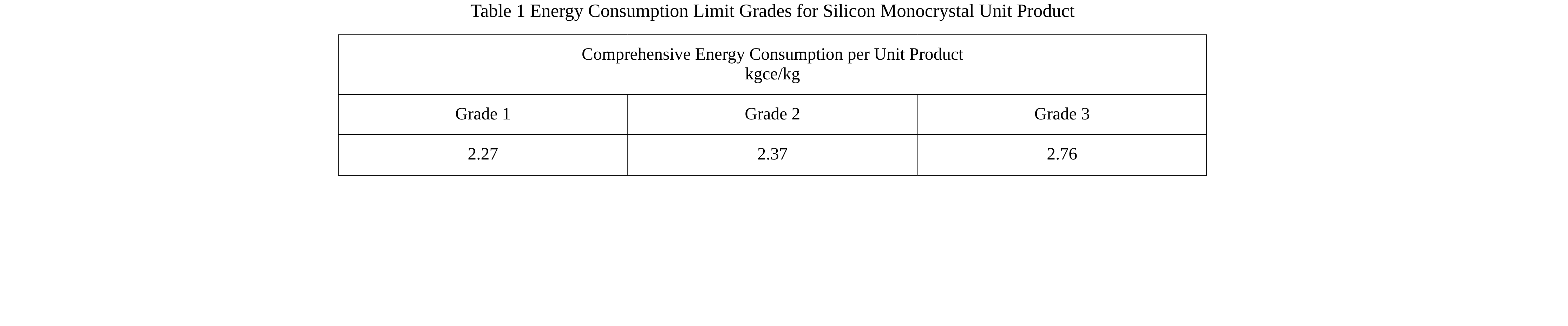

The State Administration for Market Regulation and the Standardization Administration of China jointly issued the mandatory national standard GB 47835-2026 *Energy Consumption Limit per Unit Product of Monocrystalline Silicon* in 2026, which officially takes effect on January 1, 2027. The standard clearly defines three tiers of comprehensive energy consumption quotas per unit product for two categories: monocrystalline silicon and monocrystalline silicon wafers. It adopts 182mm × 210mm (210R) wafers as the benchmark accounting caliber and sets conversion factors for wafers of different sizes, providing a unified compliance basis for energy consumption accounting and energy efficiency evaluation in the industry. The following are the energy consumption quota grades for silicon ingots and wafers:

Note: As the official final version has not yet been made public, the standards from the draft for comments are used.

