Growth Characteristics and Decadal Evolution of Vietnam's Solar Capacity

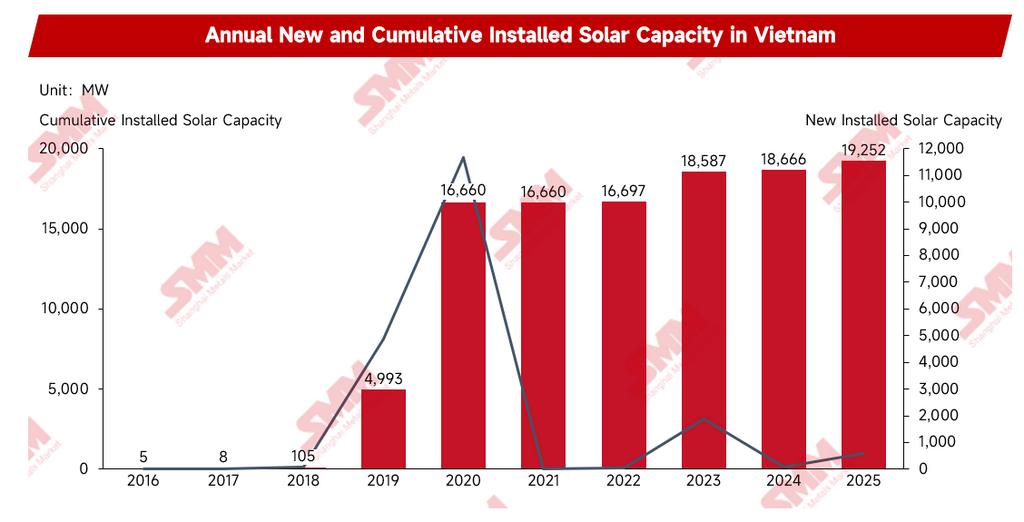

From 2016 to 2025, Vietnam's cumulative solar installed capacity increased from 5 MW to 19,252 MW, growing by more than 3,800 times over the decade. Although the market scale expanded rapidly, its development was primarily driven by policies. During the implementation of the Feed-in Tariff (FiT) subsidy policy, Vietnam experienced two peaks of solar construction; however, after the subsidy policy expired, the market slowed down significantly between 2021 and 2022 due to the failure to promptly transition into a new mechanism. This indicates that the early development of Vietnam's solar market relied heavily on policy support, and its market-driven development mechanism remains in a stage of continuous refinement.

Source: International Energy Agency (IEA) data, processed by SMM models.

Stepping into 2026, with the implementation of the revised Power Development Plan 8 (PDP8), the promotion of the Direct Power Purchase Agreement (DPPA) mechanism, and the issuance of Directive No. 10/CT-TTg, Vietnam's solar policy framework has entered a new phase of adjustment, marking a distinct shift in overall policy logic. The direction of market development has gradually shifted from relying on early fixed feed-in tariff subsidies to a DPPA model centered on market-based pricing mechanisms. The project development structure is also leaning away from centralized large-scale ground-mounted power plants toward the coordinated development of distributed rooftop solar and energy storage systems. Policy targets have shifted from temporarily easing energy supply pressures to a rigid management framework constrained by energy conservation and emission reduction indicators. Meanwhile, the power system is progressively evolving from a unified dispatch model dominated by the state-owned utility into a structure where direct power purchasing and diversified power supplies coexist. Against the backdrop of global supply chain restructuring and the continuous expansion of Vietnam's manufacturing industry, this series of changes is simultaneously reshaping the export structure of Chinese solar modules, as well as the business layout and operational models of enterprises locally in Vietnam.

