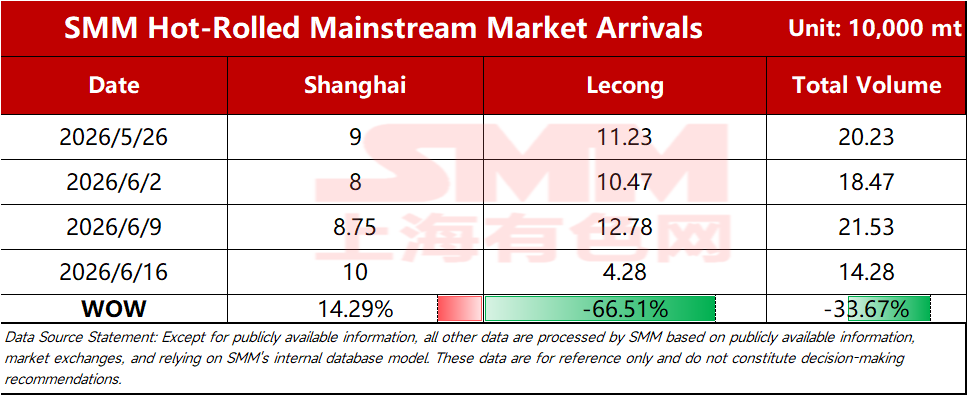

SMM Steel, June 15 – According to SMM statistics, estimated total shipments of mainstream resources this week were 142,800 mt, down 33.67% WoW. By market:

Table 1: Comparison of Arrivals in Mainstream Markets

Source: SMM Steel

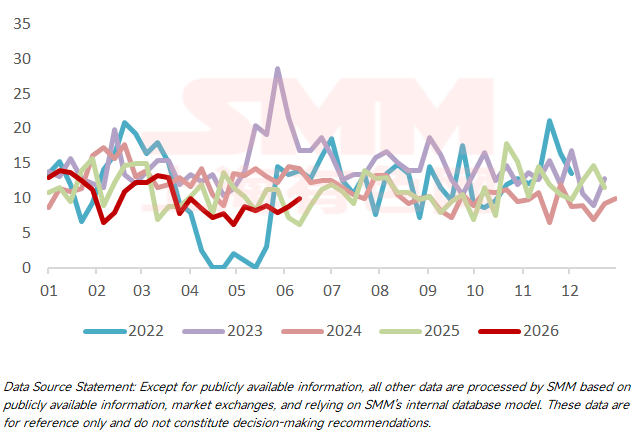

Shanghai Market: HRC shipments in the Shanghai market edged up WoW this week. Specifically, resources from North China and South China edged up, while shipments from Northeast and East China remained stable. Looking ahead to next week, shipments from the north are expected to remain largely stable in the short term with limited fluctuation; for the South China market, given the slow shipment pace of some steel mills earlier, the shipment pace is expected to pick up starting from mid-to-late month, and short-term arrivals in Shanghai are likely to see a slight increase.

Chart-1: Arrivals in Shanghai Market

Source: SMM Steel

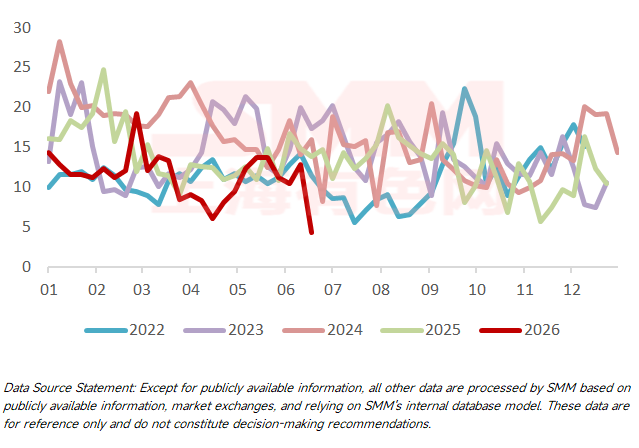

Lecong Market: Shipments to the Lecong direction hit bottom this week. Specifically, resources from North China were mainly stable, while mainstream resources saw significant declines in total shipments, due to both shipment diversion and maintenance impacts. Looking ahead, north-to-south resources are expected to remain low in the short term. As for mainstream resources, WG remains under maintenance in the near term, making it difficult for shipments to increase significantly, but shipments from another resource may rise. Short-term arrivals in Lecong are expected to bottom out and rebound MoM.

Chart-2: Arrivals in Lecong Market

Source: SMM Steel

SMM publishes weekly HRC shipment data for mainstream market routes every Tuesday. To subscribe or access more data, please scan the QR code below.

![[SMM HRC Daily Trading Volume] Spot Trading Volume Retreats from Highs](https://imgqn.smm.cn/usercenter/niwZw20251217171715.jpg)