Chinese stainless steel futures drifted lower this week (June 22–26, 2026) under the combined weight of a residual hawkish tone from the Federal Reserve and seasonally weakening fundamentals, before stabilizing in a narrow range near the lows. The SHFE main contract closed at RMB 14,670/mt ($2,158/mt) at the 10:15 a.m. break on Friday, June 26 — down RMB 390/mt ($57/mt) on the week. The defining feature of the week was a clear divergence between paper and physical: futures bore the brunt of the macro overhang and off-season expectations, while spot prices, supported by tightening supply and disciplined producer pricing, did not follow the contract lower.

Macro: hawkish concerns ease at the margin, but Fed officials remain divided

Overseas, fears around an imminent Fed rate hike eased somewhat after May U.S. PCE data came in broadly in line with expectations — headline PCE at 4.1% year-on-year and core PCE at 3.4% year-on-year. The dollar index snapped a three-day winning streak, closing down 0.1%. However, absolute inflation remains uncomfortably high, and Fed officials are visibly split on the path forward: Chicago Fed President Austan Goolsbee maintained a hawkish stance, arguing that underlying inflation is still too high, while New York Fed President John Williams pushed back his expectation for hitting the 2% target to 2028. With monetary policy direction unclear, the macro tailwind for risk assets was limited.

Domestically, the People's Bank of China conducted a RMB 500 billion ($73.5 billion) one-year Medium-term Lending Facility (MLF) operation — a routine liquidity injection to anchor medium-term funding conditions in the Chinese banking system. The operation supported sentiment but provided little direct lift to the futures market. Net of both factors, macro forces offered marginal support to the contract this week, but were not enough to override the broader weak tone.

Fundamentals: inventories flat, off-season grip tightens, spot transactions thin

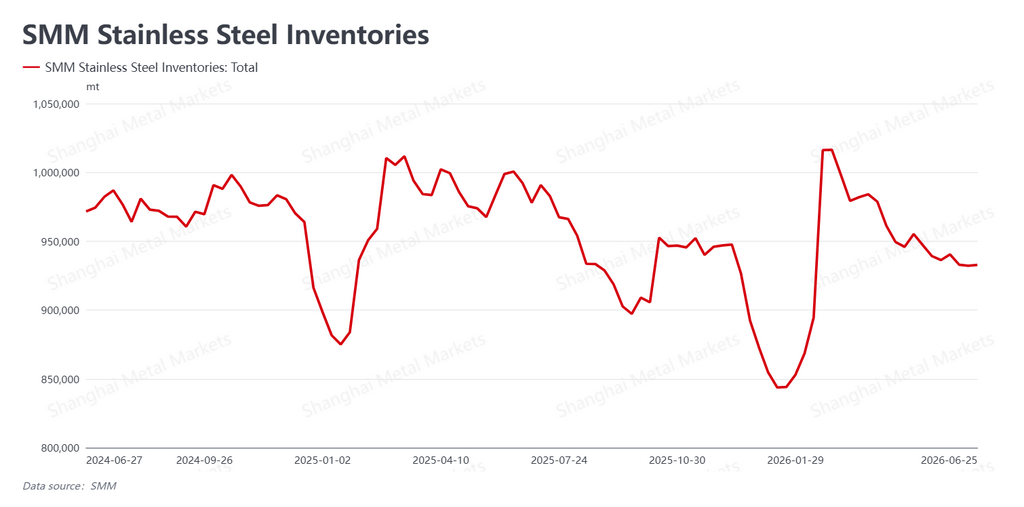

Stainless steel social inventory — the aggregate volume held at major Chinese distribution hubs such as Wuxi (Jiangsu) and Foshan (Guangdong) — finished the week at 932,800 mt, essentially unchanged from the prior week (+600 mt). With Chinese end-use demand now in its traditional summer off-season, inventories are neither drawing down further nor accumulating noticeably; destocking momentum has clearly faded. That said, the absolute inventory level remains relatively low by historical standards, providing a soft floor for physical prices.

In the spot market, firm producer determination to defend prices, combined with a marginal pullback in mill output, kept physical quotations from following futures lower. The futures-spot divergence widened accordingly. However, off-season buying remains weak — end-users are reluctant to chase prices and prefer to wait for further declines — leaving market liquidity thin and forward order books soft. The demand side of the equation is offering progressively less support.