Policy Evolution and Key Stages of Vietnam's Solar Market

Phase 1: Subsidy-Driven Explosive Growth (2017-2020)

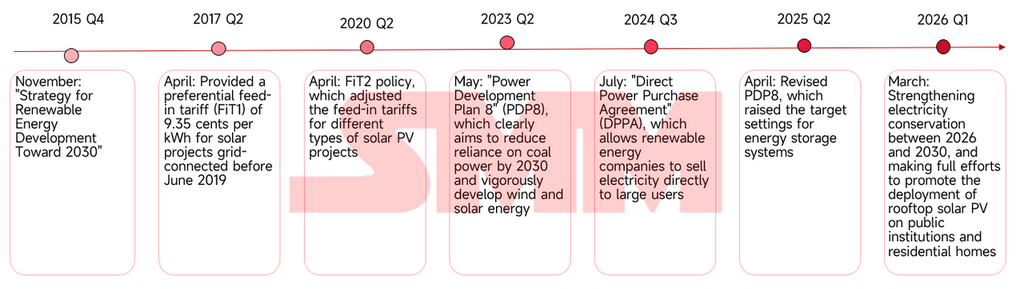

In 2017, Vietnam officially introduced the FiT1 (Feed-In Tariff) policy, which is a fixed feed-in tariff subsidy policy. This is an energy policy tool where the government sets a fixed purchase price higher than the market electricity price to encourage investors to develop renewable energy projects, thereby ensuring project investment returns. At that time, Vietnam's economy was in a period of high-speed growth, with industrial electricity demand growing at an annual rate of over 10%. Under circumstances where traditional coal power expansion was constrained by environmental pressures and hydropower development was approaching saturation, the Vietnamese government urgently needed to fill the power supply gap in a short period. Thus, the high fixed feed-in tariff became an administrative incentive tool to drive energy transition.

The FiT1 policy provided a subsidy of 9.35 US cents per kWh for solar projects grid-connected before June 2019. The FiT1 policy drove Vietnam's cumulative installed capacity to grow from 8 MW in 2017 to 4,993 MW in 2019. Subsequently, when the FiT2 policy was introduced in 2020, another rush-to-build wave occurred in the market, further increasing the cumulative installed capacity scale to 16,660 MW. However, this logic of exchanging high subsidies for installed capacity had severe defects; it only solved the problem of motivation for project construction but neglected the construction demands of the supporting grid network. Because projects were heavily concentrated in the central and southern regions with abundant solar resources, the lag in transmission and substation infrastructure led to solar curtailment becoming a norm, and the grid dispatch system at that time was completely incompatible with the volatile and intermittent characteristics of solar power generation.

Phase 2: Policy Vacuum Triggering Market Stagnation (2021–2022)

As the FiT policies expired, Vietnam fell into a dilemma: continuing fiscal subsidies was financially unsustainable, yet a smooth transition mechanism was lacking after withdrawing the subsidies. This directly resulted in a two-year policy vacuum period. The market had neither a bidding mechanism nor a supporting framework, and the combined new installed capacity over the two years was only 37 MW. This period of stagnation demonstrated in an extreme way that the market at that time remained highly dependent on policy support and clear investment frameworks.

Phase 3: Planning Guidance and Re-activation of Market Mechanisms (2023–2024)

In 2023, the Vietnamese government clarified a new path through the approval of the Eighth Power Development Plan (PDP8), integrating renewable energy into the core of the national energy security strategy. Previously, under the stimulus of the FiT policies, solar projects had experienced explosive growth and became heavily concentrated in the central and southern regions where solar resources are abundant. However, this was severely mismatched geographically with the high-consuming manufacturing centers in the north. Since the local grid could not absorb the power locally, it ultimately triggered large-scale, structural solar curtailment. PDP8 designated grid expansion as one of its key tasks to address the absorption bottleneck exposed in the previous round of centralized solar development.

Data from ASEAN Centre for Energy (ACE) shows that the planned new capacity for 500 kV substations between 2025 and 2030 has reached more than double the existing fleet in 2024. In a power system, substations function fundamentally to raise or lower voltage through transformers and distribute electrical energy, while transmission lines constitute the physical channels for long-distance, cross-regional power transmission. Combined with nearly 13,000 kilometers of new 500 kV transmission lines, the primary intent of this round of grid infrastructure is to widen the ultra-high voltage main grid to break through cross-regional transmission bottlenecks. This will enable the cross-regional transmission of surplus green power accumulated in the central and southern regions to the power load centers in the north, thereby physically relieving the absorption pressure on centralized power stations.

