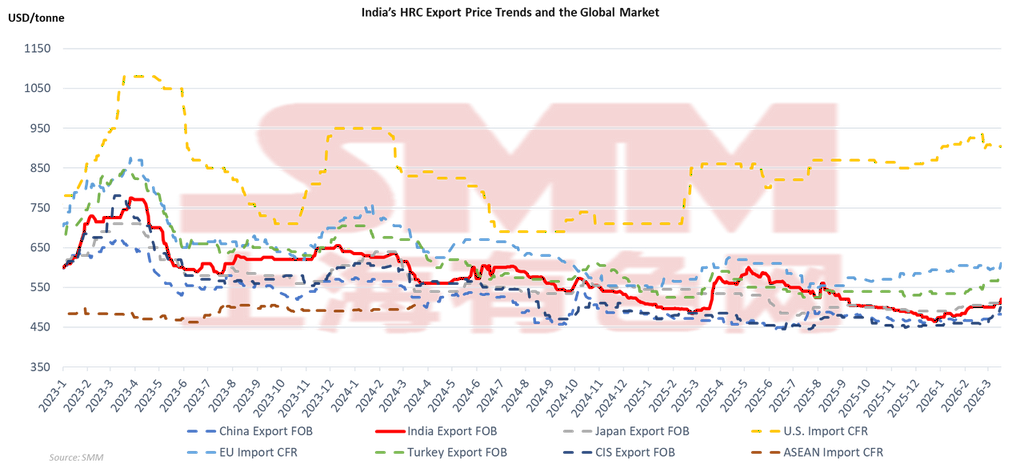

Prices: India Positioned as a Mid-Tier Price Setter Within a Globally Linked Steel Market

India’s HRC export pricing demonstrates strong integration with global steel markets, with price movements closely tracking other major exporters such as China, Japan, CIS, and Turkey. As shown in the chart, India’s export FOB prices moved in a similar pattern to global benchmarks from 2023 to early 2026, declining from the post-tight supply peak in early 2023, stabilizing through 2024, and showing mild recovery into 2026. This co-movement confirms that India is not an isolated price setter; instead, its pricing is influenced by global supply-demand dynamics and trade arbitrage opportunities. A key observation is India’s consistent positioning within the mid-tier pricing band. Throughout the period, India’s export prices generally remained above China and CIS, which represent lower-cost exporters, while staying below premium markets such as the EU and U.S. This indicates that India competes on a balance between cost efficiency and quality, allowing mills to maintain export competitiveness without fully engaging in aggressive price discounting. This mid-range positioning also gives Indian exporters flexibility to redirect shipments depending on regional demand shifts.

The synchronized movements across regions highlight the strong transmission of global market signals. When Chinese export prices declined during periods of weaker demand, India’s prices followed, reflecting competitive pressure in shared export destinations such as Southeast Asia and the Middle East. Conversely, when import prices in the EU and U.S. strengthened, India’s export prices also improved, benefiting from widened arbitrage windows. This suggests that global pricing cycles, particularly those driven by China, remain the dominant influence on Indian export prices. From a market outlook perspective, this high degree of global linkage implies that India’s steel prices in 2026 will be shaped by both domestic demand strength and international market conditions. While strong domestic consumption may provide a pricing floor, India’s export competitiveness will still depend on global price trends. As a result, price volatility is likely to remain moderate, with Indian steel prices moving in line with global benchmarks rather than diverging significantly.

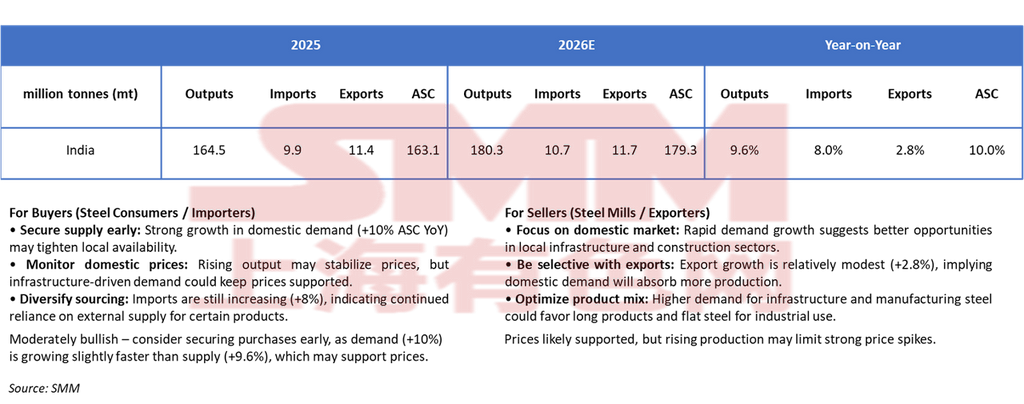

Conclusion: Short-Term Tightness, Long-Term Structural Expansion

In the short term, India’s steel market in 2026 is expected to remain relatively balanced but slightly demand-driven. Steel output is projected to rise from 164.5 Mt in 2025 to 180.3 Mt in 2026, representing a 9.6% increase, while apparent steel consumption (ASC) is forecast to grow slightly faster, from 163.1 Mt to 179.3 Mt, or +10.0% year-on-year. This marginally stronger demand growth suggests that domestic consumption will absorb most of the incremental supply, limiting the need for aggressive export expansion. Imports are expected to increase moderately from 9.9 Mt to 10.7 Mt (+8.0%), reflecting continued reliance on specific product categories where domestic capacity remains limited. Meanwhile, exports are projected to grow only slightly from 11.4 Mt to 11.7 Mt (+2.8%), indicating that India is unlikely to rely heavily on external markets to balance supply. Instead, the domestic market will remain the primary outlet for production growth. This configuration supports a moderately firm pricing environment in the short term. Demand growth slightly outpacing supply expansion suggests that local availability could tighten periodically, particularly in infrastructure-related segments. However, rising domestic production and the modest increase in imports may limit excessive price spikes. As a result, prices are likely to remain supported but not surge sharply, reflecting a broadly balanced supply-demand structure with mild upward bias.

Over the longer term, India’s steel market continues to exhibit strong structural growth potential. With per capita steel consumption still significantly below developed economies and ongoing government-led infrastructure development, domestic demand is expected to expand steadily. Capacity additions will continue to increase supply, but structural demand drivers, urbanization, manufacturing expansion, and infrastructure investment, are likely to absorb additional output. Trade flows will remain flexible, with imports covering specialized grades and exports acting as a secondary balancing mechanism rather than a primary growth driver. At the same time, emerging factors such as decarbonization requirements and carbon-related trade measures may influence export competitiveness. This further reinforces the importance of domestic demand as the core driver of industry growth.

Overall, India’s steel industry is transitioning toward a mature, demand-driven expansion phase, where domestic consumption plays the central role in sustaining growth, reducing reliance on exports, and maintaining relatively stable market conditions over the long term.

![[SMM Daily Hot-Rolled Coil Trading] Spot Trading Volume Increased](https://imgqn.smm.cn/usercenter/EXHJE20251217171720.jpg)

![[SMM Steel] EU initiates GOES and transformer steel safeguarding investigation](https://imgqn.smm.cn/usercenter/aPBtI20251217171717.jpg)