Cost and supply: raw materials weaken on both fronts; ample supply still caps the upside

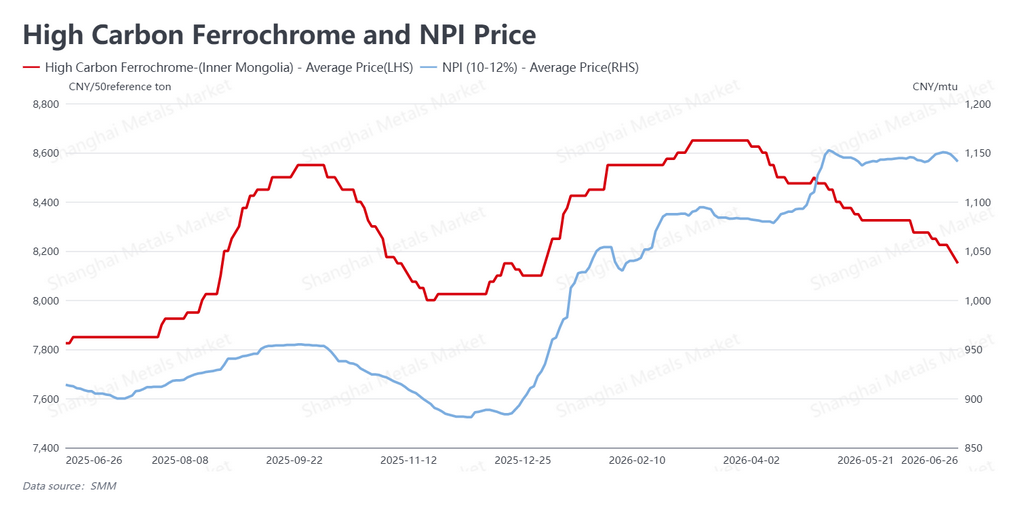

Raw material prices fell on both legs of the stainless steel cost stack. High-carbon ferrochrome — priced in China on a 50% chromium-content basis — was quoted at RMB 8,150/50-base mt ($1,199/50-base mt), down RMB 75 ($11) on the week, extending its downtrend at an accelerated pace. Nickel pig iron (NPI) — the laterite-derived low-grade ferro-nickel alloy that dominates stainless feedstock in China and Indonesia — was assessed at RMB 1,141/nickel unit ($168/nickel unit), down RMB 8.5 ($1.25) week-on-week, reversing its earlier rebound. (In Chinese trade convention, NPI is priced per "nickel unit," meaning per percentage point of contained nickel per metric ton.) With both ferrochrome and NPI weakening in tandem, cost support for stainless steel has eroded meaningfully versus the prior week.

On the supply side, scheduled mill maintenance and delayed restarts trimmed Chinese stainless output modestly this month, providing some support to physical prices. The cuts, however, are limited in scale. Falling raw material costs are also cushioning mill margins — profitability remains acceptable, and the incentive to keep producing is intact. The structural picture of ample Chinese stainless supply has not changed, and that supply overhang remains the primary constraint on any sustained upward move in prices.

Outlook: weak oscillation around the lows; macro and raw materials set the pace

Looking ahead, U.S. inflation stickiness remains intact, Fed officials are visibly divided, and the policy path is unclear. The pending ruling in the Federal Reserve Governor Lisa Cook case — a closely watched legal matter with implications for Fed governance and independence — is expected next week and could introduce fresh volatility. Macro signals will continue to set the short-term tone for the contract.

Domestically, with China firmly in its traditional off-season, end-use demand is weak and transactions are light. Whether spot prices can sustain their resilience will depend on the durability of mill price discipline and the extent of further output cuts. The simultaneous softening of ferrochrome and NPI has weakened cost support, but the structural surplus in stainless supply remains in place.

SMM expects the SHFE main contract to remain in a weak, range-bound pattern in the near term, with repeated probing of the lows. Marginal changes in macro signals and raw material prices will dictate the rhythm.

Written by Bruce Chew

Nickel & Stainless Steel Analyst, Shanghai Metals Market

Email: bruce.chew@metal.com

Tel: +601167087088

![[SMM Flash News] Canada Nickel Appoints SB1 Markets to Arrange Up to US$600M Debt Financing for Crawford Project](https://imgqn.smm.cn/usercenter/PFIti20251217171734.jpg)

![[SMM Flash News] Swelect Energy Acquires 49% Stake in Gridnex Solar Power to Expand Indian PV Portfolio](https://imgqn.smm.cn/usercenter/WYeHX20251217171733.jpg)

![[SMM Analysis] Nickel Salt Prices Show Weakness, Intermediate Product Coefficient Under Pressure in the Short Term](https://imgqn.smm.cn/usercenter/JjbtE20251217171732.jpeg)