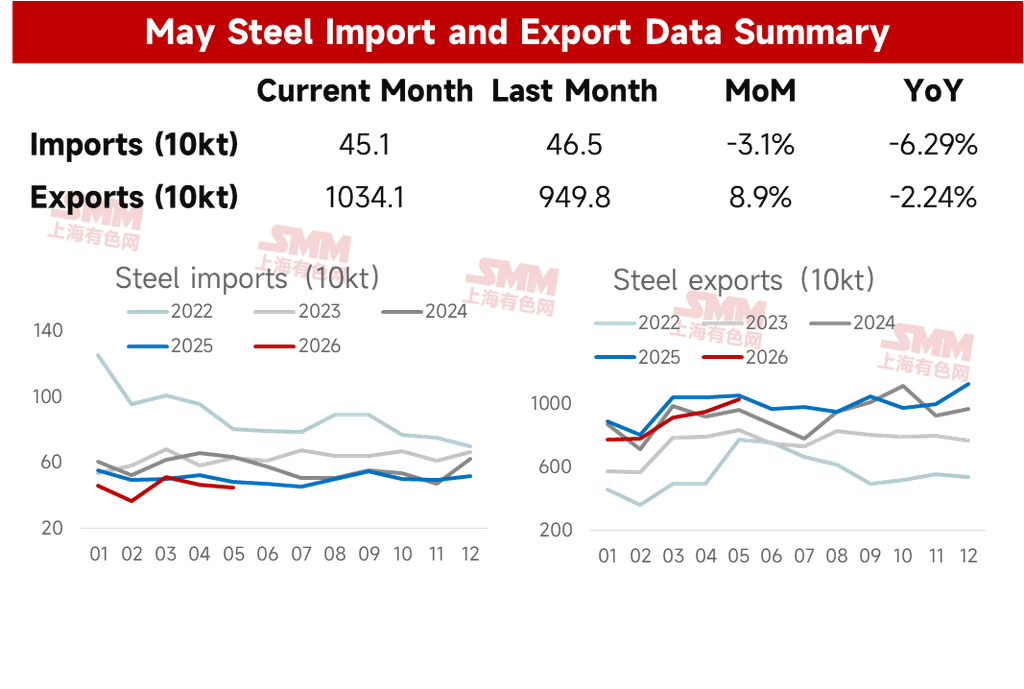

On June 9, customs data showed that China exported 10.341 million mt of steel in May 2026, an increase of 844,000 mt MoM, up 8.9% MoM. Cumulative exports from January to May reached 44.554 million mt, down 8.1% YoY.

China imported 451,000 mt of steel in May 2026, a decrease of 14,000 mt MoM, down 3.1% MoM. Cumulative imports from January to May totaled 2.255 million mt, declining 12.2% YoY.

