February 2026 coincided with the Chinese New Year holiday. Affected by holiday factors, production pace across core segments of China’s sodium-ion battery industry generally slowed, showing an “off-season reset” trend. From cathodes, anodes, and electrolyte to battery cells and end-users, production across all segments declined MoM to varying degrees, while YoY still maintained a certain degree of growth resilience. As the Chinese New Year holiday ended, the industry gradually recovered, and production across all segments in March is expected to see a sharp rebound.

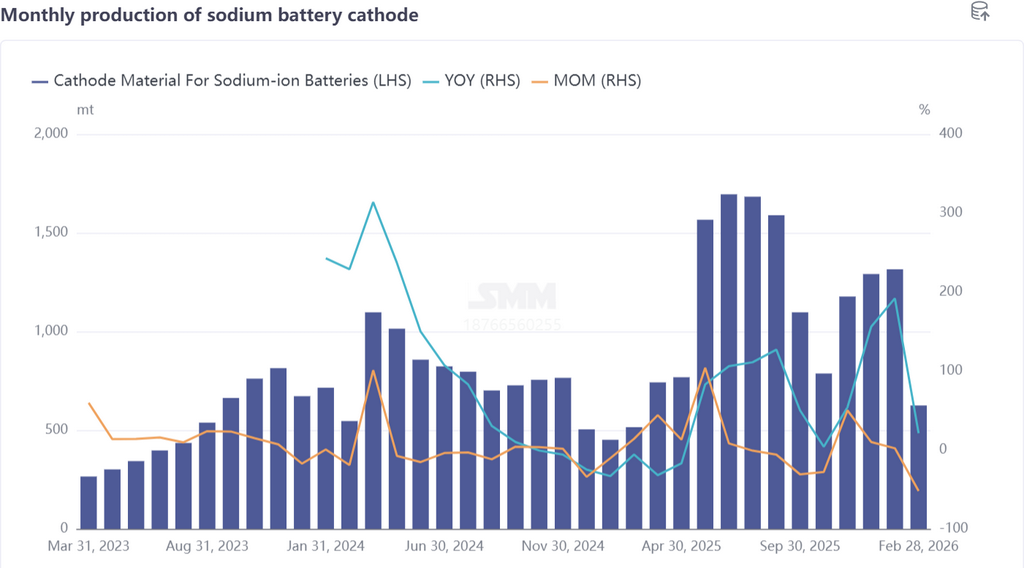

I. Cathode Materials: Chinese New Year Production Stalled, Sharp MoM Decline, Strong Recovery Expected in March

In February, production of sodium-ion battery cathode materials was significantly affected by the Chinese New Year holiday, plunging 52% MoM; however, it still achieved 21% growth YoY, demonstrating a positive long-term industry development trend. From the product mix perspective, polyanion materials continued to hold an absolute dominant position, with a share as high as 83%, while NFPP’s share fell 8 percentage points MoM, indicating a slight adjustment in the product mix.

Production side, sodium-ion battery cathode production in February showed clear divergence: some enterprises maintained production, mostly those also with lithium battery cathode capacity. As the lithium battery segment largely maintained normal production schedules in February, coupled with delivery requirements for sodium-ion battery-related orders, their sodium-ion battery production lines did not shut down during the Chinese New Year period, making full preparations for March order deliveries. Meanwhile, most enterprises in the industry suspended production and took holidays in early to mid-February,

entering the Chinese New Year holiday ahead of schedule. In particular, layered oxide cathode enterprises almost all primarily shut down and took holidays, pushing the overall sodium-ion battery cathode industry into the off-season.

As the Chinese New Year holiday ended, industry production and transportation will gradually return to normal. March sodium-ion battery cathode production is expected to see a strong rebound, surging 107% MoM, with YoY growth also expected to expand to 74%, and the industry is expected to quickly emerge from the off-season.

