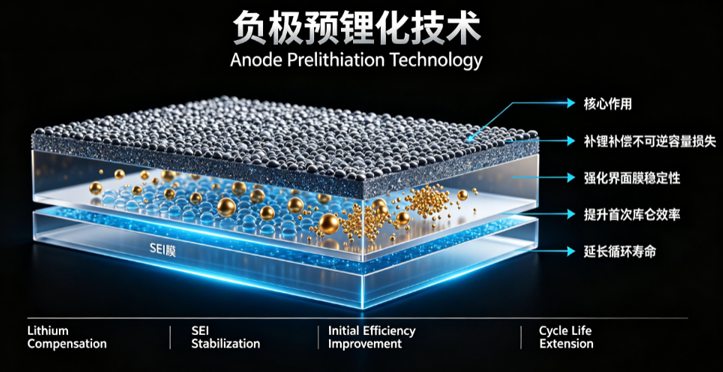

Key Points: Anode prelithiation is a key technology that pre-supplements active lithium into the silicon-based anode to compensate for the irreversible capacity loss during the first charge/discharge, aiming to overcome the industrialization bottlenecks of low initial coulombic efficiency and poor cycling stability of silicon-based anodes.

,

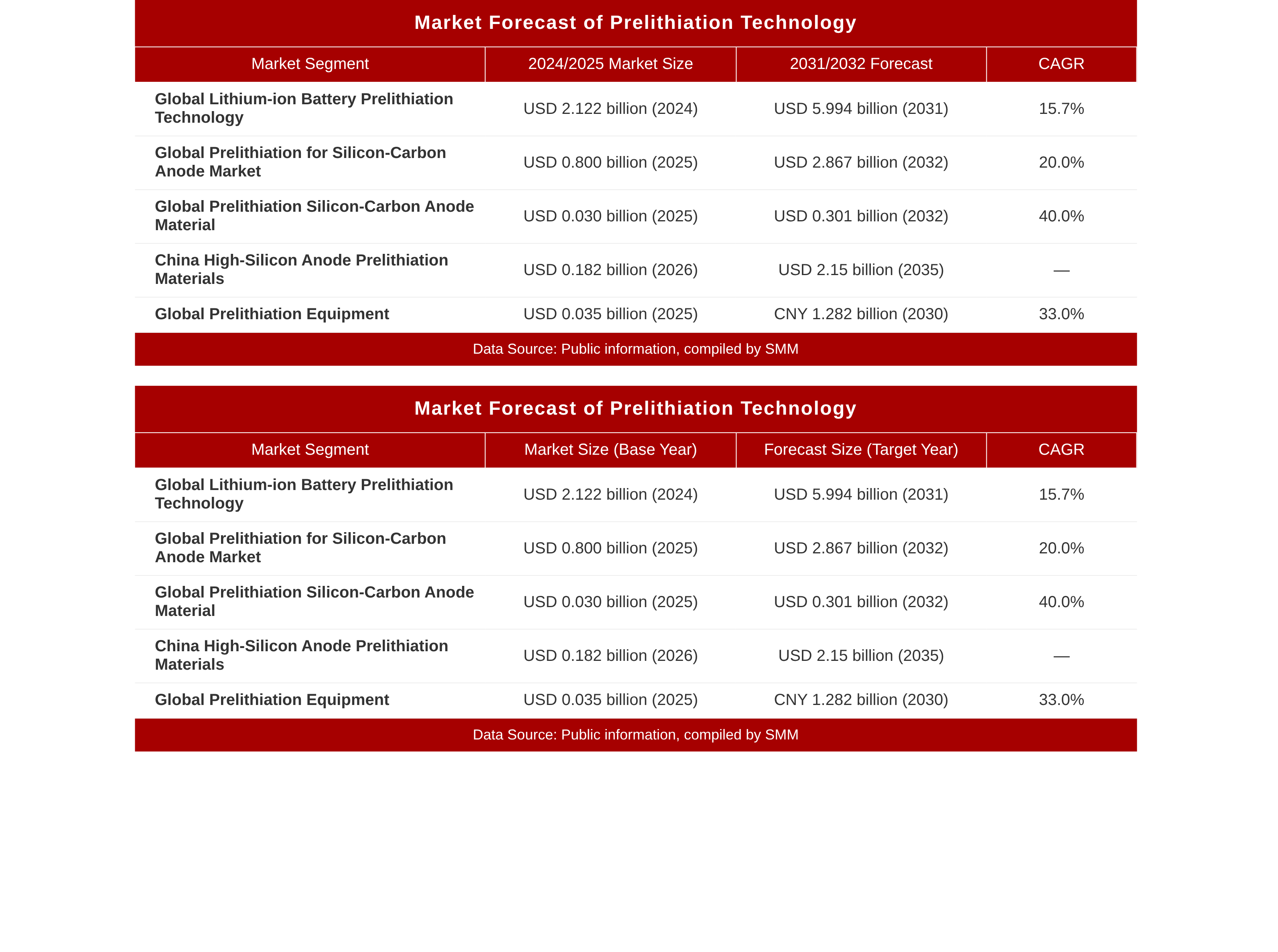

This article systematically reviews four technical routes—lithium foil contact, SLMP powder, chemical prelithiation, and prelithiation additives—analyzes their cost structures and evolution trends, and presents the full-chain industrialization progress from top-level policy design and capacity release at the material end from hundred-tonne to 10,000-tonne scale, to accelerated adoption by top-tier battery enterprises. The study finds that prelithiation technology has become an indispensable common underlying technology for high-specific-energy battery systems, especially semi-solid-state and all-solid-state batteries. Looking ahead, as the price per tonne of silicon carbon anode moves below 80,000 yuan/mt, the prelithiation technology market is expected to grow from approximately $2.1 billion in 2025 to $6 billion in 2031, and continuously penetrate the affordable vehicle market.

Contents

Introduction: Necessity of Prelithiation

Technical Routes: Four Mainstream Approaches

Cost Analysis: Structure and Evolution

Industrialisation: Progress in Policies, Materials, and Batteries

Trends: Route Divergence, Market Penetration, and Vertical Integration

Currently, in solid-state and solid-liquid batteries, anode prelithiation technology is evolving to overcome issues such as large volume expansion and continuous SEI film formation of silicon-based anodes in conventional liquid batteries.

I. Introduction: Why Is Prelithiation Needed?

During the first charge of a lithium-ion battery, a solid electrolyte interphase (SEI) film forms on the anode surface, irreversibly consuming active lithium ions from the cathode and causing capacity loss. For conventional graphite anodes, this loss is about 5%–10%; for silicon-based anodes, due to their huge volume expansion (about 300%) during charge/discharge, the SEI film repeatedly cracks and reforms, leading to more severe active lithium loss, and the initial coulombic efficiency (ICE) is often only 70%–80%.

With a theoretical specific capacity of up to 4,200 mAh/g, over ten times that of conventional graphite anodes (372 mAh/g), silicon-based anodes are recognized as the core anode material for next-generation high-energy-density lithium-ion batteries. However, the two major bottlenecks—low initial coulombic efficiency and poor cycling stability—have long constrained their practical application. Prelithiation technology—introducing additional lithium sources into the anode system before battery assembly to compensate for the irreversible lithium loss in the first cycle—is the key means to overcome this bottleneck.