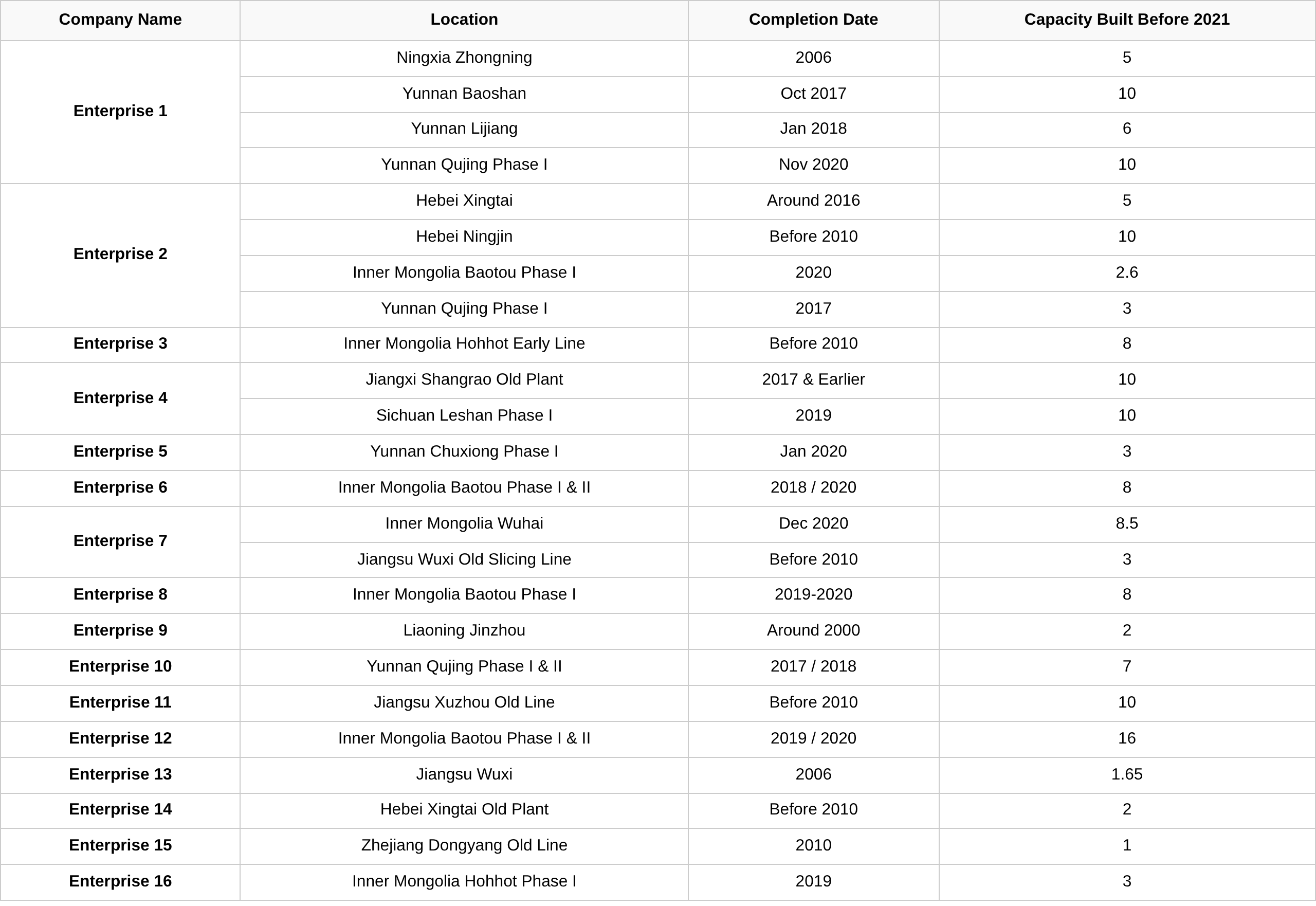

In the chart below, the order of Enterprise 1 to 16 has been shuffled for compliance reasons. In addition, the conversion coefficients for commonly used energy to standard coal equivalent and for commonly used energy-consuming utilities to standard coal equivalent are fixed, but the specific consumption figures of each enterprise are reported by the enterprises themselves and verified by relevant authorities, and the final official published results shall prevail. Therefore, to avoid disputes, I do not use this method to estimate the scale of capacity to be phased out. Instead, I consider production lines for silicon ingots/wafers that were built before 2021 (excluding 2021) and for which no public announcement has been made regarding energy-saving technological transformation or large-size upgrade modifications.

According to SMM statistics, we can calculate that a total of 152.75 GW currently does not meet the Tier 3 energy consumption requirements, accounting for approximately 12.90% of total wafer capacity. This figure excludes overseas capacity of Chinese-funded enterprises (overseas bases in Malaysia, Vietnam, etc., are not subject to mandatory constraints of GB 47835-2026 and are not classified as outdated capacity under China's standards). The mandatory national standard (GB), enforced in accordance with the Standardization Law of the People's Republic of China and the Energy Conservation Law, means that this portion of capacity will have the following impacts:

July 2026 – December 2026:

Enterprises that fail to meet energy efficiency requirements must complete energy consumption verification and energy audits for all production lines, implement energy-saving technology upgrades for lines with retrofit economic viability and obtain third-party compliance detection reports, and orderly promote the shutdown and exit of old production lines with long service life and no technological transformation value. At the same time, they may voluntarily report their rectification plans to the local energy conservation authorities.

From January 1, 2027:

Production lines with energy consumption exceeding Tier 3 limits are in violation of energy use regulations. Local energy conservation authorities will order rectification within a prescribed period in accordance with the law, with the rectification period generally not exceeding six months. If the Tier 3 energy efficiency requirements are still not met after the prescribed rectification period, or in serious cases, the energy conservation authorities shall report to the people's government at the same level and order the enterprise to suspend operations for rectification or even shut down the relevant production lines. There is no flexible "produce first, pay penalties later" approach.

Legal basis: Article 16 and Article 72 of the Energy Conservation Law of the People's Republic of China, and Article 20 of the Measures for Industrial Energy Conservation Supervision.

Conclusion:

In simple terms, after the official release of the *Energy Consumption Limit per Unit Product of Monocrystalline Silicon*, the government grants a six-month rectification period. By January next year, this capacity must either undergo technological transformation and upgrading or exit the market. The most concerning issue for everyone is the enforcement effectiveness of this policy. My view is:

1. The national standard is mandatory.

2. Products that do not meet the requirements will find no buyers, no matter how cheap they are.

3. The policy facilitates market-driven capacity rationalization, with profitability of products serving as the criterion for determining the completion of the rationalization process.

Looking ahead, we expect the wafer segment to complete capacity rationalization from Q4 2027 to Q2 2028. At that point, supply-demand balance will not be achieved, and it will be normal for many production lines to operate below capacity. Publicly listed firms should prioritize shareholder interests; therefore, I mainly use the industry average profit margin to gauge the health of the PV industry's operations.

![[SMM PV Flash] 6 GW! Another Ex-China Topcon Solar Cell Plant Starts Production!](https://imgqn.smm.cn/usercenter/fYlYx20251217171740.jpg)

![[SMM PV Flash] 2.79 Yuan/W! Tianjin 18.81 MW Distributed PV Project EPC Winning Bid Result Publicized](https://imgqn.smm.cn/usercenter/SoBNj20251217171739.jpg)

![[SMM PV Express] Risen Energy received a module order worth 10.73 million yuan!](https://imgqn.smm.cn/usercenter/Pjwqt20251217171738.jpg)