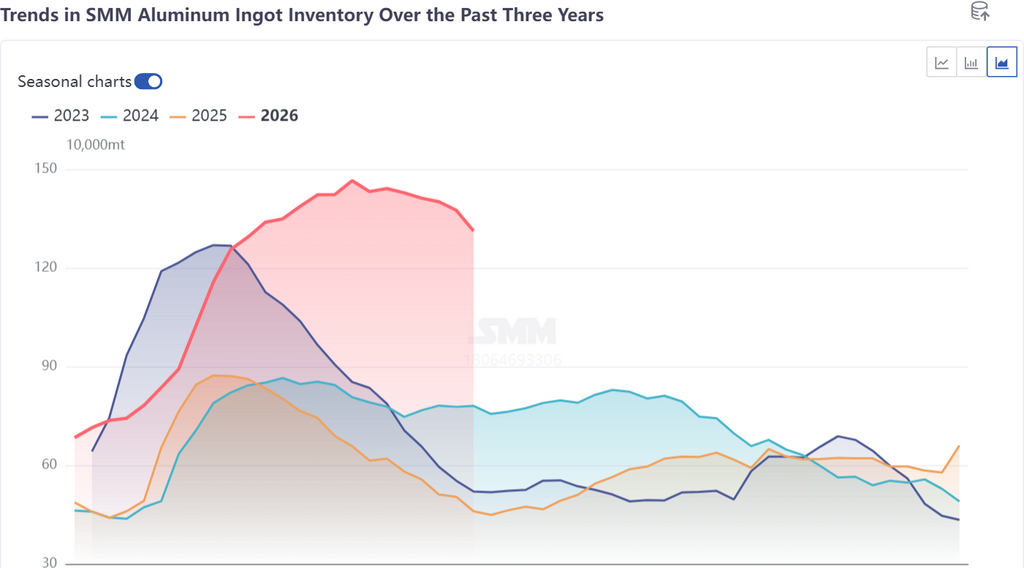

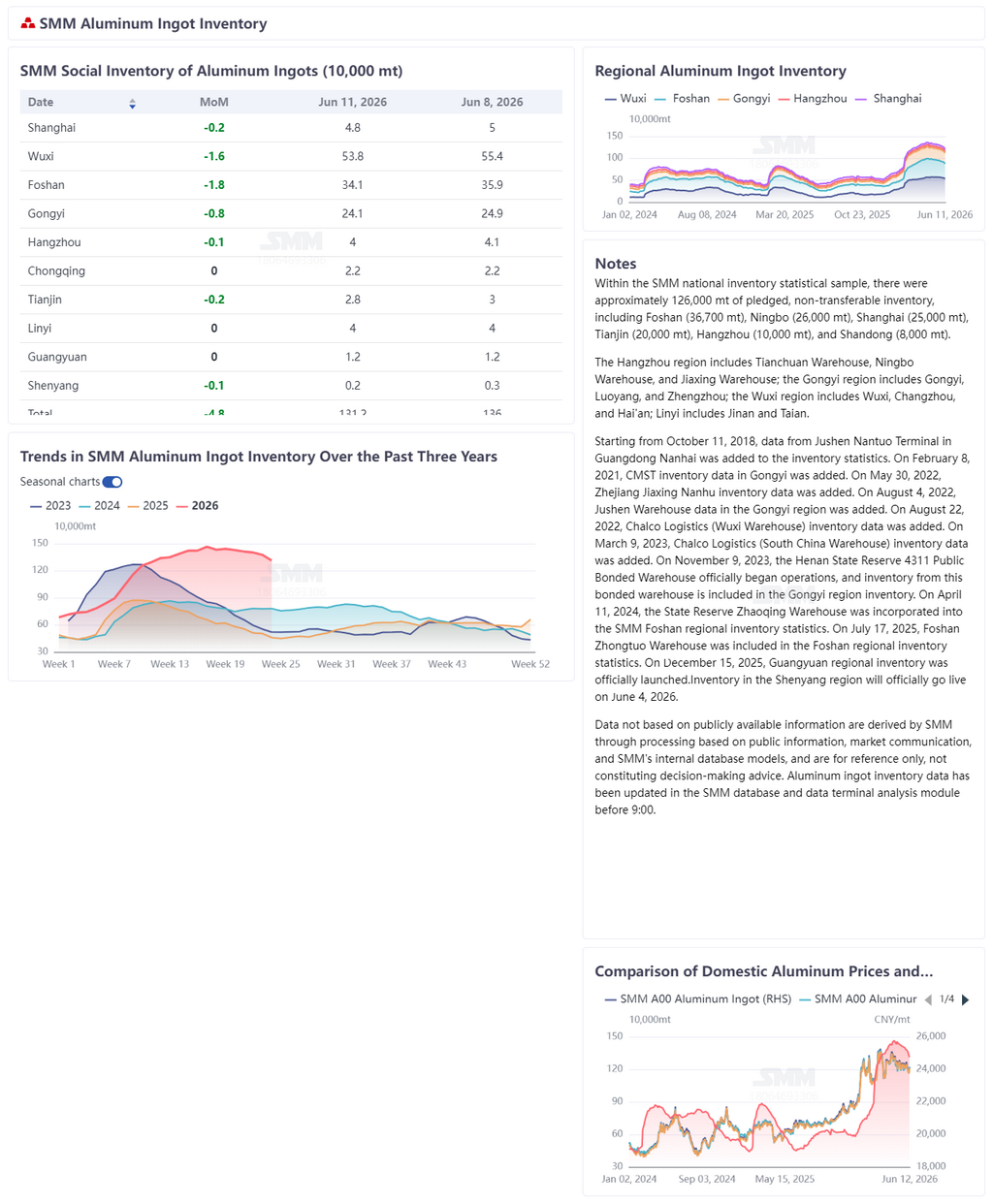

Aluminum Ingot Inventory: Destocking Turning Point Established at High Levels, but Absolute Volume Pressure Persists

China’s aluminum ingot inventory, after hitting a peak not seen in nearly three years in 2026, accelerated its pullback this week. According to SMM statistics, as of June 11, aluminum ingot inventory in major Chinese consumption areas was reported at 1.312 million mt, having cumulatively destocked by nearly 160,000 mt from the early-May high of around 1.47 million mt. The single-week decline this week reached 48,000 mt, clearly steepening the destocking slope.

From a seasonal pattern perspective, over the past three years, aluminum ingot inventory has shown a cyclical pattern of “building up around Chinese New Year, peaking around April-May, and gradually destocking in Q2.” The peak was around 880,000 mt in 2024 and also around 880,000 mt in 2025 (basically flat vs. 2024), while the 2026 peak reached approximately 1.48 million mt, about 600,000 mt higher than the previous two years, placing YoY inventory at a historically high level and indicating that supply accumulation pressure has significantly amplified since the start of this year.

The driving forces behind this destocking round are structurally differentiated and cannot be simply attributed to a recovery in domestic demand following the pullback in aluminum prices. SMM believes there are three reasons:

1. Both actual and expected supply are contracting: The proportion of liquid aluminum has rebounded continuously (reaching 76.5% in May and expected to rise further to 76.6% in June), with casting ingot shifting toward billet and other processed products, reducing the physical circulation of aluminum ingot. Combined with the standardized advancement of China’s aluminum capacity, this has caused actual aluminum ingot supply to edge down in June.

2. Export boost driven by wide price spread between Chinese and overseas markets: The supply gap for aluminum outside China continues to widen, and China’s aluminum semis export orders have improved more than expected, effectively absorbing liquid aluminum capacity and reducing the amount of aluminum ingot formed—a key structural support for this destocking round.