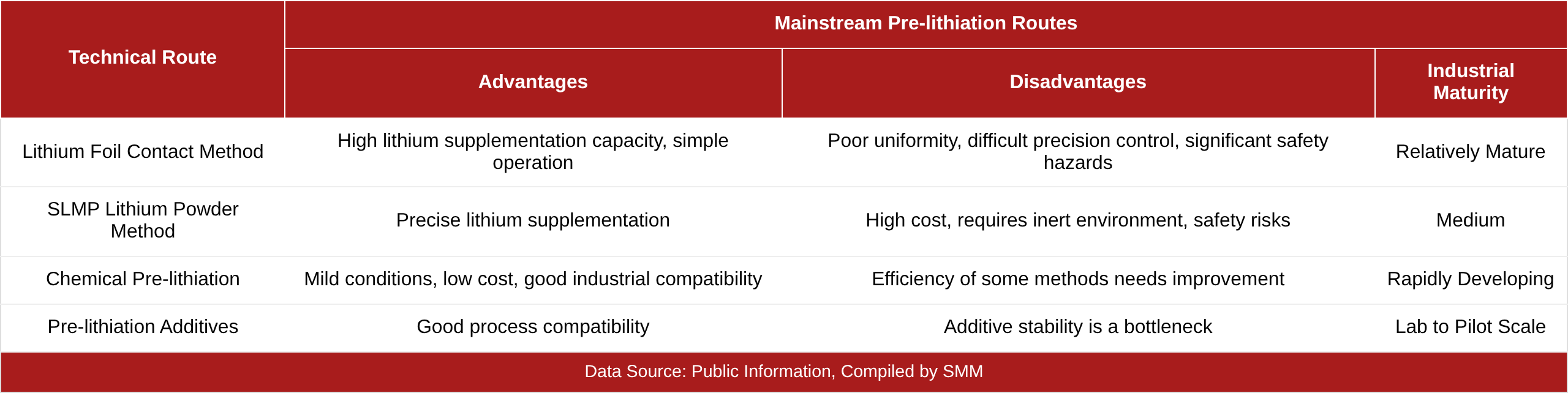

II. Technology Overview: Analysis of Mainstream Prelithiation Routes

2.1 Technical Classification Framework

Pre-lithiation technology, based on the method of introducing the lithium source, can be divided into two major categories: anode pre-lithiation and cathode lithium supplementation. Anode pre-lithiation is the mainstream approach with faster industrialisation progress, mainly including the following technical routes: lithium foil contact pre-lithiation, stabilized lithium metal powder (SLMP) pre-lithiation, chemical pre-lithiation, and pre-lithiation additives

2.2 Lithium Foil Contact Pre-lithiation

By directly pressing and contacting lithium foil with the anode electrode sheet, the potential difference between lithium metal and the anode material is exploited to enable spontaneous lithium intercalation into the anode. This method features simple operation and high lithium supplementation capacity, but the degree of pre-lithiation is difficult to control precisely: insufficient pre-lithiation leads to limited improvement in initial coulombic efficiency, while excessive pre-lithiation may form a metallic lithium plating layer on the anode surface, affecting battery performance. In addition, lithium foil has extremely stringent environmental requirements, poses safety hazards, and demands high equipment standards.

2.3 Stabilized Lithium Metal Powder (SLMP) Pre-lithiation

Stabilized lithium metal powder with a surface-coated passivation layer (such as Li₂CO₃) is mixed with anode slurry for coating. Compared to lithium foil, lithium powder allows easier control of the pre-lithiation degree and more precise lithium dosage. However, the chemical reactivity of lithium powder remains relatively high, making practical operations challenging and similarly requiring an inert environment.

2.4 Chemical Pre-lithiation

The anode is soaked in chemical reagents (such as polycyclic aromatic lithium reagents, lithium-biphenyl solution, etc.), achieving pre-insertion of lithium through chemical reactions. The chemical pre-lithiation method is mild, low-cost, and compatible with industrial production, showing considerable application potential. The “salt-free medium-mediated” contact pre-lithiation strategy developed by the team of Professor Sun Yongming at Huazhong University of Science and Technology utilizes the spontaneous reaction between the medium and lithium metal to generate lithium ions in situ, achieving spatially and temporally uniform pre-lithiation within the electrode.

2.5 Pre-lithiation Additives

Lithium-containing additives are directly introduced during the preparation of anode materials. The environmentally stable lithium-silicon alloy pre-lithiation additive developed by the team of Shao Huaiyu at the University of Macau can increase the initial coulombic efficiency of silicon oxide anode materials from 78% to 98.1%. This type of method offers good process compatibility but demands extremely high stability of the additive.

2.6 Comparison of Various Technical Routes

Chart: Mainstream Pre-lithiation Routes

3. Cost Analysis: Economic Viability as the Core Bottleneck of Industrialisation

3.1 Cost Composition

The comprehensive cost of anode pre-lithiation is approximately 80–150 yuan/kWh, which can increase battery energy density by 15%–25%. The cost breakdown is roughly as follows:

Material cost (lithium source): accounts for about 60%, the largest cost item

Equipment depreciation:accounts for about 15%

Labour and energy consumption: accounts for about 10%

Environmental control cost:accounts for about 15% (inert atmosphere, dehumidification, etc.)

