Entering June, while upstream MHP payables stayed high, auxiliary material prices such as sulphur and sulphuric acid continued to climb, and downstream ternary production schedules remained at relatively high levels, the performance of battery-grade nickel sulphate prices was not optimistic. SMM believes this was mainly driven by multiple factors, including weakening cost support, front-loaded downstream stockpiling, increased import supplementation, and higher volumes of nickel sulphate converted from refined nickel.

I. Nickel Sulphate Cost Situation

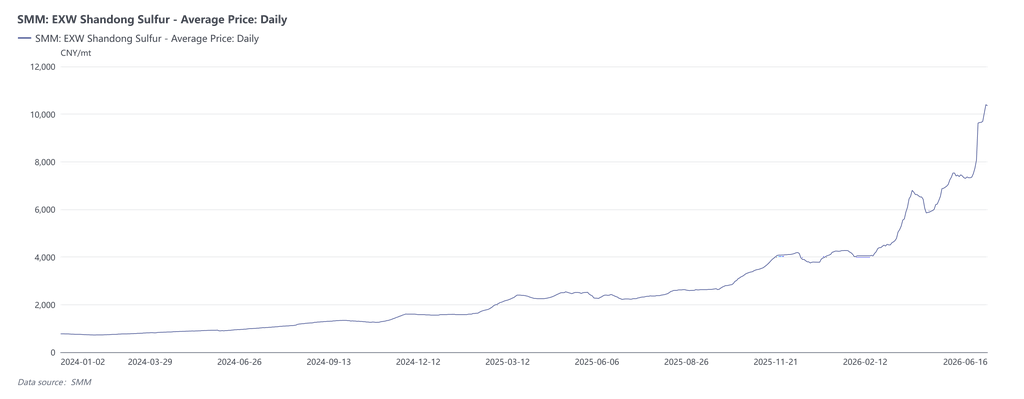

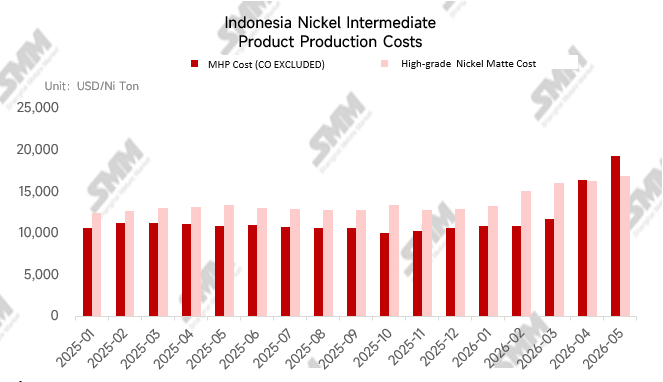

Overall, the sharp rise in sulphur and sulphuric acid prices this year significantly increased the total processing cost of nickel sulphate. As of this week, according to SMM data, spot transaction prices for sulphur in China exceeded 10,000 yuan/mt, while sulphur prices in Indonesia reached $1,250-1,300/mt. Against this backdrop, the per-mt price of sulphuric acid approximately doubled compared to the beginning of this year. Taking MHP-based nickel sulphate processing as an example, the theoretical processing cost per mt in metal content of nickel sulphate rose by over 3,000 yuan from the start of the year, putting pressure on nickel sulphate producers.

By raw material, in May, MHP payables strengthened and high-grade nickel matte payable indicators stayed high. Nickel prices showed an overall fluctuating downward trend but remained at relatively high levels.

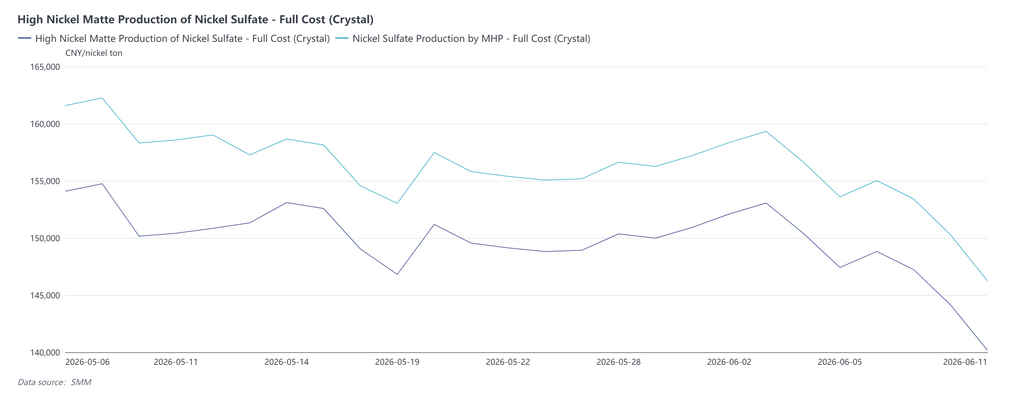

Affected by production cuts, MHP payables rose somewhat. This month, costs for externally purchased MHP-based nickel sulphate production increased, driven by higher payables and rising sulphuric acid costs, leading to losses for enterprises. The theoretical cost of integrated MHP-based nickel sulphate production also surged significantly due to sulphur, likewise falling into a loss-making state.

