SMM Apr 8 News:

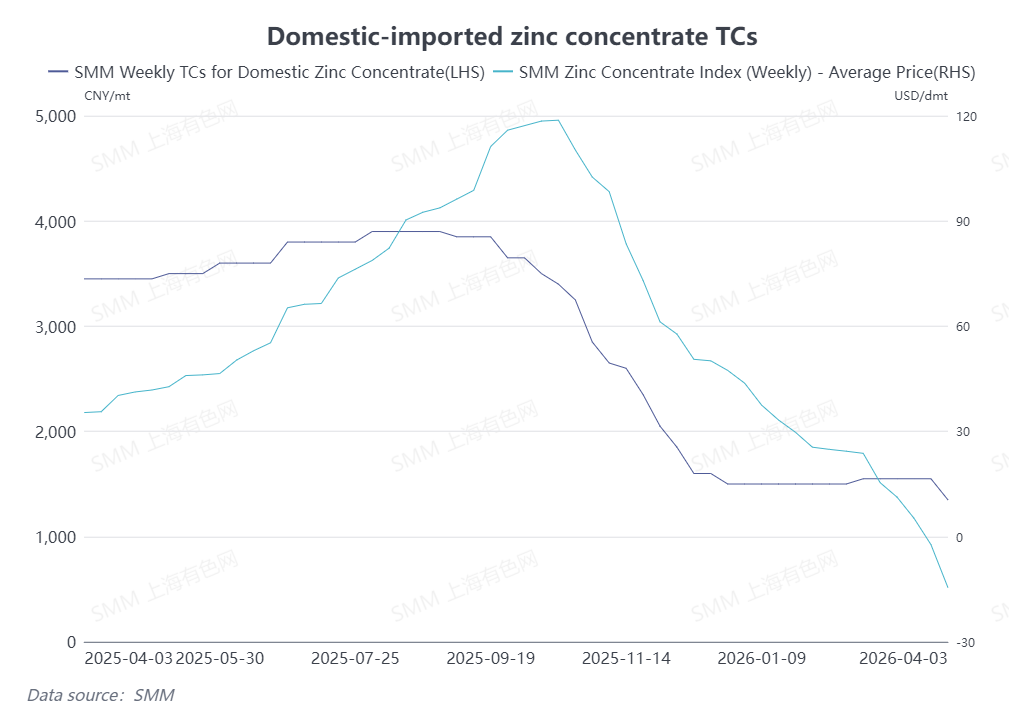

As of April 3, the average domestic zinc concentrate TC dropped to 1,350 yuan/mt in metal content, and the imported zinc concentrate TC fell to -$14.5/dmt, with the import market once again entering negative territory. After Chinese New Year, domestic mines gradually resumed production — so why did zinc concentrate TCs decline again in April?

First, let's look at the import market. In Q1, frequent disruptions occurred at the ex-China ore supply side. Starting from February, hindered transportation affected parts of Australia due to severe weather such as floods and typhoons. Subsequently, at the end of February, Middle East conflicts re-escalated, affecting the shipment of Iranian zinc concentrates. Based on shipping cycle estimates, these disruptions are expected to impact zinc concentrate arrivals in China in Q2. In addition, production guidance for ex-China zinc concentrates has been released one after another this year. The Garpenberg mine lowered its production guidance for this year due to an earthquake, and overall ex-China zinc concentrate production is expected to decline YoY this year. Market expectations for a tighter overall balance have strengthened, and coupled with periodic transportation disruptions, imported zinc concentrate TCs have declined rapidly in recent weeks.

Now let's look at domestic zinc concentrate TCs. Although domestic lead-zinc mines gradually recovered in March and April after Chinese New Year, and SMM expects zinc concentrate production to continue growing MoM in April, the import market remained tight. Moreover, domestic zinc concentrates still held a price advantage, and domestic smelters actively purchased domestic zinc concentrates. Demand side, rising sulphuric acid prices in China continued to supplement smelter profits, and domestic smelters maintained high production enthusiasm. Domestic refined zinc production in April is expected to continue rising, with overall robust market demand for zinc concentrates. Against this supply-demand backdrop, the increase in domestic zinc concentrate TCs was hindered in April.

Overall, affected by supply-side disruptions, the domestic zinc concentrate market experienced periodic tightness in supply and demand recently. Imported zinc concentrate TCs continued to decline, but domestic lead-zinc mines are gradually recovering in Q2. SMM will closely monitor the subsequent supply-demand pattern and TC trends.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)

![Easing Middle East Tensions Released Positive Sentiment, SHFE Zinc Opened Higher with a Gap Today [SMM Zinc Futures Brief]](https://imgqn.smm.cn/usercenter/ipTIN20251217171755.jpg)

![Galvanizing Operating Rates Were Weaker YoY in Q1, Will Q2 See a Turnaround? [SMM Analysis]](https://imgqn.smm.cn/usercenter/EviJV20251217171754.jpg)