Table1 – Steel Import and Export Data Overview, January-May

Source: SMM

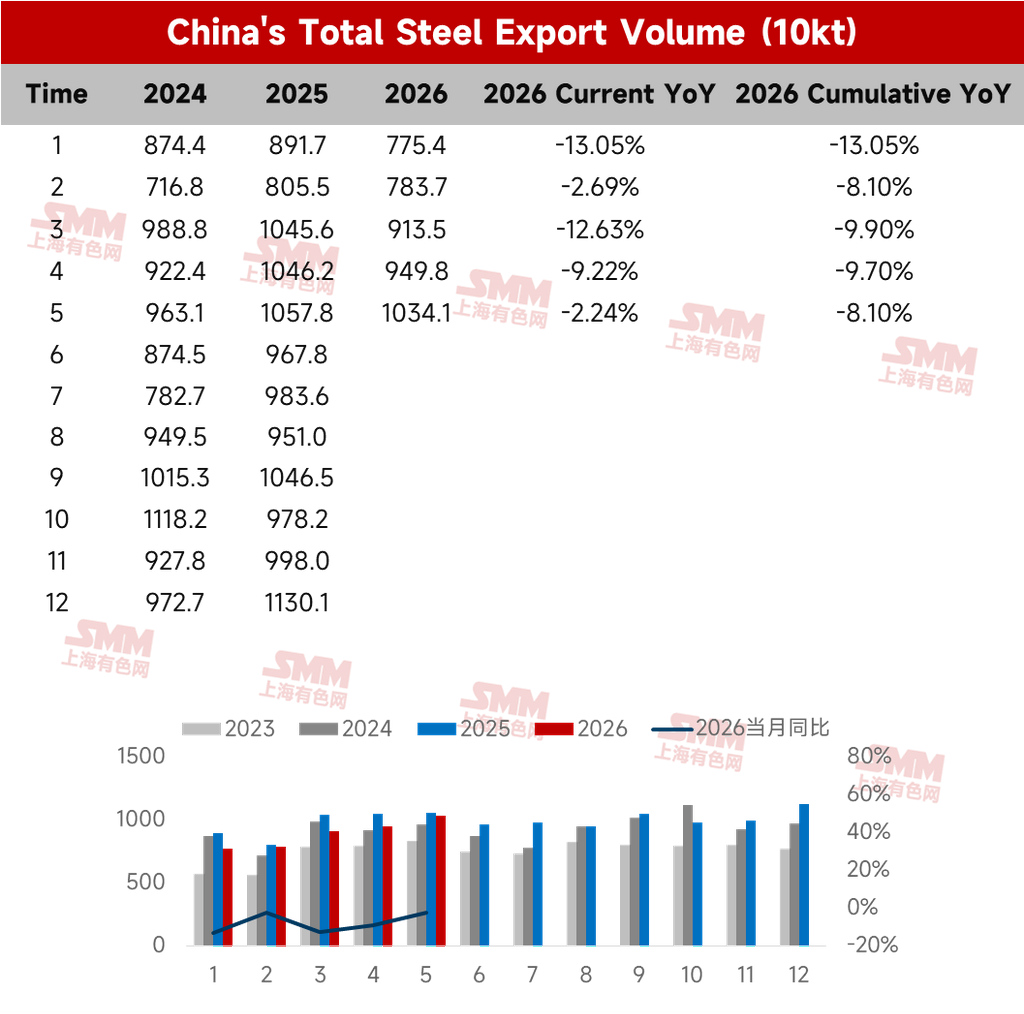

- Steel Exports in May Crossed 10 Million mt MoM

According to SMM's export schedule survey for May, planned HRC exports that month stood at 1.1435 million mt, up 213,500 mt from actual April exports, a 23% MoM increase. Meanwhile, SMM export order data showed that from March to April, domestic export prices held a strong advantage in international markets, and overseas demand for semi-finished products remained present. Export orders reached a periodical high in mid-April, providing some support for May exports exceeding 10 million mt.

Table 2– China Total Steel Exports

Source: SMM

- Steel Imports in May Declined MoM

On the import side, steel imports stood at 451,000 mt in May, edging down MoM. From January to May, China imported a total of 2.255 million mt of steel, down 12.2% YoY; net steel exports reached 42.299 million mt.

- Short-Term Steel Export Outlook

1. Global manufacturing diverges notably; US accelerates sharply while domestic new export orders slide from highs

Global manufacturing activity showed marked divergence in May 2026. The latest PMI data indicates the US accelerated strongly, rising to 54% from 52.7% in April, though cost surges driven by inflation posed significant headwinds. The Eurozone PMI dropped to 47.5% from 48.8%. India continued to demonstrate resilience: its May manufacturing PMI reached 55%, a three-month high, fueled by robust domestic demand, infrastructure spending, and new business growth. China's new export orders index came in at 48.6% in May, down 1.7 percentage points MoM, reflecting some weakening in export demand.

