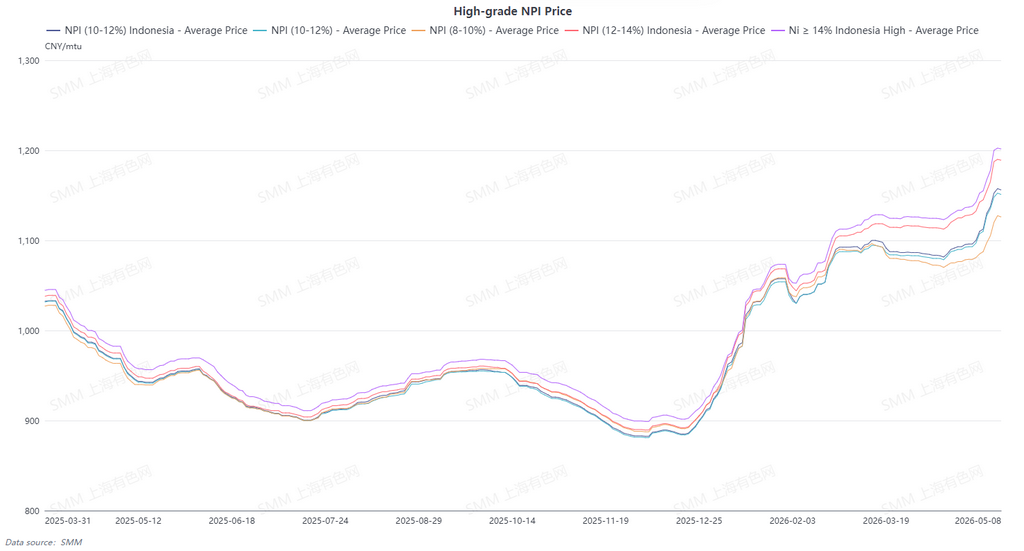

The average price of SMM 10-12% high-grade NPI rose 30.5 yuan/nickel unit WoW to 1,150.5 yuan/nickel unit (ex-factory, tax included), while the average Indonesian NPI FOB index price rose 3.58 $/nickel unit WoW to 146.78 $/nickel unit. This week, policies and futures drove prices steadily higher, with the NPI price center moving further up, but by the end of the week, the market shifted from a one-sided rise to a high-level standoff.

Upstream producers showed strong willingness to hold prices firm during the week, with offers continuously rising. Some enterprises anchored their psychological price level at 1,200 yuan/nickel unit, with strong hold-back-from-selling sentiment. However, downstream steel mills showed weak acceptance of high prices. Steel mills that had completed restocking earlier saw weakened purchase willingness, with maximum purchase intentions capped. Meanwhile, as futures pulled back, fear-of-heights sentiment intensified. Although inquiry activity was moderate, actual trading volume was notably lower than before the holiday. The price spread between high- and low-grade sources also widened further, with increasing divergence in supply structure. Looking ahead, cost support remains, but demand follow-through is insufficient. NPI prices are expected to stay high in a standoff pattern in the near term.