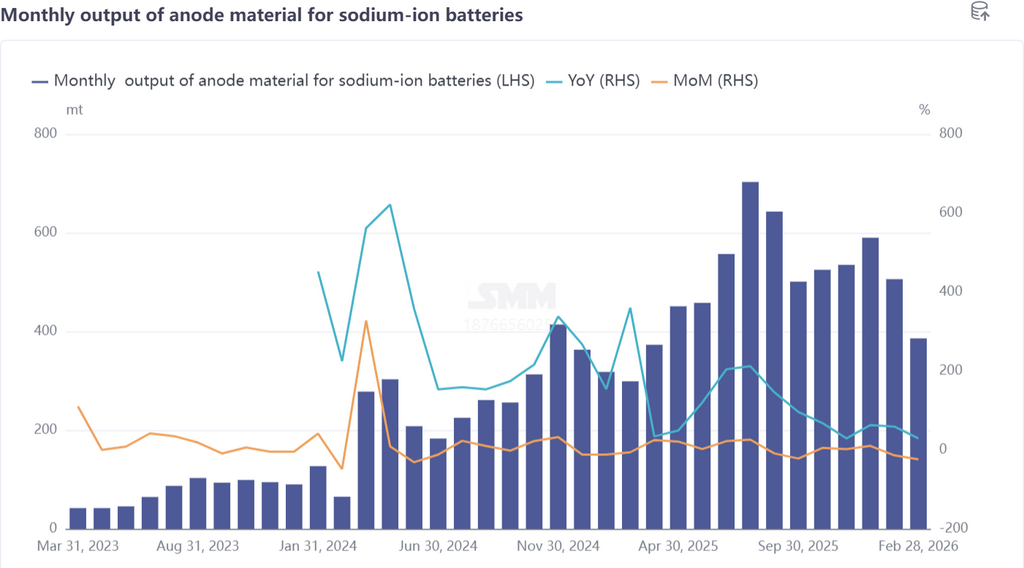

II. Hard Carbon Anode Materials: Production Mostly Halted During Chinese New Year, Order Backlog Supports Subsequent Growth

In February, production of sodium-ion battery hard carbon anode materials fell 24% MoM and rose 29% YoY, showing a trend similar to that of cathode materials overall. From a production scheduling perspective, most hard carbon enterprises mainly halted production and took the holiday. To mitigate the impact of the Chinese New Year holiday, enterprises largely delivered orders ahead of the holiday and reserved necessary inventory to ensure smooth post-holiday deliveries.

Notably, not all enterprises entered a shutdown. Some hard carbon enterprises, based on order demand, reasonably arranged production plans during the Chinese New Year period to keep production lines operating normally. Industry feedback indicated that in the first two months of 2026, battery cell manufacturers had issued relatively clear plans for bulk hard carbon orders, which not only supports the scaled rollout of sodium-ion battery hard carbon but will also drive enterprises to further conduct R&D on new products tailored to the sodium-ion battery market. However, insufficient hard carbon capacity remains the primary challenge facing the industry, constraining the pace of scaled development.

Entering March, hard carbon enterprises will further align with downstream demand and steadily advance post-holiday efforts to resume production. March production is expected to surge 69% MoM and rise 75% YoY, with the capacity utilization rate gradually rebounding.

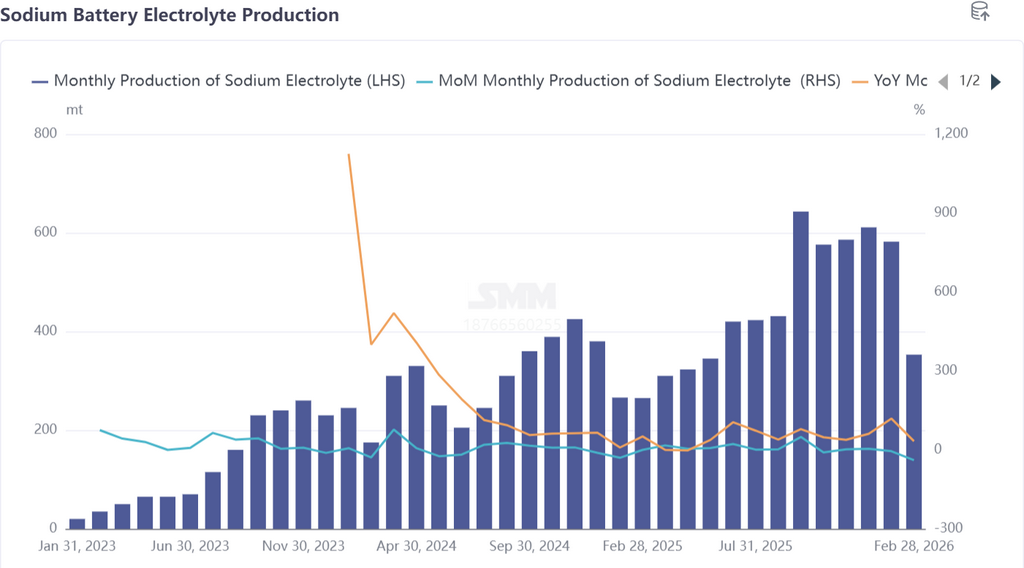

III. Sodium-Ion Battery Electrolyte: Sluggish Market Performance, With Demand Gradually Recovering in March

In February, the sodium-ion battery electrolyte market remained sluggish, with both orders and actual shipments at low levels. Production fell 39% MoM and rose 33% YoY. Raw material side, raw material costs for sodium-ion battery electrolyte fluctuated relatively little during the month and did not have a noticeable impact on industry production.

