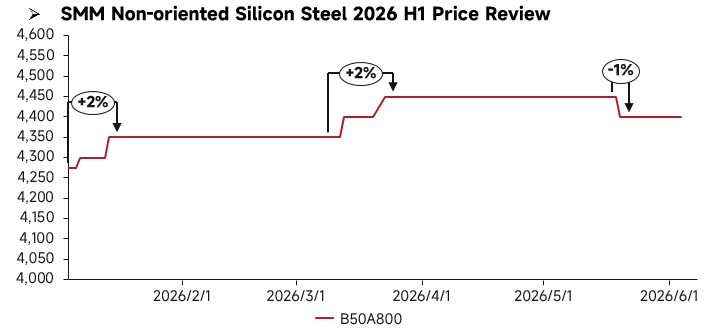

H1 Price Review:

In H1 2026, China's non-oriented silicon steel prices generally fluctuated upward before pulling back, with notable structural divergence in the market. Supply side, the overcapacity in the low and mid-end segment persisted, and supply pressure for standard-grade products remained high; meanwhile, the commissioning pace of high-end production lines aligned with the new energy sector was slow, keeping supply of high-end grades tight. Demand side showed a clear divergence: demand from the traditional home appliance and industrial motor industries was moderate in Q1 before entering the off-season in Q2, with downstream procurement volumes gradually declining; demand in the NEV and high-end motor sectors remained stable, continuously supporting the price trend of high-end grade products.

H1 Fundamentals Review:

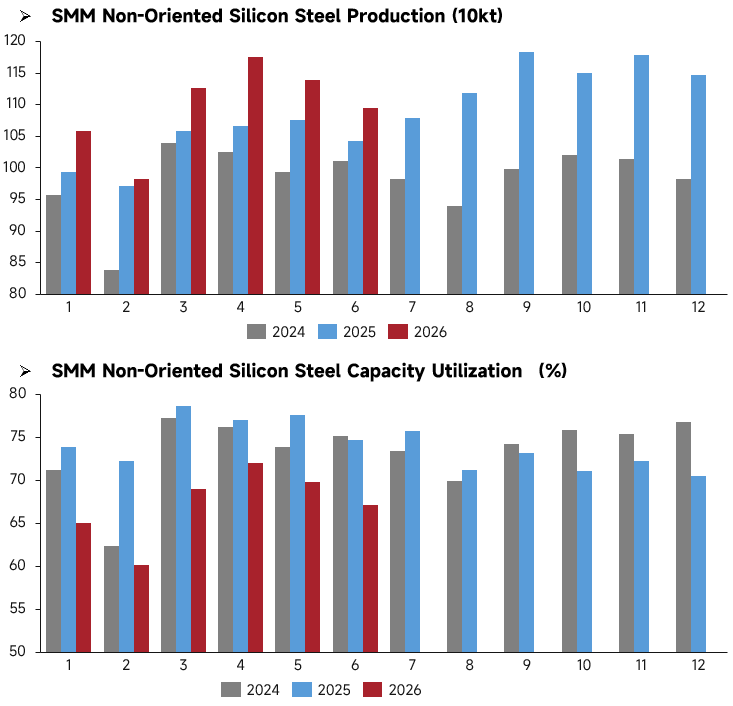

Production side, China's non-oriented silicon steel production schedule showed an overall high-growth trend in H1 2026. The January-June schedule scale was significantly higher than the same periods in 2024 and 2025. April’s schedule hit the H1 peak of about 1.175 million mt, and although it pulled back slightly in May-June, the overall remained in the high range of 1.09-1.14 million mt, reflecting the industry's optimistic expectations for market demand. However, the capacity utilization rate over the same period retreated after a rapid rise. It dipped briefly in January-February due to the Chinese New Year holiday, then rebounded to 69%-72% in March-April, but overall was still significantly lower than the same periods in 2024 and 2025, staying in the 60%-72% range. This divergence of "high production schedule growth but weak utilization rate" reflects that the industry's capacity expansion has outpaced the increase in actual production load, and the pace of new capacity release has been faster than the recovery on the demand side. Although enterprises maintained relatively high production plans, actual operating intensity still fell short of the same period in previous years.