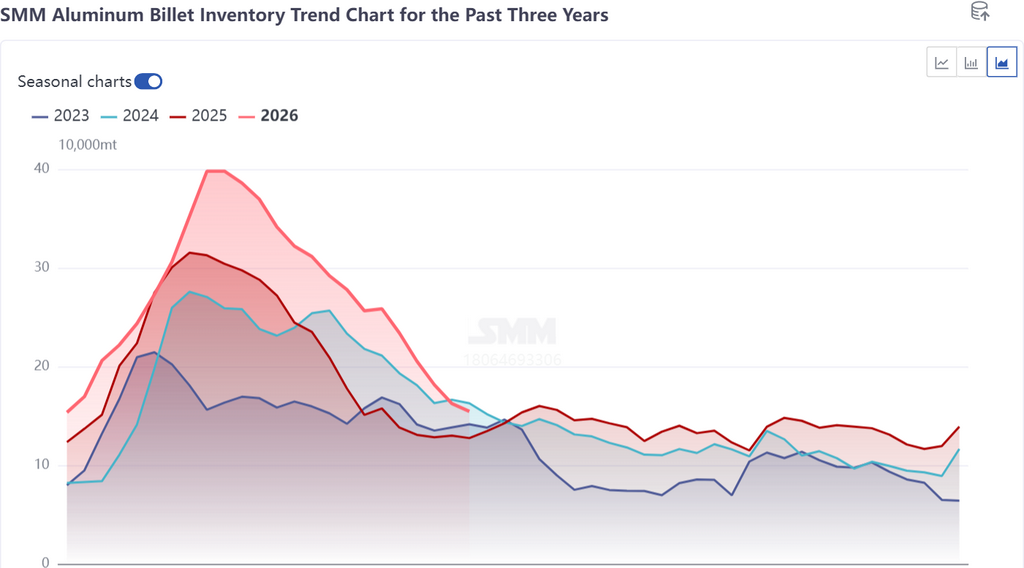

3. The substitutability of demand between aluminum ingots and aluminum billets was the main reason for the accelerated destocking this week: when the outright price is low and the processing fees of aluminum billets are high, downstream users tend to directly purchase aluminum ingots rather than billets. This substitution logic is now taking effect, and the accelerated destocking of aluminum ingots, alongside a slowdown in destocking of aluminum billets, also serves as supporting evidence.

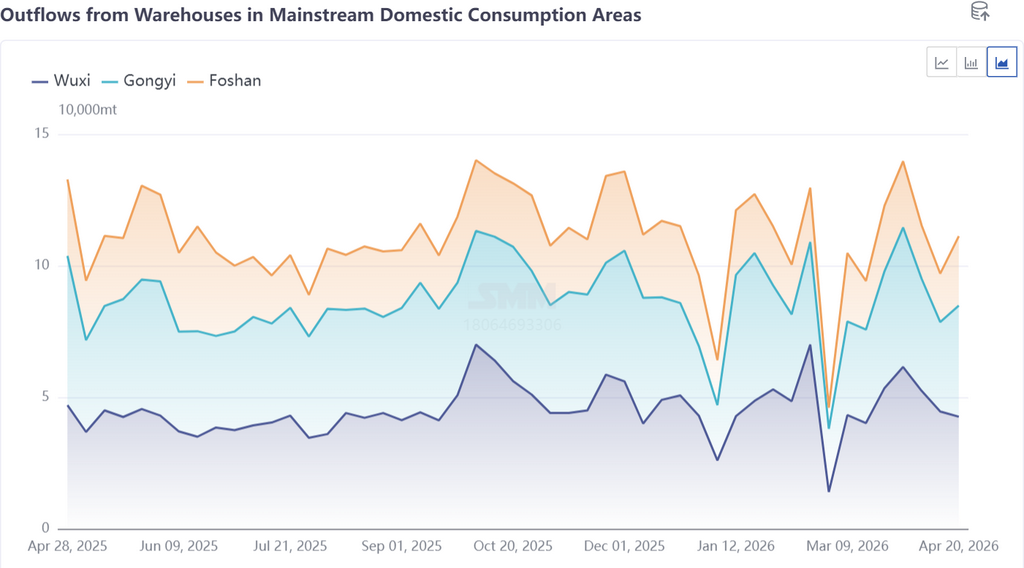

This week, accelerated destocking saw warehouse withdrawals of aluminum ingot in south China rise over 50% WoW, while those in east China increased over 60%. However, a seasonal comparison chart of warehouse withdrawals over the past three years shows that 2026 withdrawals had no significant YoY advantage. The recent surge in withdrawals primarily reflects passive acceptance following a sharp price pullback, rather than a real improvement in demand fundamentals.