Affected by insufficient orders and the Chinese New Year holiday, some enterprises adjusted production resources, reallocating production lines originally used for sodium-ion battery electrolyte to the lithium battery segment, further reducing sodium-ion battery electrolyte production. As industry demand recovered in March, market orders were expected to increase gradually.

Sodium-ion battery electrolyte production was projected to rise accordingly, up 51% MoM and up 72% YoY, with the industry gradually shaking off the impact of the off-season.

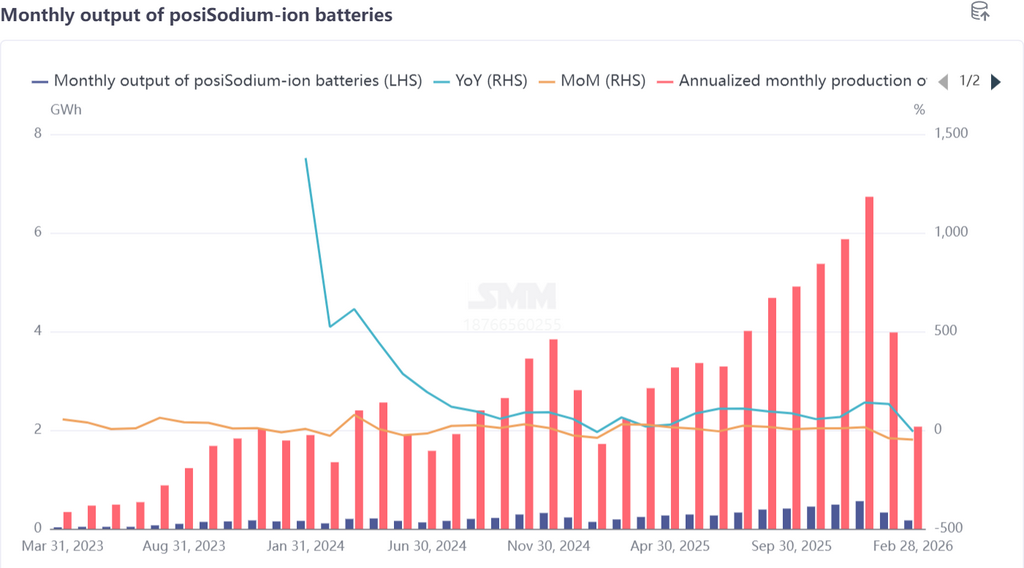

IV. Battery Cells and End-Use Applications: The Production Off-Season Became More Pronounced, and Long-Term Growth Potential Was Released

In February, the sodium-ion battery cell market also entered the off-season, with production down 48% MoM and down 7% YoY. On the production side, most sodium-ion battery cell enterprises took holidays and suspended operations during the Chinese New Year, leading to a marked reduction in output; meanwhile, logistics suspensions slowed delivery progress for orders, further weighing on production for the month.

Long term, the development potential of the sodium-ion battery industry continued to be released: after the holiday, lithium carbonate prices remained at high levels, and the cost advantages of sodium-ion battery cells gradually became a focus of market attention, with inquiries increasing; in addition, leading traditional lithium battery manufacturers rolled out sodium-ion battery-related products, and policies across regions in 2026 were also accelerating the buildout of sodium-ion energy storage, promoting more diversified development of sodium-ion battery end-use application scenarios and further expanding room for market demand.

As the market recovered after the holiday, some sodium-ion battery projects had already begun preparatory work in March. Sodium-ion battery cell production was estimated to recover gradually, up 88% MoM and up 37% YoY, with the industry returning to a growth track.

V. Summary

Overall, in February 2026, key segments of the sodium-ion battery industry were affected by the Chinese New Year holiday, with the production pace slowing down and production across the board declining to varying degrees on a MoM basis. The industry as a whole entered the off-season, a performance consistent with the seasonal pattern. Although production was affected in the short term, the industry’s long-term resilience became evident: except for

battery cells, the cathode, anode, and electrolyte all achieved positive YoY growth, and favorable factors such as downstream order backlogs and policy support laid a solid foundation for the industry’s recovery.

As the Chinese New Year holiday ends in March, production and transportation will fully resume, and each segment of the industry will gradually emerge from the off-season. Production is expected to post a significant MoM increase across the board, and YoY growth is also expected to expand further. Looking ahead, as hard carbon capacity is gradually released, end-use application scenarios continue to expand, and policy support intensifies, the sodium-ion battery industry will continue to maintain a steady development momentum, with the industrial-scale rollout expected to accelerate.