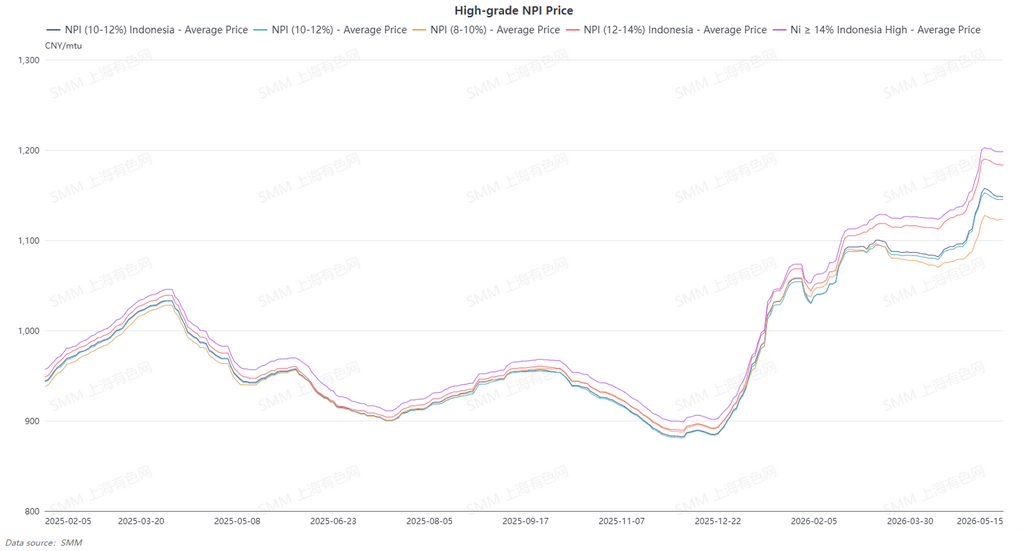

SMM 10-12% high-grade NPI average price fell 4.5 yuan/nickel unit WoW to 1,146 yuan/nickel unit (ex-factory, tax included), while the Indonesian NPI FOB index average price rose 0.97 $/nickel unit WoW to 147.75 $/nickel unit. This week, the high-grade NPI market overall hovered at highs, with significant divergence between sellers and buyers. The price center shifted slightly lower amid the tug-of-war between cost support and weak demand, and overall market sentiment was subdued.

Supply side, cost support underpinned strong willingness to hold prices firm, with high-priced transactions occurring and premiums for high-grade cargoes remaining evident. However, as market sentiment shifted during the week, some enterprises saw marginal weakening in their willingness to hold prices firm due to shipment pressure and arbitrage factors. Combined with weakening stainless steel prices, low-priced cargoes flowed out periodically, market transactions became notably differentiated, and the supply side's price support loosened somewhat. Demand side, weak stainless steel sales, lower steel scrap prices, and weakening futures weighed on sentiment, with strong fear-of-heights sentiment among end-users and cautious purchasing attitudes from downstream steel mills. Looking ahead, the NPI market is expected to maintain a fluctuate-at-highs pattern in the short term. Cost support and tight spot cargo availability provide a floor for prices, limiting significant pullbacks, but downstream stainless steel shipment pace will cap prices.