Source: ASEAN Centre for Energy (ACE)

In addition, the Direct Power Purchase Agreement (DPPA) mechanism officially landed in 2024, providing an institutional foundation for generation enterprises to bypass the utility's monopoly dispatch and sell power directly to industrial users. The emergence of this mechanism was fundamentally to fill the commercial logic void left after the exit of FiT. During the implementation of the fixed feed-in tariff policy, developers only needed to complete grid connection to sell power to the state utility at a fixed price, without needing to concern themselves with the actual flow and ultimate consumption of the electricity. However, with the withdrawal of the subsidy mechanism, this revenue path was closed, forcing power generators to confront a question they never had to answer before—once electricity is generated, who exactly is it sold to.

The DPPA mechanism is precisely the institutional response to this question. The DPPA mechanism allows renewable energy generators to sign long-term power purchase agreements with large industrial users, gradually shifting project revenue sources from fixed subsidies toward market-based electricity sales. For power generators, a long-term agreement means stable and predictable cash flows, thereby providing a more solid foundation for project financing. For Vietnam's manufacturing clusters, directly locking in long-term green power prices can effectively hedge against the risks of electricity price volatility, while providing a practical path for enterprises to address increasingly stringent supply chain ESG compliance requirements. However, the DPPA mechanism was only in its initial implementation stage in 2024, with its scope of application mainly concentrated in a few large industrial user pilots, while true large-scale promotion and systems remained incomplete.

Phase 4: From Subsidy-Driven Toward Rigid Institutional Restructuring (2025-Present)

After 2025, Vietnam's solar industry entered a new phase of transitioning from policy incentives to institutional constraints. Different from the past when investments were stimulated by fixed feed-in tariff subsidies, current policy priorities have shifted toward energy security assurance, stable operation of the power system, and the realization of energy conservation and emission reduction targets.

This shift is first reflected in the implementation of the revised PDP8. The revised version further raised the target proportion of renewable energy in the power mix and for the first time incorporated Battery Energy Storage System (BESS) construction as an important component of power system development. As solar and wind installed capacities continue to rise, energy storage facilities are beginning to take on functions such as peak shaving, smoothing fluctuations, and enhancing grid absorption capabilities. Although the policy level has not introduced a one-size-fits-all mandatory storage mandate, the development model for renewable energy is gradually shifting from standalone generation project construction toward the coordinated development of "renewable energy + storage" under market-driven pressures in the face of main grid absorption constraints.

At the same time, the DPPA mechanism has transitioned from pilot implementation into a large-scale promotion phase, providing the institutional foundation for establishing long-term power trading relationships between renewable energy enterprises and large industrial users. The power sales model has begun to progressively transition from the traditional EVN single-buyer model to a market-based trading model, and the revenue sources of solar projects have also shifted from relying on subsidies toward being supported by market-based power demand.

Directive No. 10 issued in 2026 further reflects the shift in policy direction. The directive proposes to raise the solar coverage rate on public buildings and residential rooftops, and integrates energy conservation and consumption reduction requirements into the management objectives across government departments, enterprises, and society. Unlike the past practice of attracting project construction through subsidies, the policy in this new phase places more emphasis on promoting the popularization of solar applications through institutional constraints and energy‑saving targets, allowing the solar industry to gradually become an essential component of energy system construction rather than an emerging sector relying solely on subsidies.

