SMM June 16 News:

Signs of significant improvement in the Middle East conflict have emerged recently. On June 14, the US and Iran finalized the text of a memorandum of understanding; on June 15, Iran confirmed the memorandum, and some terms have already begun to be implemented. Trump stated that the strait is "partially open" and will be fully open on the 19th. The official signing ceremony will be held in Geneva on June 19, with Vance signing on behalf of the US. Core terms include: an immediate and permanent ceasefire on all fronts (including Lebanon); lifting the maritime blockade on Iran; entering final agreement negotiations within 60 days; and Iran taking charge of safe passage management for the strait during a "specified period." The market has already begun to fully price in a US-Iran agreement and the resumption of shipping through the Strait of Hormuz. So, how would this affect the zinc market?

From a transmission logic perspective: in the short term, it affects sentiment → in the medium term, it affects costs → in the long term, it affects supply and demand. Overall, it is biased to the upside but faces an upside ceiling.

I. Easing Inflationary Pressure, Strengthened Liquidity, and Repaired Market Risk Appetite

The geopolitical risk premium in crude oil has been rapidly cleared, inflationary pressure has pulled back, suppressing expectations for US Fed interest rate hikes. The US dollar index has weakened, valuations of dollar-denominated metals have been repaired, market risk appetite has recovered, and funds have flowed out of safe-haven assets (gold, US Treasuries) and into the cyclical nonferrous metals sector.

II. Declining Mining and Shipping Costs, Along with Pullback in Smelting Energy Costs

Oil prices have recently pulled back significantly following the announcement of the agreement. Consequently, in the medium term, as strait shipping returns to normal, shipping congestion and insurance premiums will disappear, ocean freight rates and diesel costs will decline, reducing mining transportation costs. Zinc smelters primarily use electricity, so energy costs will fall, indirectly leading to marginal improvements in electricity costs. The cost support center for smelters will decline, thereby expanding profit margins and boosting smelter production enthusiasm.

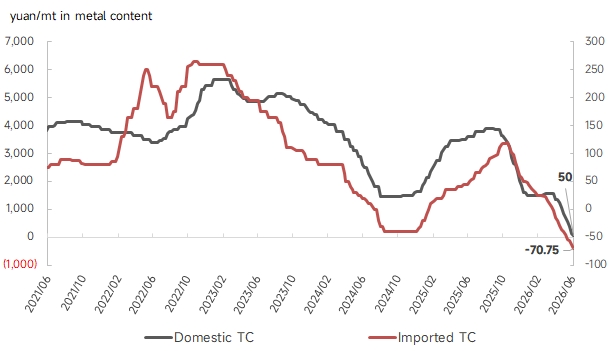

III. Structurally Eased Raw Material Supply Without a Trend of Widespread Ease

In 2025, China imported 5.31 million mt in physical content of zinc concentrates, of which about 325,000 mt in physical content came from the Middle East, accounting for around 6%. After shipping resumes, the return of these supplies will marginally ease the tightness in ore supply. However, imported TCs have already dropped to -$71.2/dmt, and domestic weekly TCs have also fully entered negative territory. Supported by smelter profits, demand for ore remains high, making it impossible to fundamentally reverse the ore shortage. Until large-scale production cuts occur at smelters, TCs are unlikely to rebound quickly.

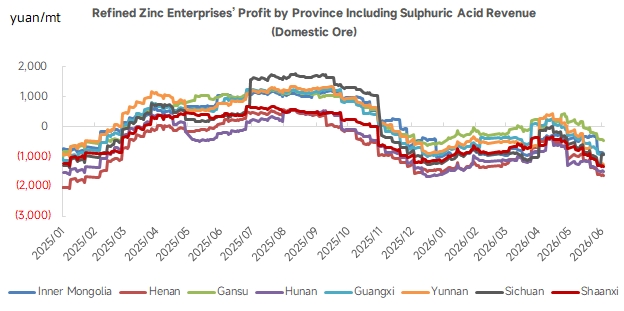

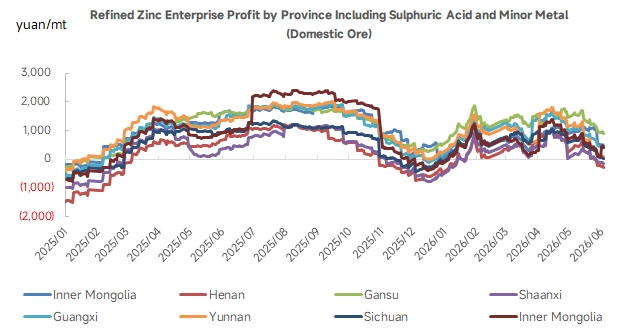

Additionally, against the backdrop of negative TCs, smelters' current profit mainly comes from sulphuric acid and minor metal revenues. The Strait of Hormuz serves as the main shipping route for overseas sulphur. Once shipping resumes, sentiment will cause prices to pull back in the short term, but the high prices of sulphur and sulphuric acid are primarily driven by a fundamentals-side supply-demand mismatch. Medium and long-term price support remains relatively strong. If sulphuric acid prices stay high, smelter profits will still be supported, and production will be difficult to reduce significantly.

Demand-Side Divergence Caps Upside Room

According to customs data calculations, exports of galvanized sheet from China to Middle Eastern countries accounted for 15.3% in 2025. After the agreement is signed, domestic exports will recover, combined with post-conflict infrastructure and housing reconstruction in the Middle East driving incremental galvanizing demand. However, China is in its traditional consumption off-season with no emerging consumption support at present. Domestic social inventory is at a high level for the same period, with spot cargo continuing to sell at a discount, which suppresses the upside room to some extent, making a divergent market of "macro rising, spot weak" likely to emerge.

Overall, the impact of the US-Iran agreement and strait shipping resumption on zinc leans toward "short-term sentiment repair and medium-term marginal cost improvement," but does not alter China's domestic zinc market fundamentals pattern of "mine tightness, high inventory, off-season." The core drivers for zinc prices require attention to the inflection points of domestic mine-side TCs and inventory, as well as the impact of sulphuric acid price trends on smelter production.

Data Source Statement: All data, except for publicly available information, is processed by SMM based on public information, market communication, and SMM’s internal database models. It is for reference only and does not constitute any decision-making advice.