Data: SHFE, DCE market movement (Jul 16)

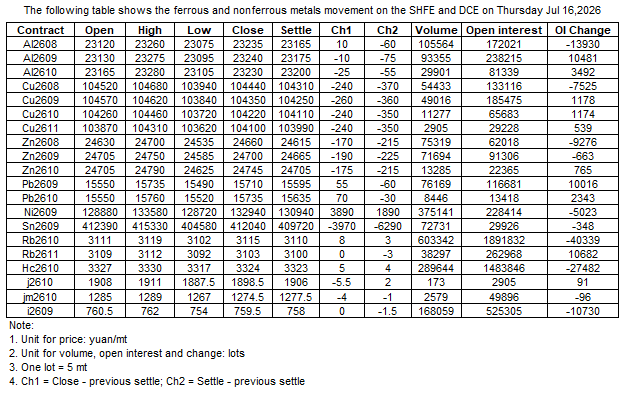

The following table shows the ferrous and nonferrous metals movement on the SHFE and DCE on 16 Jul , 2026

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market communication, and relying on SMM's internal database model. They are for reference only and do not constitute decision-making recommendations.

For any inquiries or for more information, please contact: lemonzhao@smm.cn

For more information on how to access our research reports, please contact:service.en@smm.cn

Related News

Common.Time.hoursAgo

Huahong Technology: H1 net profit expected to rise YoY by 301.84%-352.08% as major rare earth product prices rise

Read More

Huahong Technology: H1 net profit expected to rise YoY by 301.84%-352.08% as major rare earth product prices rise

Common.Time.hoursAgo

Common.Time.hoursAgo

MMi Daily Iron Ore Report (July 17)

Read More

MMi Daily Iron Ore Report (July 17)

The iron ore market traded sideways today, with the DCE main contract I2609 eventually closing at 762 RMB/ton, up 0.53% from the previous day's closing price. Spot prices mostly followed with gains of 0–2 RMB/ton.

Common.Time.hoursAgo

Common.Time.hoursAgo

7.17 SMM Global Steel Daily Report

Read More

7.17 SMM Global Steel Daily Report

[Plate/HRC]HRC export deals at 488-494 USD, flat d/d; overseas fears further downside and delays buying

HRC and other flat-product export prices were flat day on day, with HRC export deals in the 488-494 USD/tonne range. Overseas buyers reckon prices may still have room to fall and prefer to delay purchasing and watch the market even when holding orders, so little actual volume was released.

[Billet]Export billet FOB steady at 458-460 USD ex-Jiangyin; mills hold firm, deals face resistance

Export billet FOB held steady, quoted at 458-460 USD/tonne ex-Jiangyin. Domestic mills held offers firm, while importers' essential demand was soft and buyers' bids sat below sellers' floor, leaving spot deals hard to close and actual trade limited.

[Rebar]Rebar export flat at 480-485 USD; buyers press price and wait, trade thin

Rebar export prices were flat day on day, with deals at 480-485 USD/tonne. Some buyers pressed hard on price and stayed cautious, while domestic sellers, mindful of margins, were unwilling to sell low, so trade saw no meaningful release.

[India]India Mumbai HRC down ~3 USD w/w to 602 USD, monsoon curbs demand

Mumbai HRC fell about 3 USD/tonne week on week to 602 USD/tonne EXW, with transacted prices around 571-611 USD/tonne. Monsoon weather curbed construction and infrastructure demand, keeping spot buying and restocking weak while low-priced cargoes intensified competition; a soft, sideways tone is expected near term.

[Black Sea/CIS]Black Sea billet quiet and steady; Russian mills front-load for Q4 EU tariff-free quota

Black Sea billet trade was quiet with FOB offers steadying and to-Turkey quotes around 495-500 USD/tonne CFR; holidays plus soft demand slowed buyers' pace. Russian mills, racing to secure Q4 EU tariff-free quota, have brought some production forward.

[Indonesia]Indonesia SAE1008 wire rod at 485 USD, below China; SE-Asia off-season keeps trade thin

Indonesia's SAE1008 wire rod export offers held at 485 USD/tonne FOB, clearly below China's comparable ~509 USD/tonne FOB. With Southeast Asia in its seasonal lull, buyers' restocking appetite was limited and, despite the competitive price, actual deals stayed thin.

[Brazil/Vietnam]Brazil HRC import quotes down to 600-610 USD; Vietnam cuts prices, ~20kt booked

Brazil HRC import quotes slipped to 600-610 USD/tonne CFR, with about 20,000 tonnes of flat-product imports booked recently. Vietnam, the core supplier, was forced to cut offers to win orders against low-priced Indonesian and Indian material, while Brazil's strict import quotas and domestic credit tightening capped restocking.

Common.Time.hoursAgo

Related News

Huahong Technology: H1 net profit expected to rise YoY by 301.84%-352.08% as major rare earth product prices rise

Jul 17, 2026 19:22

MMi Daily Iron Ore Report (July 17)

Jul 17, 2026 18:04

7.17 SMM Global Steel Daily Report

Jul 17, 2026 17:57

[Al Yamamah Steel Advances Steel Billet Project]

Jul 17, 2026 17:36