Available spot cargo volumes of high-grade nickel matte remained low, and its payable indicators stayed high. However, as its processing cost was lower than that of MHP, costs had not yet fallen into losses. The costs of integrated high-grade nickel matte producers were slightly driven up by ore prices and sulphur but still retained a significant advantage compared to other raw materials.

Meanwhile, due to tight supply of crude slag, its payable indicators remained high this month, and the cost of producing nickel sulphate from crude slag also remained loss-making.

Entering June, MHP and high-grade nickel matte payables are expected to stay high. Meanwhile, amid rising expectations of interest rate hikes combined with inventory pressure, nickel prices saw a sharp correction at the beginning of the month.

By raw material, as the impact of the Middle East situation on sulphur supply has not yet been fully resolved, a significant recovery in overall MHP supply was not yet observed, and payables are expected to fluctuate at highs. However, due to the correction in nickel prices, the loss-making pressure on enterprises purchasing MHP externally may ease somewhat, while integrated producers remain loss-making due to high sulphur prices. The market circulation of high-grade nickel matte also remained relatively tight, with the coefficient expected to hold steady. Production costs for external purchases in June may pull back in tandem, while integrated production costs are similarly expected to maintain their advantage.

II. Nickel Sulphate Supply & Demand Analysis for June

Looking at the month's supply and demand, nickel sulphate was relatively tight in June. SMM estimates a supply-demand gap of approximately 3,700 mt in metal content of nickel sulphate, driven mainly by high downstream production schedules.

Demand side, sustained restocking by downstream players in China's ternary battery market combined with strong export orders kept the June production schedule for ternary cathode precursors basically stable compared to May, still at historically high levels. Supply side, as production of hydrometallurgy intermediate products had yet to recover significantly, some producers reduced nickel sulphate output using MHP, while production plans using other raw materials did not show notable supply contractions. Meanwhile, some refined nickel producers also planned to cut refined nickel output in favour of nickel sulphate production. As a result, overall nickel sulphate production edged up roughly 1.5% in June but remained insufficient to meet precursor demand.

Despite the supply-demand gap, the weak performance of nickel sulphate prices was driven, in addition to softening cost support, by the following factors:

1. Pace of downstream stockpiling

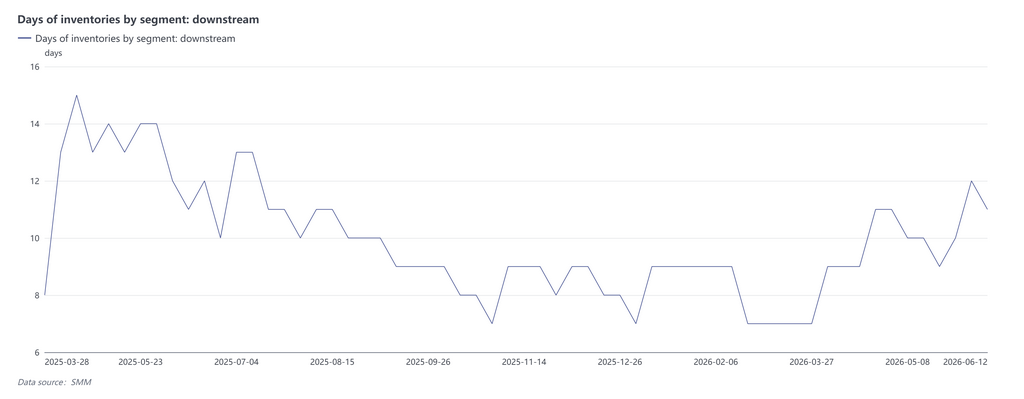

SMM downstream inventory data shows that the downstream inventory index trended upward, April-May, driven by stockpiling for Labour Day holiday as well as by production cuts in intermediate products and a sharp rise in nickel prices. Against this backdrop, nickel prices pulled back sharply this month. "Rush to buy amid continuous price rise and hold back amid price downturn" sentiment, combined with the mid-year period, led to generally weak downstream procurement sentiment for nickel sulphate in the middle of the month. Destocking was expected to dominate this month, thus capping the uptrend in nickel sulphate prices to some extent.

