According to Bloomberg, flooding has caused the collapse of a key bridge located south of the Zambian border in the Democratic Republic of Congo (DRC), cutting off the main copper export route to the Kasumbalesa border post and disrupting outbound shipments from the world’s second-largest copper producer. In a statement released on Sunday, the Zambia Revenue Authority noted that traffic to and from the Kasumbalesa border crossing has been affected due to bridge damage and advised transporters to use alternative routes. According to SMM, this corridor accounts for roughly one-third of the DRC’s refined copper export shipments. At present, cargoes from the southern copper-cobalt belt are being rerouted via the Jiu–Sakania and Mokambo border crossings.

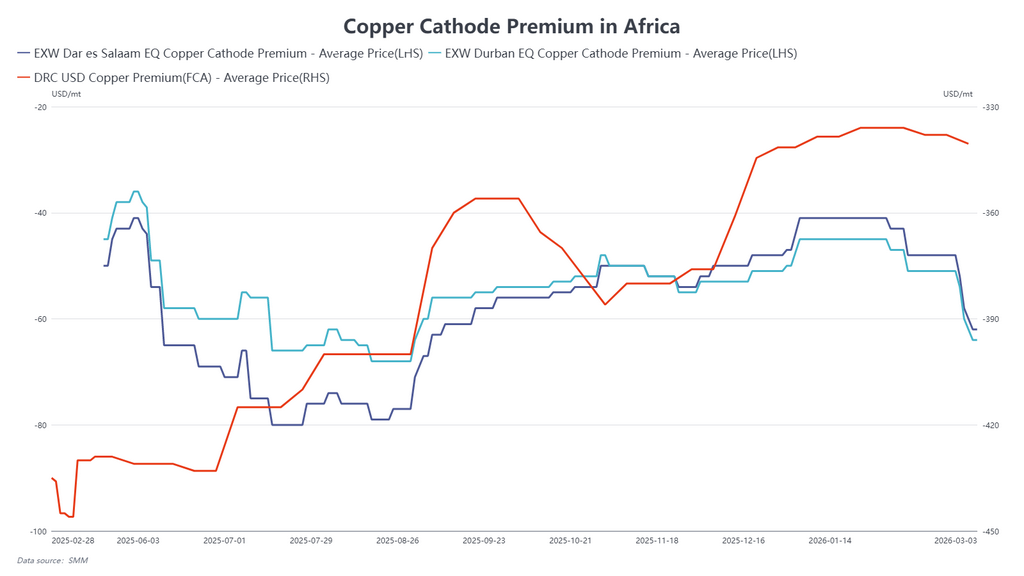

The disruption has had a direct impact on the regional logistics system. Approximately one-third of export volumes that previously transited through Kasumbalesa are now being diverted to the Jiu–Sakania and Mokambo routes. However, these alternative corridors have a daily vehicle capacity of around 1,000 trucks, making it difficult to fully absorb the additional traffic in the short term. Inland freight rates within the DRC are therefore expected to rise, leading to a temporary increase in transportation costs. At the same time, Africa’s smelting structure is predominantly hydrometallurgical and heavily reliant on sulfuric acid imports from Zambia. Any cross-border transport disruptions may further heighten operational risks for hydrometallurgical copper production, increasing localized supply uncertainty. Given that African refined copper premiums have been trending downward recently, this disruption may temporarily slow the pace of premium declines.

From an inventory perspective, reduced transport efficiency may cause refined copper to accumulate at mine sites, smelters, and ports, leading to a short-term buildup of regional “hidden” inventories. As these stocks are not reflected in LME or other visible inventory statistics, they may distort short-term market assessments of global inventory levels and influence expectations regarding the broader supply-demand balance.

For the Chinese market, if logistical bottlenecks persist beyond mid-April, arrivals in the second half of April may slow, potentially resulting in a modest decline in import volumes. However, alternative routes are already in operation, and further developments will depend on improvements in detour efficiency and customs clearance speed. Overall, the incident appears to represent a temporary logistical disruption, with its broader impact on the annual supply-demand structure still to be assessed.