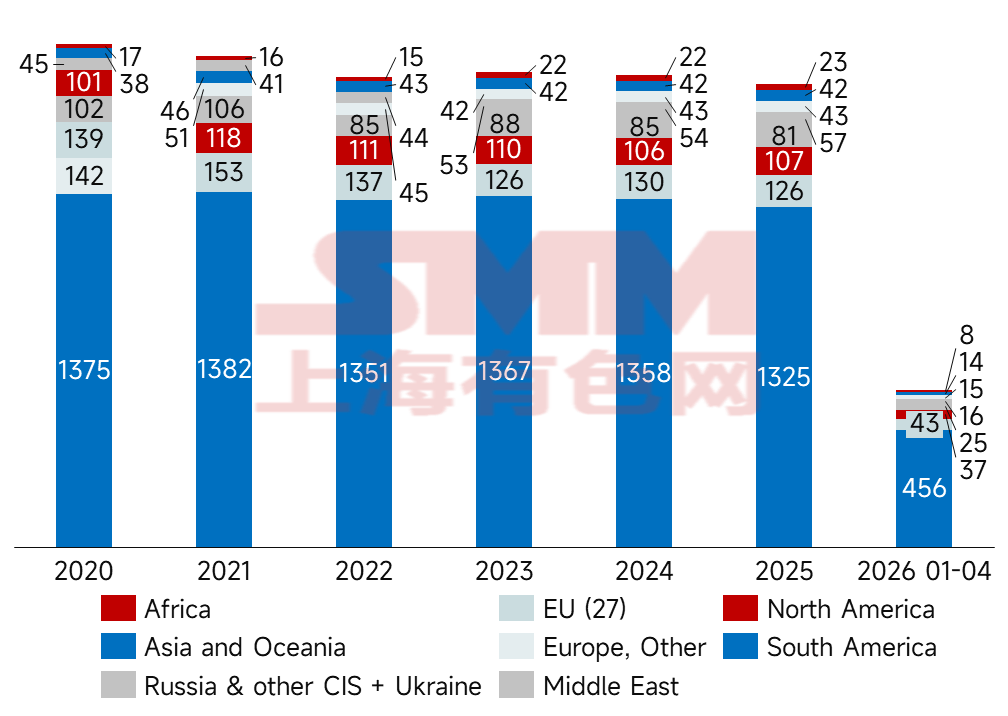

2. Overseas supply continues to decline, particularly evident in the Middle East

World Steel Association data shows global crude steel production fell 1.9% YoY to 153.4 million mt in April 2026. Excluding China, output in the rest of the world slid 4.25% MoM, with production schedule paces diverging significantly across regions. Among markets outside China, India and Vietnam maintained high production levels, mainly benefiting from the structural ramp-up dividends brought by new capacity commissioning. Meanwhile, the US and Germany also stood out in April: the US was directly boosted by seasonal Q2 production schedule expansions in high-end manufacturing sectors such as automobiles, while Germany's four consecutive months of production rebound essentially reflected a strategic inventory build by steel mills in response to raw material price fluctuations. In contrast, Middle East production continued its steep YoY plunge during the month, mainly attributable to wartime energy controls and systemic logistical paralysis triggered by the US-Iran conflict and the full closure of the Strait of Hormuz. Overall, Middle East output remains in contraction. As original recipient countries face a lack of stable supply sources, coupled with the digestion of previous low-priced resources, China's steel export orders may encounter structural opportunities.

Figure 1 – Global Crude Steel Production by Region

Source: SMM

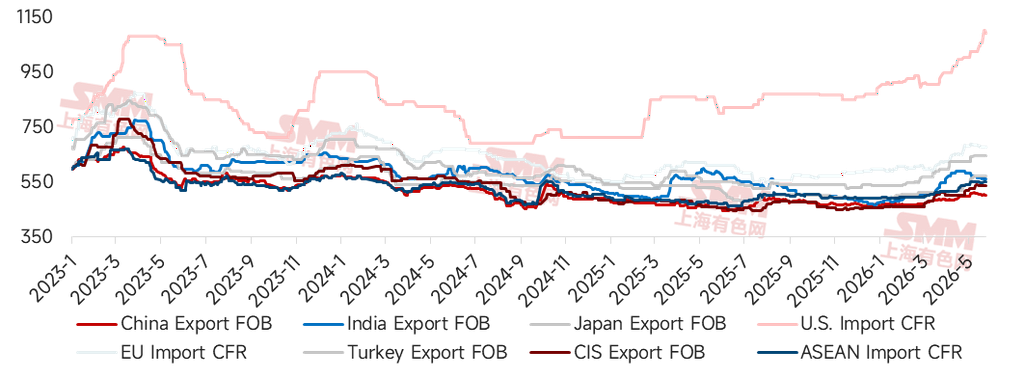

3. Price advantage remains notable, but Southeast Asian markets show price-cutting behavior to seize market share

As of June 5, 2026, HRC export quotations (FOB) from India, Turkey, and the CIS stood at $550/mt, $645/mt, and $535/mt, respectively, while China's HRC export quotation (FOB) was $501/mt. China's HRC export quotations currently stand at discounts of -$49/mt, -$144/mt, and -$34/mt against these countries, keeping its steel export price advantage distinct. Recently, however, Southeast Asia entered its off-season; with domestic demand unable to support elevated prices, there are signs of price reductions to capture orders from the international market and disperse domestic pressures. The price spread between China and Southeast Asia has narrowed somewhat.