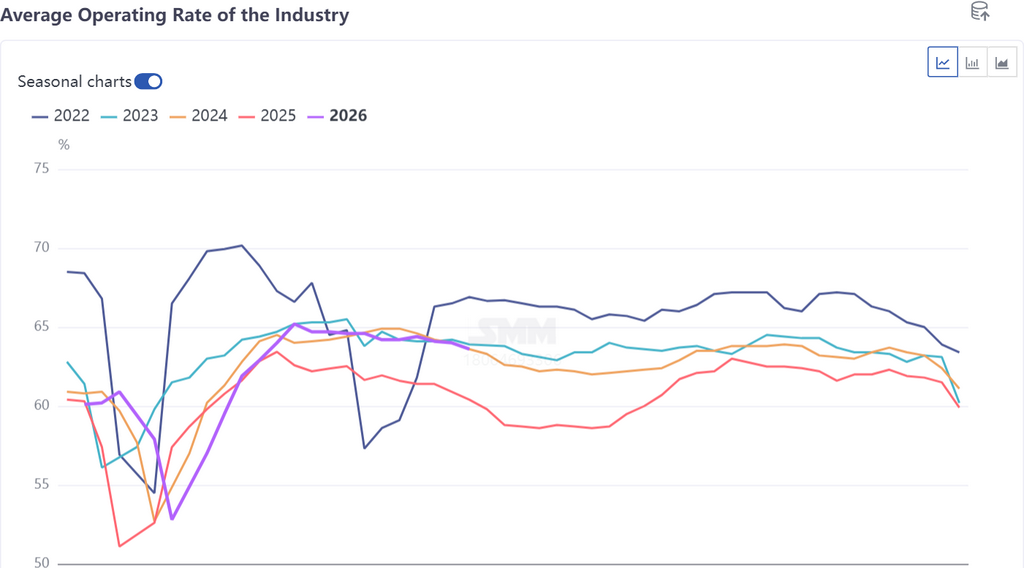

Currently, it is the traditional off-season in China, and domestic end-use demand remains a weakness: the weekly operating rate of aluminum extrusion continues to decline WoW, the pace of domestic demand recovery is relatively slow, and decent export and processing profits do not mean a simultaneous expansion in end-use consumption. Whether warehouse withdrawals can be sustained still needs verification. The trend in aluminum billet inventory will be a coincident indicator to verify the sustainability of aluminum ingot destocking, and should be closely monitored.

Inventory Outlook, June-July: Destocking Trend Established, Pace of Acceleration Uncertain

The destocking trend has been established, with the direction unchanged. A rebounding proportion of liquid aluminum, export demand support, and supply normalization reducing aluminum ingot formation — these three fundamental factors are jointly driving the continuation of destocking. SMM maintains its forecast that inventory will fall to around 1.28 million mt in late June. By late June to early July, it is expected to move closer to 1.2 million mt.

However, the destocking pace should not be linearly extrapolated, and two major risks warrant caution:

Demand-side drivers are relatively passive. The current increase in warehouse withdrawals is mainly driven by restocking triggered by low prices, rather than by proactive expansion by end-users. Once prices stabilize and rebound, the momentum for warehouse withdrawals could weaken marginally. The continued decline in the operating rate of aluminum extrusion and the slowdown in aluminum billet destocking both indicate that a substantial turning point in domestic demand has not yet materialized.

Pressure from regional diversion of supply. Warehouse capacity at delivery facilities in southwest China and south China is already saturated. Some supply has been forced to be diverted to warehouses in east China such as Wuxi. As a result, inventory pressure in east China will remain higher than in other regions, which could periodically drag down the overall pace of destocking.

Key monitoring indicators: 1) Whether the weekly operating rates of aluminum extrusion and aluminum billet stop falling; 2) Whether absolute warehouse withdrawals in China, especially in east China and south China, can stay high; 3) The sustainability of strong export orders; 4) The room for further increase in the proportion of liquid aluminum.

![South China Leads in Basis Repair, Guangdong-Shanghai Spot Cargo Price Spread Narrows to Zero [SMM Analysis]](https://imgqn.smm.cn/production/admin/votes/imagesqsDLb20240416161800.jpeg)