SMM News, April 7:

In Q1 2026, China's secondary lead market navigated through turbulence amid holiday effects and industry difficulties. Following a sharp production decline of over 140,000 mt in February, the market saw a post-holiday recovery rebound in March, but the recovery fell short of expectations, with the industry mired in the dual constraints of "profit pressure and tight raw material supply." Looking ahead to April, although large smelters are expected to resume production in a concentrated manner, concerns over off-season demand weakness combined with imported lead inflows may significantly discount production gains. Key attention should be paid to the maintenance and production shutdown plans of large smelters in east China.

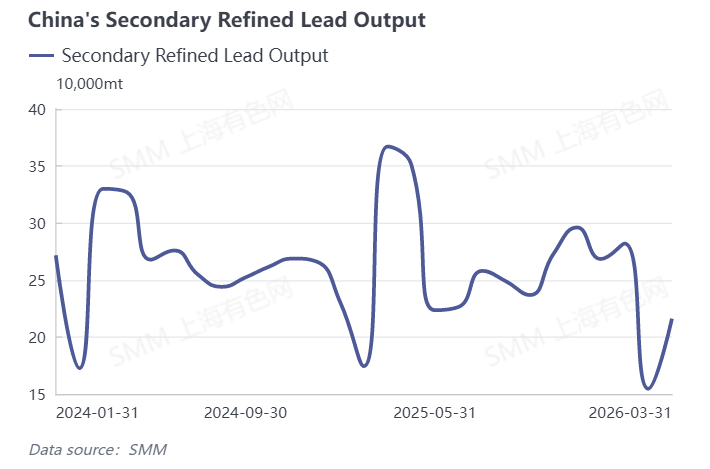

I. March Production Data: Significant Rebound MoM, Deep Decline YoY

The latest data showed that secondary lead production in China achieved a recovery growth as expected in March 2026, up 27.75% MoM, but due to a high base and industry sluggishness, it decreased significantly by 36.17% YoY. Among this, secondary refined lead production increased 39.83% MoM and declined 41.11% YoY.

Key drivers behind the March production rebound:

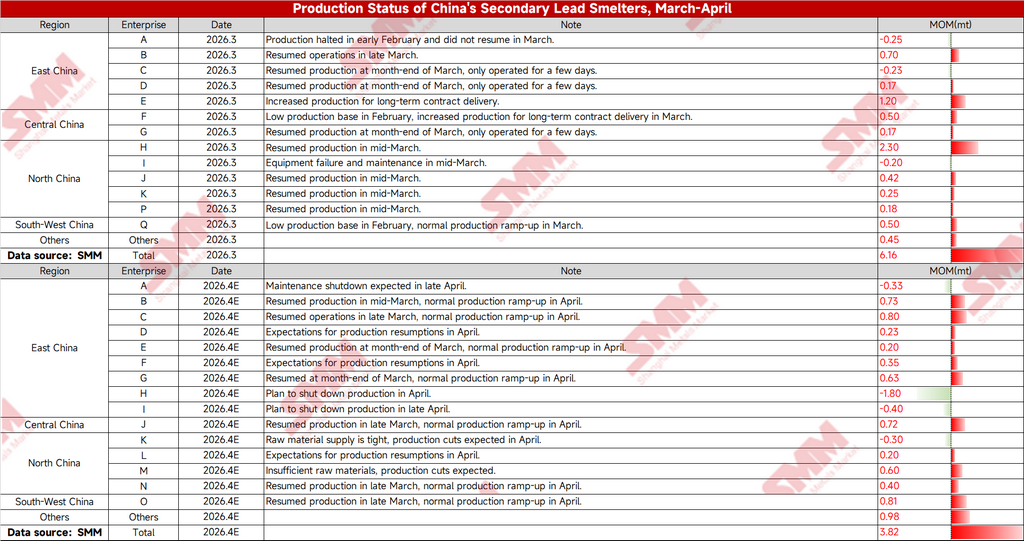

(1) Concentrated post-holiday production resumptions: After the Lantern Festival, workers gradually returned to their posts. Combined with the ultra-low base in February, smelters in major producing regions such as Jiangsu, Henan, and Inner Mongolia began to resume production in a concentrated manner from mid-to-late March, serving as the core driver of the production rebound.

(2) Inventory and order-driven: Downstream battery enterprises slowly resumed operations after the holiday and began to digest lead ingot inventory accumulated before the holiday. Some secondary lead enterprises were compelled to raise operating rates to fulfill long-term contract obligations and ensure delivery.

(3) Easing of raw material constraints: The scrap battery recycling market gradually recovered along with the resumption of work, smelter raw material inventory received some replenishment, and the persistently tight raw material supply situation improved to some extent.

Core contradictions constraining the recovery momentum in March:

(1) Sustained profit losses: Scrap battery prices remained elevated in March, while lead prices were in the doldrums. The theoretical profit-loss values for large-scale enterprises remained in negative territory, with small and medium-sized enterprises suffering even greater losses, severely suppressing enterprises' willingness to proactively increase production.

(2) Tight raw material supply: Scrap battery recyclers lagged in resuming operations, and the sentiment to hold back from selling was strong. Raw material supply had not fully recovered, becoming a key bottleneck limiting the improvement of operating rates. (3) Slow demand recovery: The downstream battery industry saw overall weak demand, slow finished product destocking, and lead ingot purchases driven mainly by rigid demand. Purchase willingness fell short of the same period in previous years, making it difficult to form strong support.

II. April Outlook: Expected Increment of 38,000 mt, Actual Delivery in Question

1. Bullish driver: Production resumptions at large smelters to provide incremental supply

Secondary refined lead production in April is expected to increase by 38,000 mt MoM. The main support comes from the capacity side: multiple large secondary lead smelters in north China, east China, and north-west China plan to resume production in a concentrated manner from late March to early April, releasing considerable incremental capacity.

2. Bearish factors: Triple pressure from maintenance, supply, and demand

Capacity offset: Some large smelters in east China have scheduled routine maintenance shutdowns during the same period, partially offsetting the new production.

Ample supply: Imported lead ingots continued to flow into the Chinese market, maintaining an overall loose lead supply pattern and squeezing domestic smelters' production space.

Weakening demand: The traditional consumption off-season is approaching, and downstream battery enterprises' operating rates and lead ingot purchase willingness are expected to decline. If demand continues to weaken, it will directly undermine smelters' production enthusiasm, and the actual production increment in April will fall below the 38,000 mt expectation.

III. Market Summary

The MoM rebound in secondary lead production in March was an inevitable result of post-holiday production resumptions, but the significant YoY decline revealed the industry's deep-seated challenges. In April, the market will be caught in a tug-of-war between "production resumptions at large smelters" and "weakening demand in the off-season plus the impact of imported lead." Against the backdrop of margins yet to turn positive, raw materials yet to loosen, and demand yet to recover, the industry's "weak recovery" pattern is unlikely to change. April production is expected to maintain an upward trend, but the extent to which the incremental output materializes requires close attention to the actual performance of downstream demand.