The lithium source cost accounts for 10%–15% of the total battery material cost. The high price of lithium metal, coupled with the stringent environmental control requirements for lithium foil/powder, significantly drives up battery cell costs.

3.2 Cost Evolution Trends

Large-scale production is significantly reducing costs. Capacity plans of top-tier players have surpassed the 10kt level, with per-unit costs dropping by over 60% compared to 2020. In 2025, the industry's capacity utilization rate reached 73%, and the average gross margin stood at approximately 35%.

In 2025, global production of prelithiated silicon carbon anode material reached 362 mt, with an average price of approximately $83,000/mt. With technology iteration and mass production, costs are expected to decrease by more than 40% by 2030.

3.3 Economic Challenges

Despite the declining costs, prelithiation technology still faces multiple economic challenges:

Lithium Source Price Fluctuations: The price of lithium metal is significantly affected by the upstream lithium carbonate market, introducing uncertainty in cost pass-through.

Process Complexity: Issues such as the poor stability of prelithiation agents and insufficient compatibility with battery systems are driving process complexity higher.

Safety Costs: The reactive nature of lithium metal demands strict environmental controls, increasing production line investment and operational costs.

Cost Reduction Target: The industry generally believes that the price of silicon carbon anodes must drop below 80,000 yuan/mt to enable large-scale replacement of graphite anodes.

4. Industrialisation Progress: From Hundred-Ton to Ten-Thousand-Ton Scale

4.1 Policy Support

The national “15th Five-Year Plan” has listed silicon-based anode materials as one of the core strategic R&D directions in the new energy sector. This policy orientation provides top-level support for the industrialisation of prelithiation technology.

4.2 Material End: Rapid Capacity Release

Sichuan Tiannuo Juneng: In December 2025, the first phase of its hundred-ton high-performance prelithiated silicon oxide material project at the Suining base officially commenced production, with an investment of 30 million yuan, achieving an annual capacity of 500 mt of prelithiated silicon oxide and 50 mt of silicon carbon products. The product model TNSO1580 has a specific capacity of approximately 1,580 mAh/g, an initial coulombic efficiency of about 89%, and retains over 80% capacity after more than 1,200 cycles. The product has entered the small-batch procurement stage for several power battery enterprises.

Lianchuang Lithium Energy: One of the few domestic enterprises mastering prelithiated silicon oxide technology, it has completed land acquisition for a 10,000 mt/year production line. Equipment installation and commissioning for the first-phase 2,000 mt line is underway, with production expected to commence in H2 2026.

BTR: As an early entrant in the silicon-based anode space in China, it already possesses a silicon-based anode capacity of 12,500 mt/year.

Other Layouts: Qingdao Zhengwang’s CVD silicon carbon anode products have rolled off the production line; the first-phase project of Inner Mongolia Guiyuan Xinneng’s 20,000 mt/year silicon carbon anode production has commenced operations; Lanzhou Zhide completed its D+ round of financing, with exclusive strategic investment from CATL’s Puquan Capital.

4.3 Battery End: Top-Tier Players Accelerate Introduction

Currently, dozens of companies across the global battery industry chain are involved in the R&D of silicon-based anode materials. Top-tier battery producers such as CATL, EVE, Gotion High-tech, Farasis Energy, Sunwoda, and SVOLT Energy Technology are all actively introducing silicon-based anodes.

CATL: Secured third-generation vapor-phase silicon carbon anode technology through an investment in Lanzhou Zhide.

Sunwoda: Has extensively applied silicon carbon anode battery processes in the consumer electronics sector, with a silicon blending ratio of 5%-10% in consumer products in 2024, expected to rise to 10%-15% in 2025.

EVE: Has filed patents related to prelithiated silicon-based anodes.

4.4 R&D Breakthroughs: From Laboratory to Industrialisation

The Team of Shao Huaiyu at the University of Macau: Developed an environmentally stable lithium-silicon alloy prelithiation additive that boosted the initial coulombic efficiency of silicon oxide anodes from 78% to 98.1%. Kilogram-scale trial production has been completed, and joint verification is underway with domestic top-tier lithium battery enterprises.

The Team of Zou Ruqiang at Peking University: Proposed an in-situ anode lithium replenishment and cathode near-surface fluorination reconstruction strategy, driving a commercial breakthrough for high-energy-density anode-free lithium metal batteries.