Comprehensive Impact of Vietnam's Solar Policy

Market Growth Model Undergoing Transformation

With the end of the feed-in tariff era, Vietnam’s incremental solar PV demand structure is shifting toward a parallel development of distributed solar PV and commercial and industrial solar-plus-storage projects. In the past, market growth relied primarily on subsidy policies to stimulate development, and project developers focused more on locking in grid-connection windows to secure fixed returns. Currently, driven by the DPPA mechanism, energy storage matching requirements, and energy security demands, market growth is progressively shifting toward being grounded on genuine power demand. Commercial and industrial users, industrial parks, and export manufacturing enterprises are becoming vital sources of new demand, and the economics of solar projects are beginning to depend more on long-term power sales capabilities rather than policy subsidy levels.

Power Marketization Reform Reshaping the Supply Chain Competitive Landscape

The implementation of the DPPA mechanism not only alters power trading methods but is also reshaping the competitive logic of the supply chain. In the past, the core competitiveness of solar enterprises was mainly reflected in module prices and delivery capabilities; however, the future market will pay closer attention to system efficiency, project development capabilities, storage integration capabilities, and long-term operations and maintenance (O&M) service capabilities. As end-users' participation continuously deepens, project investment decisions will become more market-driven, forcing enterprises to progressively transform from equipment suppliers into comprehensive energy solution providers.

Policy Execution Effectiveness Will Continue to Dictate the Pace of Market Development

Although Vietnam has established a relatively complete development framework for renewable energy, the progress of policy implementation remains a key variable affecting market prosperity. In the past, the market experienced distinct stagnation due to insufficient policy alignment; therefore, the implementation of revised PDP8 contents, the rollout of detailed energy storage matching policy rules, and the advancement speed of power marketization reforms will all directly influence new installed capacity scales and investor confidence. In the long term, the direction of Vietnam's renewable energy development is fundamentally clear, but the pace of market growth will still be influenced to a large extent by policy execution efficiency.

Summary

The development history of Vietnam's solar market over the past decade reflects that its energy transition path is undergoing a fundamental transformation. The early market relied heavily on fixed feed-in tariff subsidies to rapidly expand its installed scale, but the resulting rush-to-build waves, grid congestion, and policy disruptions also exposed the limitations of driving renewable energy development solely through fiscal incentives. The market stagnation between 2021 and 2022 further demonstrated that installed capacity growth does not equate to market maturity, and that a stable institutional framework and power market mechanisms are the critical foundations for supporting the industry's long-term development.

Entering 2025 and moving forward, as the revised PDP8, the DPPA mechanism, and Directive No. 10 land successively, Vietnam's renewable energy policy has begun to pivot from encouraging investment toward optimizing power system operations, and from pursuing installed capacity scale toward enhancing energy security and power assurance capabilities. The development logic of the solar industry is also progressively shifting from being subsidy-driven to demand-driven, with the importance of C&I power demand, grid absorption capabilities, and energy storage system construction continuing to rise.

For Chinese solar enterprises, opportunities in the Vietnamese market are extending from pure module exports toward higher value-added areas such as energy storage systems, C&I distributed project development, energy management services, and localized operations. With the expansion of Vietnam's manufacturing industry and the continuous advancement of power marketization reforms, Vietnam is still one of the solar markets with the greatest growth potential in Southeast Asia. However, at the same time, policy execution efficiency, grid construction progress, and the rhythm of marketization reforms will continue to dictate the actual speed and growth quality of the industry's development over the coming years.

![[SMM Photovoltaic] Sun Village Unveils ‘Road to 2030’ Strategy: Targeting 2GW Solar and ¥100 Billion Sales](https://imgqn.smm.cn/usercenter/GHTIQ20251217171741.jpg)

![[SMM PV] AIKO Wins Wood Mackenzie 2026 Module Manufacturer Grade A Rating](https://imgqn.smm.cn/usercenter/CpbPE20251217171736.jpg)

![[SMM PV] National Energy Administration's June Dispatch Meeting: Cumulative Grid-Connected Wind and Solar Capacity Hits 1.911 Billion kW, Seven Key Tasks Deployed](https://imgqn.smm.cn/usercenter/TygQH20251217171742.jpg)