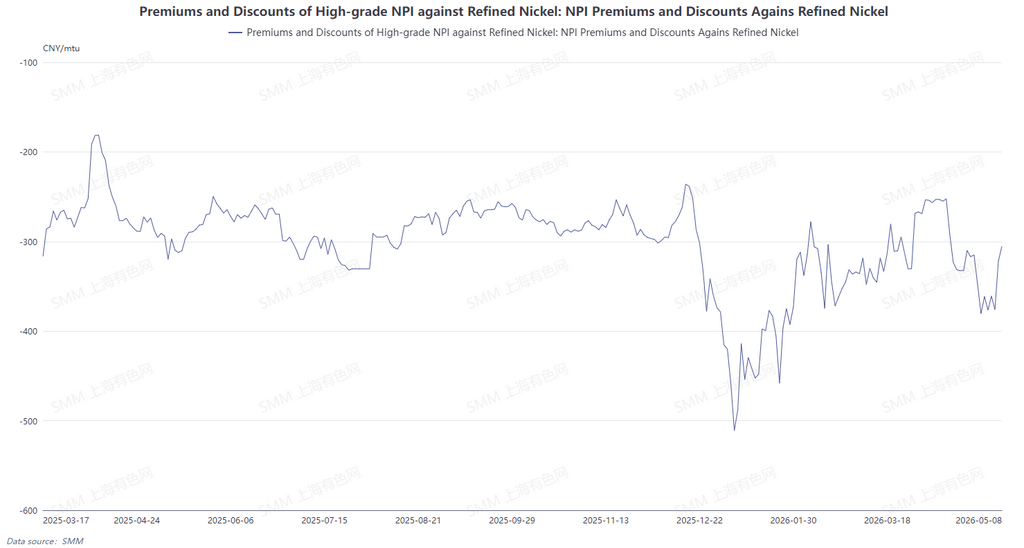

From the perspective of conversion of NPI to high-grade nickel matte, refined nickel prices pulled back from highs this week, while high-grade NPI prices held firm and rose. The average discount of high-grade NPI to refined nickel narrowed to 334.5 yuan/nickel unit. High-grade NPI prices are expected to remain supported by costs next week, while refined nickel prices are expected to see weakened support and pull back. The average discount of high-grade NPI to refined nickel is expected to continue narrowing, reducing profitability of NPI conversion.

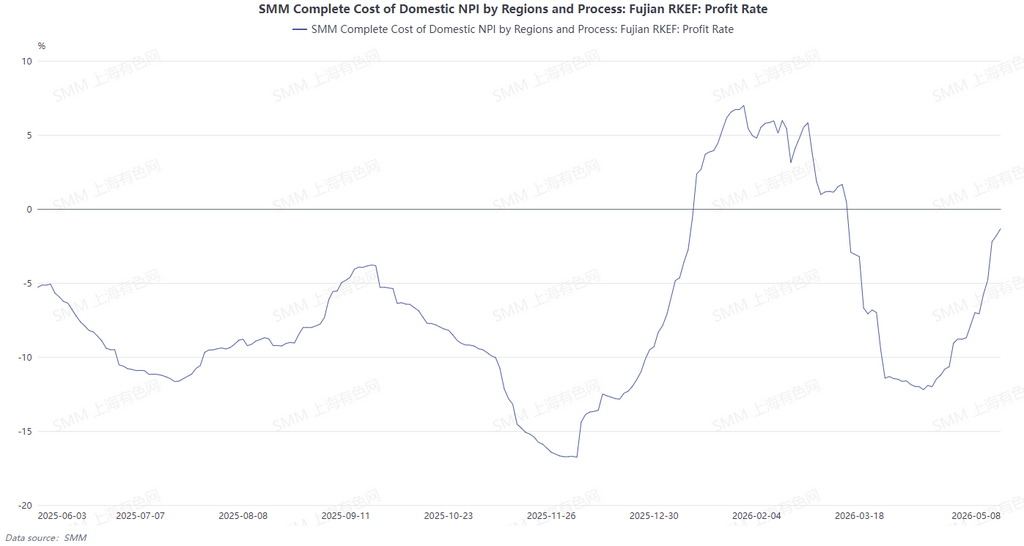

Based on cash costs of high-grade NPI calculated using nickel ore prices from 25 days prior, smelter profits continued to recover during the week, with profitability gradually turning positive. Raw material side, auxiliary material prices rose this week. Ore side, Philippine nickel ore held steady, while Indonesian nickel ore prices saw some pullback. In summary, domestic smelters saw profit expansion this week, mainly driven by the upward shift in the high-grade NPI price center and simultaneous cost reductions. Next week, raw material prices are expected to remain unlikely to rise, high-grade NPI prices are expected to fluctuate at highs, and smelter profit margins may continue to improve.

![[SMM Analysis] Geopolitical Thaw Pulls Stainless Steel Off Multi-Week Highs as Post-Holiday Reality Bites](https://imgqn.smm.cn/production/admin/votes/imagesJgbeN20260508181713.jpeg)