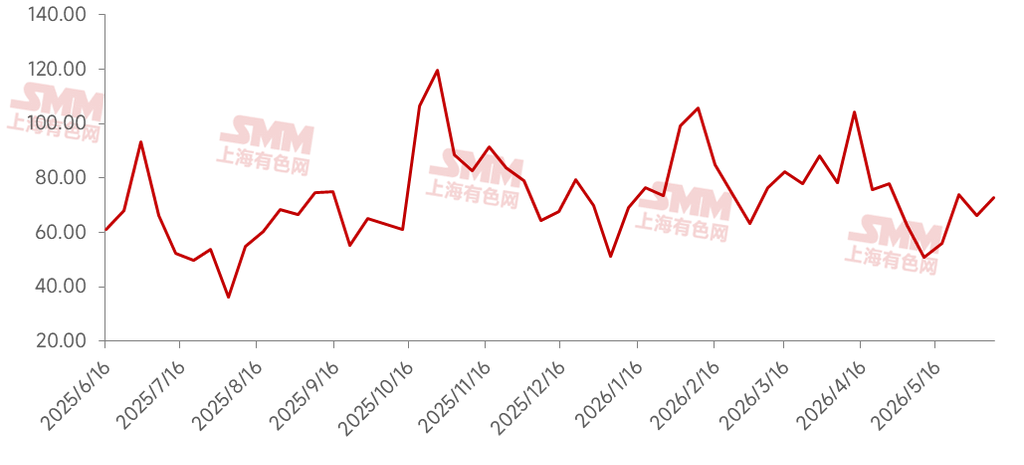

Figure 2 – HRC Quotations in Key Global Markets

Source: SMM

4. Export orders dropped notably in May, with a related slowdown after concentrated procurement

According to SMM's latest survey of steel mill export schedules, planned HRC exports this month stand at 1.03 million mt, roughly steady compared with actual exports last month. SMM steel export order data indicates that, affected by holidays, export orders in May declined noticeably from April on a MoM basis. Orders for both flat products and long products slipped, signaling that overseas buyers have slowed their procurement pace after the earlier round of concentrated procurement.

Figure 3 – SMM Steel Export Order Volumes

Source: SMM

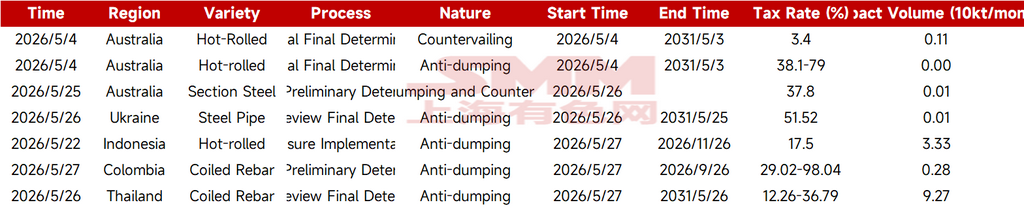

5. HRC faced the most cases entering the enforcement stage in May

After the concentrated final rulings of anti-dumping cases in April, anti-dumping cases decreased somewhat in May, involving products including HRC, coiled rebar, section steel, and steel pipes. Specific cases and their affected volumes are shown in the table below:

Table – New Anti-Dumping Cases in May

Source: SMM

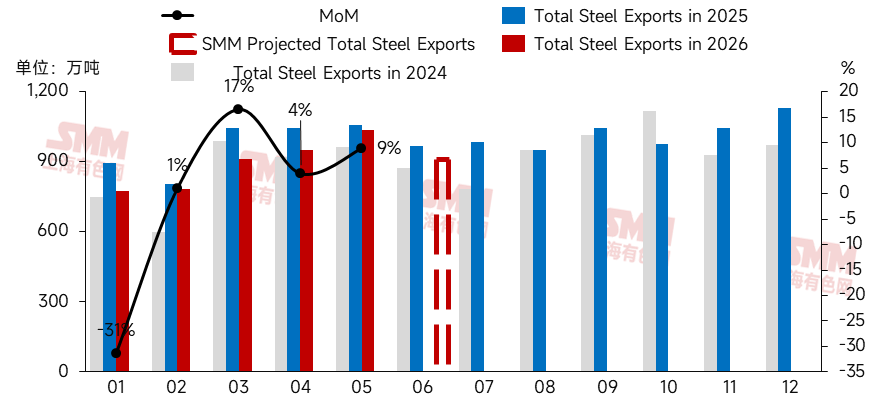

Taking all factors into consideration, as the new export orders index narrows somewhat, Southeast Asian markets cut prices to compete for orders, and the significant contraction in export order volumes over the previous two months gradually feeds through to the shipment stage, the cushioning effect from earlier orders will weaken considerably. SMM expects that actual total steel exports in June will face some downward pressure. At the same time, as overseas supply of previously low-priced materials is absorbed and Chinese prices remain competitive, domestic export orders may show a bottoming-out recovery trend. Recent feedback from the Southeast Asian market also indicates new procurement demand for semi-finished products.

Figure 4 – Steel Exports and Forecast, 2024-2026

Source: SMM

Disclaimer on Data Sources: Except for publicly available information, all other data herein are processed and derived by SMM based on publicly available information, market communication, and SMM's internal database models. The content is for reference only and does not constitute decision-making advice.

Note: This article is an original work published on this official account. For requests regarding reproduction, whitelist access, cooperation, or other matters, please contact us. Without permission, the content shall not be reproduced, modified, used, sold, transferred, displayed, translated, compiled, disseminated, or otherwise disclosed to third parties or licensed for third-party use. Upon discovery of any violation, Shanghai Metals Market will pursue infringement liability through legal means, including but not limited to demanding contractual breach of contract liability, return of unjust enrichment, and compensation for direct and indirect economic losses. Scan to Get Free Information

![[SMM Hot-Rolled Coil Daily Trading Volume] Spot trading volume releases somewhat.](https://imgqn.smm.cn/usercenter/hyiDc20251217171715.jpg)