2. Nickel sulphate imports

Since the end of Q4 2025, due to relatively strong nickel sulphate demand and prices in China, nickel sulphate imports from outside China have remained at elevated levels overall. From January to April 2026, China's cumulative nickel sulphate imports rose roughly 43% YoY. In addition to regular imports from Indonesia, some enterprises in South Korea sold sulphate raw materials to China amid relatively weak domestic demand for ternary cathode precursors there, while Finland and other countries also shipped a certain scale of nickel sulphate into China, supplementing the spot nickel sulphate market.

3. Conversion of Refined Nickel to Nickel Sulphate

Since May, the Middle East situation had been releasing expectations of de-escalation, and with no significant reversal in refined nickel inventory pressure, nickel prices pulled back in May. Meanwhile, nickel sulphate prices performed strongly, supported by downstream stocking demand and costs, with battery-grade nickel sulphate maintaining an overall premium over refined nickel. The average premium in May exceeded 10,000 yuan/mt. Entering June, the macro environment for nonferrous metals was weighed down by interest rate hike pressure, and the turning point for refined nickel inventories had yet to emerge, amplifying the correction pressure on nickel prices. However, due to tight supply-demand conditions and being a spot cargo not directly influenced by the futures market, nickel sulphate prices remained relatively strong, with the average premium reaching 13,000 yuan/mt in the first two weeks.

Therefore, for enterprises with refined nickel production capacity, using the same raw materials to produce nickel sulphate was more economical. Although the volume of refined nickel converted to nickel sulphate was currently relatively small, considering cross-product price linkage, raw material shortages, and the cash flow conversion advantages of refined nickel, if the high premium of nickel sulphate continued in the future, some refined nickel enterprises might expand the scale of conversion, thus impacting the nickel sulphate market from the supply side.

4. Raw Material Adjustments in Nickel Sulphate Production

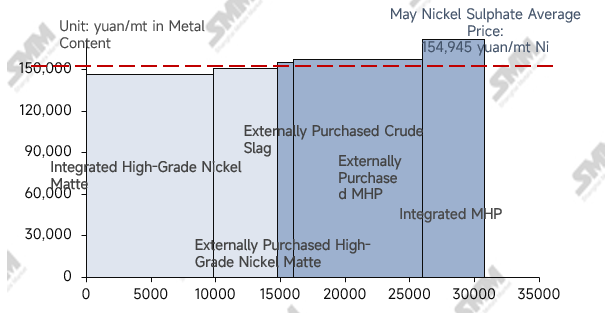

While MHP supply declined significantly due to the impact of sulphur, high-grade nickel matte suffered relatively less impact on production costs and scale. According to SMM data, in May, high-grade nickel matte accounted for 41% of nickel sulphate raw materials, equaling the share of MHP, and was expected to rise further to 42-43% in June.

According to SMM calculations, for integrated enterprises, based on a consumption of 11.8 mt of sulphur per mt Ni from MHP, with other factors unchanged, when the sulphur price was $870/mt, the economic viability of using MHP and high-grade nickel matte to produce nickel sulphate was equivalent. As the current sulphur price was already above $870/mt, integrated nickel sulphate producers found it more economical to use high-grade nickel matte as the raw material.

For enterprises using externally purchased raw materials, the current coefficients of high-grade nickel matte and MHP were similar, while the cost of processing into nickel sulphate was lower than that of MHP. Therefore, it was also theoretically more economical, and some enterprises had already adopted high-grade nickel matte as the main raw material for nickel sulphate production. Therefore, if the sulphur problem in hydrometallurgy intermediate product projects remains difficult to resolve in Q3, while saprolite ore supply is replenished after the rainy season ends and supplementary quotas are implemented, high-grade nickel matte could release supply flexibility on the raw material side for nickel sulphate. Based on the assumption that MHP can resume normal production by end-Q3, SMM estimates that high-grade nickel matte could account for over 45% of nickel sulphate raw materials in Q3. If hydrometallurgy intermediate products subsequently maintain a low operating rate, the share of high-grade nickel matte could rise further.

III. Price Outlook

Looking ahead to Q3, on the raw material side, the impact of high sulphur prices on intermediate product production is expected to be difficult to eliminate in the short term, and the recovery in intermediate product supply is likely to remain limited. Although some new projects may bring incremental MHP, the intermediate product coefficient is expected to fluctuate upward. On the demand side, after heavy stockpiling in H1, downstream procurement demand in Q3 is expected to pull back compared to H1. However, the domestic September-October peak season and export orders from top-tier producers will still support the overall demand level for nickel sulphate. On the supply side, uncertainty in raw materials may continue to disrupt nickel salt production, but external sales from refined nickel producers could provide supply flexibility.

Therefore, nickel sulphate supply is expected to remain tight in Q3, and cost support may weaken slightly. With procurement demand pulling back, nickel salt prices at the beginning of Q3 may decline compared to Q2, but a rebound could occur during the September-October stockpiling period.