The Team of Wu Jianfei at the Qingdao Institute of Bioenergy and Bioprocess Technology: Proposed a synergistic “prelithiation-fortress” strategy involving “basalt-like porous silicon + Li₁₃Si₄,” achieving significant progress in enhancing the performance of silicon anode sulphide-based all-solid-state batteries.

5. Future Scale and Trends

5.1 Market Size Forecast

Chart-: Prelithiation Technology Market Forecast

5.2 Penetration Rate Forecast

Assuming significant increases in penetration rates and blending volumes, global consumption of silicon-based anode materials (pure material) will grow substantially from 2027 to 2030. The consumer electronics sector has become the first large-scale application scenario for silicon-based anodes; in the power battery sector, silicon anodes have achieved a leap forward.

5.3 Key Trends

Trend 1: Divergence and Convergence of Technology Routes

High-end CVD silicon carbon anodes, with their structural design advantages, can substantially reduce reliance on prelithiation, thereby lowering additional costs. This means that future prelithiation technology will diverge: the low-end silicon oxide route will rely on prelithiation to improve initial coulombic efficiency, while the high-end silicon carbon route will seek to minimize prelithiation dependence. At the same time, the convergence of prelithiation technology with solid-state batteries is accelerating—prelithiated silicon oxide materials are particularly well-suited for high-energy-density liquid, solid-liquid hybrid, and all-solid-state battery technology routes.

Trend 2: Penetration from High-End to Mass-Market Segments

Prelithiated silicon-based anodes are currently used mainly in high-end digital products, high-end EVs, and solid-state batteries, and they are expected to penetrate the mass-market vehicle segment after 2028. As costs continue to decline and capacity is released, the penetration rate of silicon-based anodes in the power battery sector is anticipated to exceed 15%.

Trend 3: Accelerated Vertical Integration of the Industry Chain

From upstream raw materials such as silicon metal, silane, and porous carbon, to midstream prelithiation processes, and downstream battery manufacturing, enterprises across all segments of the industry chain are accelerating their deployment and integration. Battery giants like CATL are locking in upstream technologies through strategic investments, while material companies are seizing market share through capacity expansion.

Trend 4: Cost Reduction Is the Eternal Theme

The industry consensus is that the price per mt of silicon carbon anode needs to fall below 80,000 yuan. Large-scale production, process optimization, and technological advances will jointly drive cost reductions, with costs expected to decline by over 40% from current levels by 2030. Only when costs fall to a reasonable range can prelithiated silicon-based anodes truly achieve large-scale substitution for graphite anodes.

VI. Conclusion

Anode prelithiation technology is at a critical turning point from technical verification to mass production. On the policy side, there is strategic support from the “15th Five-Year Plan”; on the supply side, capacity is being released from the hundred-tonne to 10,000-tonne level; and on the demand side, leading battery enterprises are accelerating adoption. The global prelithiation technology market was approximately $2.1 billion in 2025, and is projected to reach $6 billion by 2031.

However, the path to industrialisation is not without obstacles. High lithium source costs, process complexity, safety risks, and cost reduction pressures remain barriers to be overcome. Over the next five years, whoever can achieve breakthroughs in all three dimensions—cost control, technical precision, and large-scale capabilities—will gain first-mover advantage in the next-generation anode material competition. Prelithiation technology is not only relevant to the industrialisation of silicon-based anodes but also critical to whether lithium-ion batteries can break through the 300 Wh/kg energy density ceiling and enter a new era of 400 Wh/kg or even 500 Wh/kg.

Tel: 021-20707860 (or add WeChat 13585549799) Yang Chaoxing, thank you!

Related Information

![[SMM Analysis] Demand Boost Lifted Anode Production in June, Enterprises Prioritized Destocking Under Cost Pressure](https://imgqn.smm.cn/usercenter/MjfPv20251217171728.jpg)

![[SMM Analysis] Rio Tinto’s Q2 Lithium Output Up 20% YoY](https://imgqn.smm.cn/usercenter/MyEcZ20251217171727.jpg)

![[SMM Analysis] Global Lithium to Buy IGO’s Nova Assets for Manna Lithium Development](https://imgqn.smm.cn/usercenter/KnMyT20251217171727.jpg)