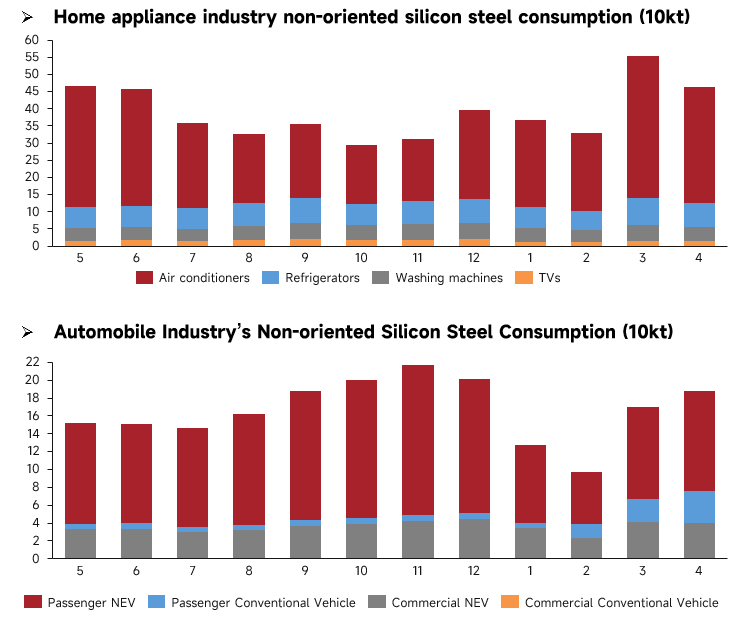

Demand side, in H1 2026 non-oriented silicon steel demand exhibited a pattern of seasonal rebound in home appliances and structural divergence in automobiles. In the home appliance sector, air conditioners served as the core demand support, with the traditional peak-season stockpiling peak in March-April driving industry demand above 550,000 mt. Although demand pulled back due to the off-season in January-February, the overall volume remained higher than the same period last year, while refrigerator and washing machine demand remained stable. In the automobile sector, NEVs remained the main demand driver, with steel consumption by passenger NEVs rebounding rapidly in March-April, while demand for traditional internal combustion engine vehicles stayed sluggish. Overall industry demand recovered from low levels at the beginning of the year, but the growth pace fell short of expectations. Overall, in H1 non-oriented silicon steel demand showed a pattern of “home appliances provided a floor, automobiles recovered.” The peak-season effect in home appliances supported short-term demand, but the recovery pace in the automobile sector was moderate, and the overall demand recovery momentum was weaker than the production schedule expansion, leaving the supply-demand pattern still under certain pressure.

H2 Outlook:

In H1 2026, there were few new capacity additions for non-oriented silicon steel in China, with stable production mainly from existing lines and no new capacity coming on stream. H2 will see concentrated capacity commissioning: Tianjin Shenghui Technology Co., Ltd. in north China plans to commission 160,000 mt of high-grade capacity in Q3; Baowu Baoshan Base in east China will commission 160,000 mt of high-grade ultra-thin gauge capacity and Jiangsu Zhongsheng will commission 280,000 mt of high-grade capacity in Q4. In addition, 250,000 mt of high-grade capacity from Jiangxi Chongxin New Material Co., Ltd., 250,000 mt of high-grade capacity from Fujian Jingu New Material Co., Ltd., and 450,000 mt of NEV-grade capacity from Guangxi Liusteel Electrical New Material Co., Ltd. will also be released intensively in Q4. High-grade and NEV-grade products will become the mainstream of new supply.

Entering H2, new capacity will consist mainly of high-end production lines, while inefficient low and mid-end capacity will gradually exit the market. Traditional downstream demand is expected to see a seasonal recovery, but the boost will be limited. In the new energy sector, rigid demand will remain stable. Overall, the non-oriented silicon steel market is expected to be in the doldrums in H2. Continued capacity expansion will suppress prices; low and mid-grade product prices will continue to trend in the doldrums, while high-end grade product prices will fluctuate.

![[SMM Iron & Steel] South Korea Urges EU to Maintain Fair TRQ Allocations for Korean Steelmakers](https://imgqn.smm.cn/usercenter/UrrTG20251217171717.jpg)

![[SMM Iron & Steel] Turkey’s Q1 2026 Iron Ore Imports Explode 33.9% as Norway and Russia Aggressively Gain Ground](https://imgqn.smm.cn/usercenter/GGaSo20251217171716.jpg)

![[SMM Iron & Steel] US Continues AD and CVD Orders on Prestressed Concrete Steel Wire Strand from Six Countries](https://imgqn.smm.cn/usercenter/SduBz20251217171716.jpg)