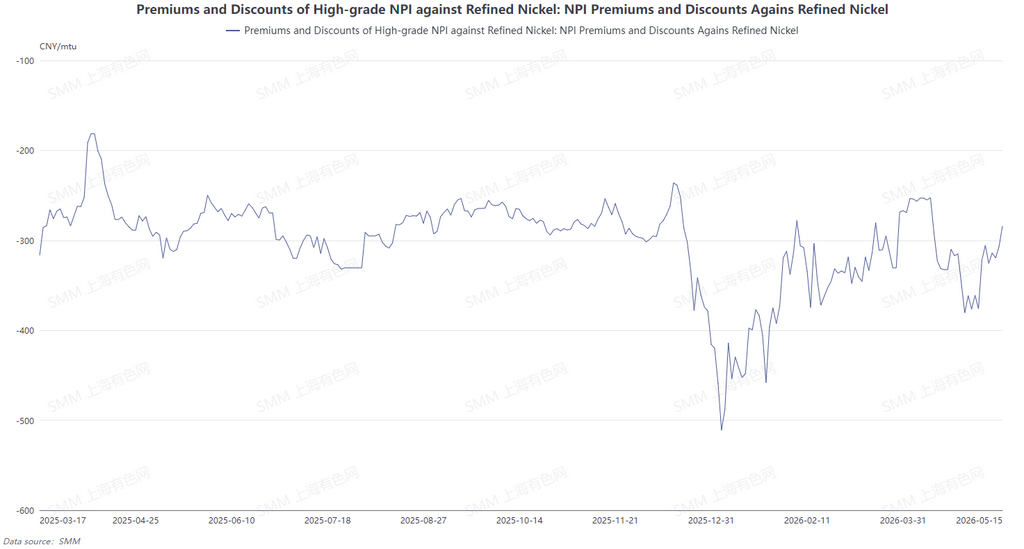

From the perspective of conversion of NPI to high-grade nickel matte, the refined nickel price center moved lower this week, while high-grade NPI prices remained stagnant at highs, and the average discount of high-grade NPI versus refined nickel narrowed to 310 yuan/nickel unit. High-grade NPI prices are expected to remain relatively stable next week, while refined nickel prices are expected to see weakening support and pull back. The average discount of high-grade NPI versus refined nickel is expected to continue converging, reducing profitability of NPI conversion.

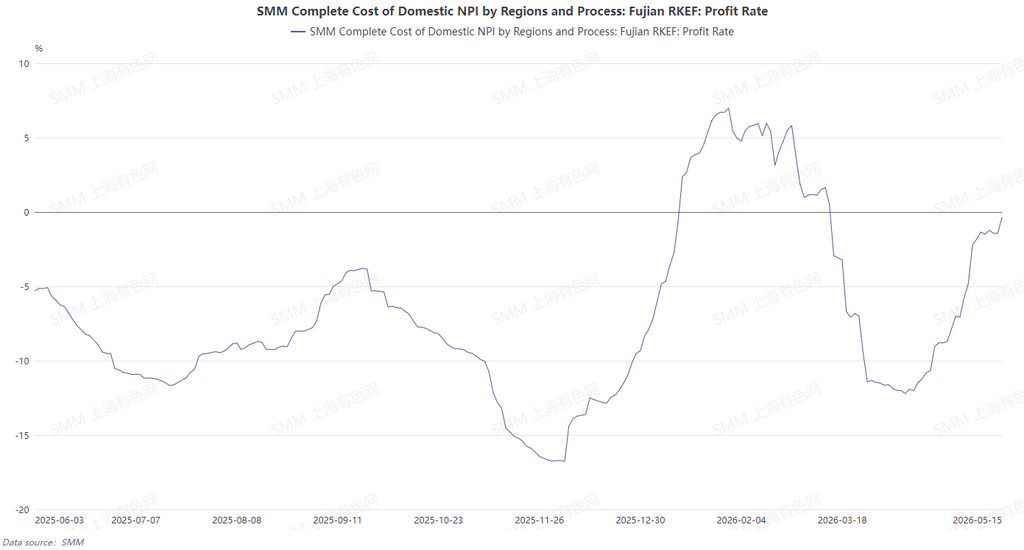

Based on nickel ore prices from 25 days ago for calculating high-grade NPI cash costs, high-grade NPI smelter profits continued to recover during the week. Raw material side, auxiliary material prices rose this week, Philippine nickel ore continued to decline, and Indonesian nickel ore prices recovered somewhat. Overall, the decline in Philippine nickel ore drove down domestic production costs, and China smelter profits continued to expand this week. Next week, high-grade NPI prices are expected to remain unlikely to see significant declines, and smelter profits are expected to be maintained.

![[SMM Analysis] Indonesia's Nickel Benchmark Price Broke Through $18,000 with Strong Momentum, Extreme Weather and Policy Dynamics Intensified Price Divergence](https://imgqn.smm.cn/usercenter/sKmGT20251217171733.jpg)