SMM, July 15:

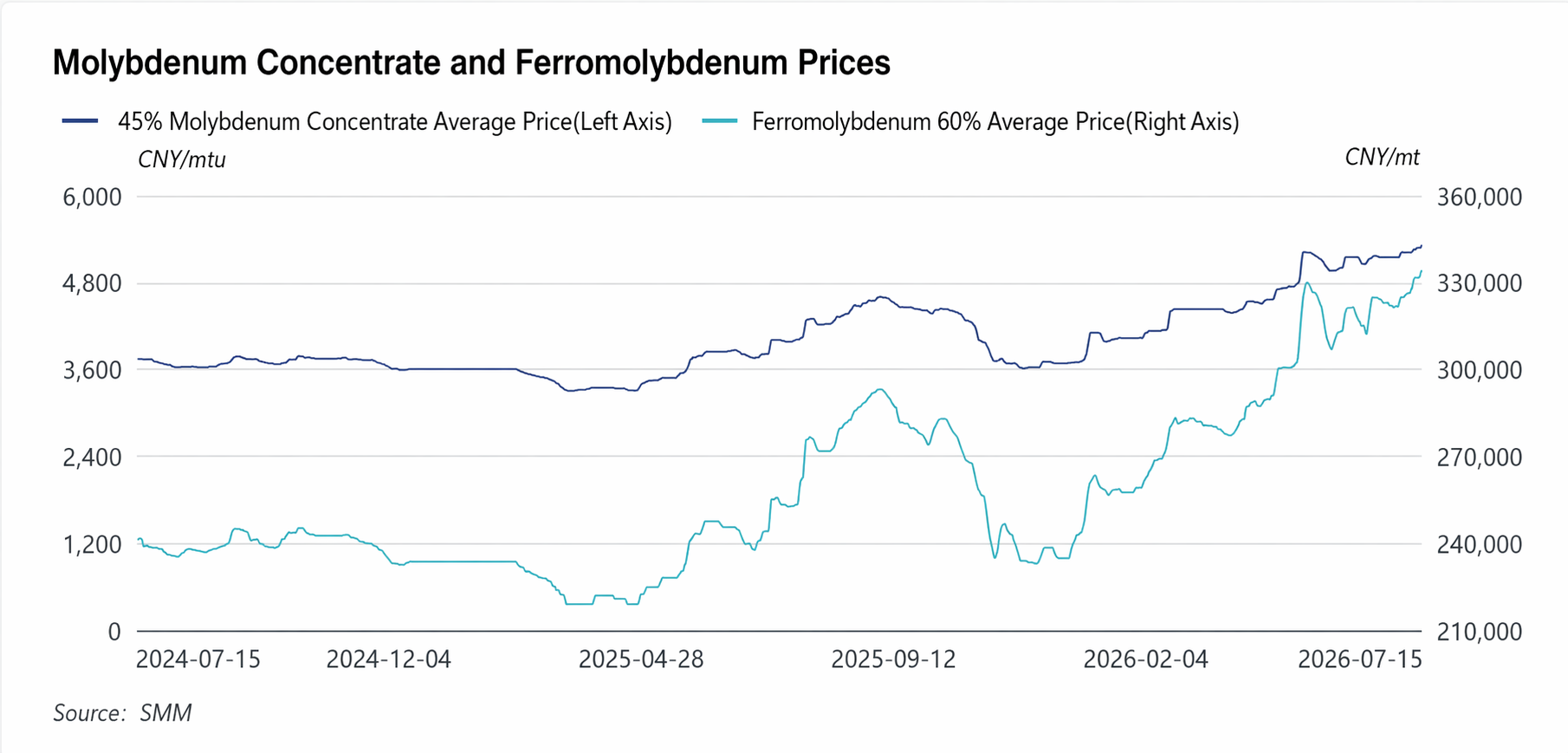

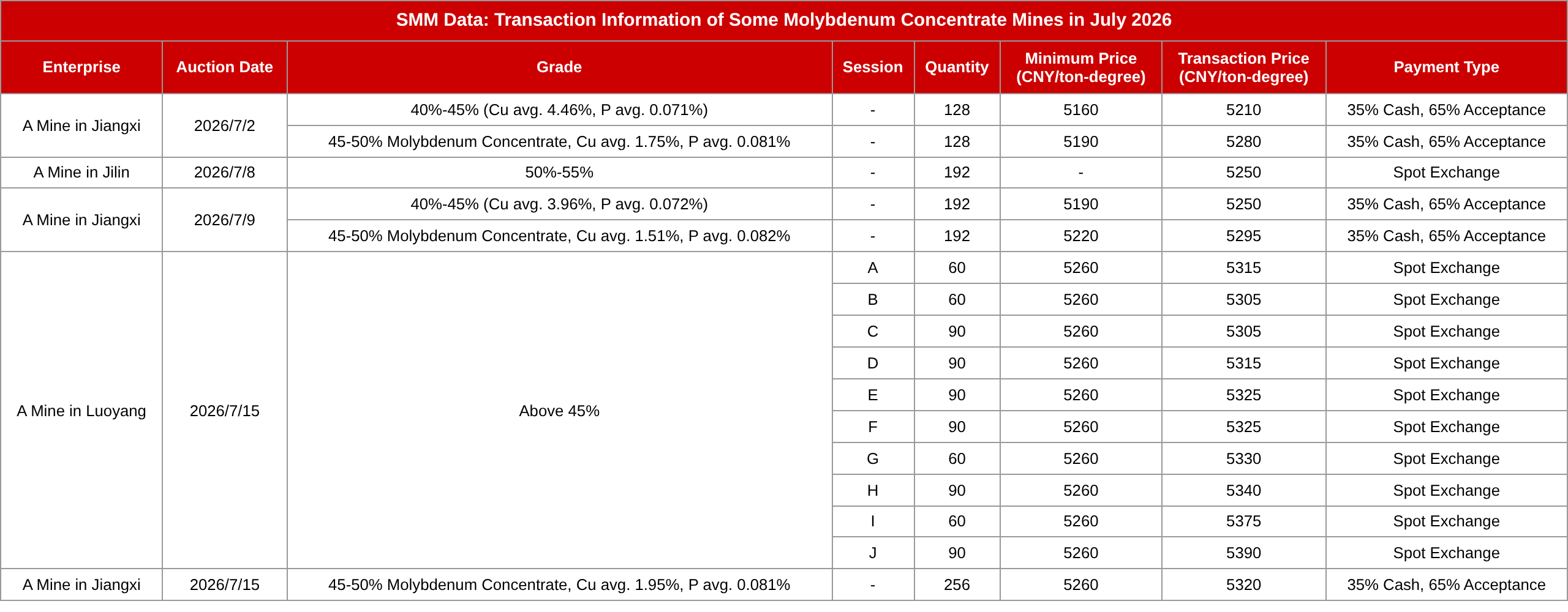

Major domestic mines launched public tenders for molybdenum concentrates today, with all rounds fully settled at premiums. Futures prices rose steadily and transaction performance was strong, breaking the traditional off-season weakness and showing a typical strong off-season rally and tight spot supply trend. Looking at the specific transaction details, a large Luoyang mine sold 810 mt of molybdenum concentrates via tender. The tender floor price was 5,260 yuan/mtu, and all material was sold at transaction prices ranging from 5,305 to 5,390 yuan/mtu, with a weighted average transaction price of approximately 5,334 yuan/mtu. Meanwhile, a large Jiangxi mine listed 256 mt of 45%-50% grade molybdenum concentrates via tender. The ore quality indicators were excellent (average copper 1.95%, average phosphorus 0.081%), and the tender also anchored on a floor price of 5,260 yuan/mtu, ultimately settled at 5,320 yuan/mtu. The price center for domestic molybdenum concentrates moved significantly higher. As of the morning of July 15, the SMM 45% molybdenum concentrate price closed at 5,300-5,330 yuan/mtu, up 30 yuan/mtu from the previous day and up 36.8% from the beginning of the year. Overall, the premium space for tenders was stable and the material sold quickly, fully reflecting a futures market characterized by active just-in-time procurement downstream, scarce low-priced material, and strong panic buying sentiment.

The core reason for the current high and firm molybdenum prices comes from a continuously intensifying supply-demand tight balance . On the supply side, domestic molybdenum mine output is constrained by stricter environmental protection and safety inspections and tight mining quotas, resulting in limited incremental mine release. With no new large-scale capacity coming online, spot circulating material remains tight. Traders and mines are widely holding back from selling, and low-priced supply has almost disappeared. Outside China, declining ore grades at major producing mines and persistent geopolitical and labor disruptions continue to tighten global molybdenum supply, further supporting the resilience of China’s spot prices. Molybdenum concentrate prices outside China are consolidating at highs, with international molybdenum oxide prices consolidating at highs at $31.7/lb of molybdenum, while the domestic import window remains shut, lending some support to the domestic raw material spot market.

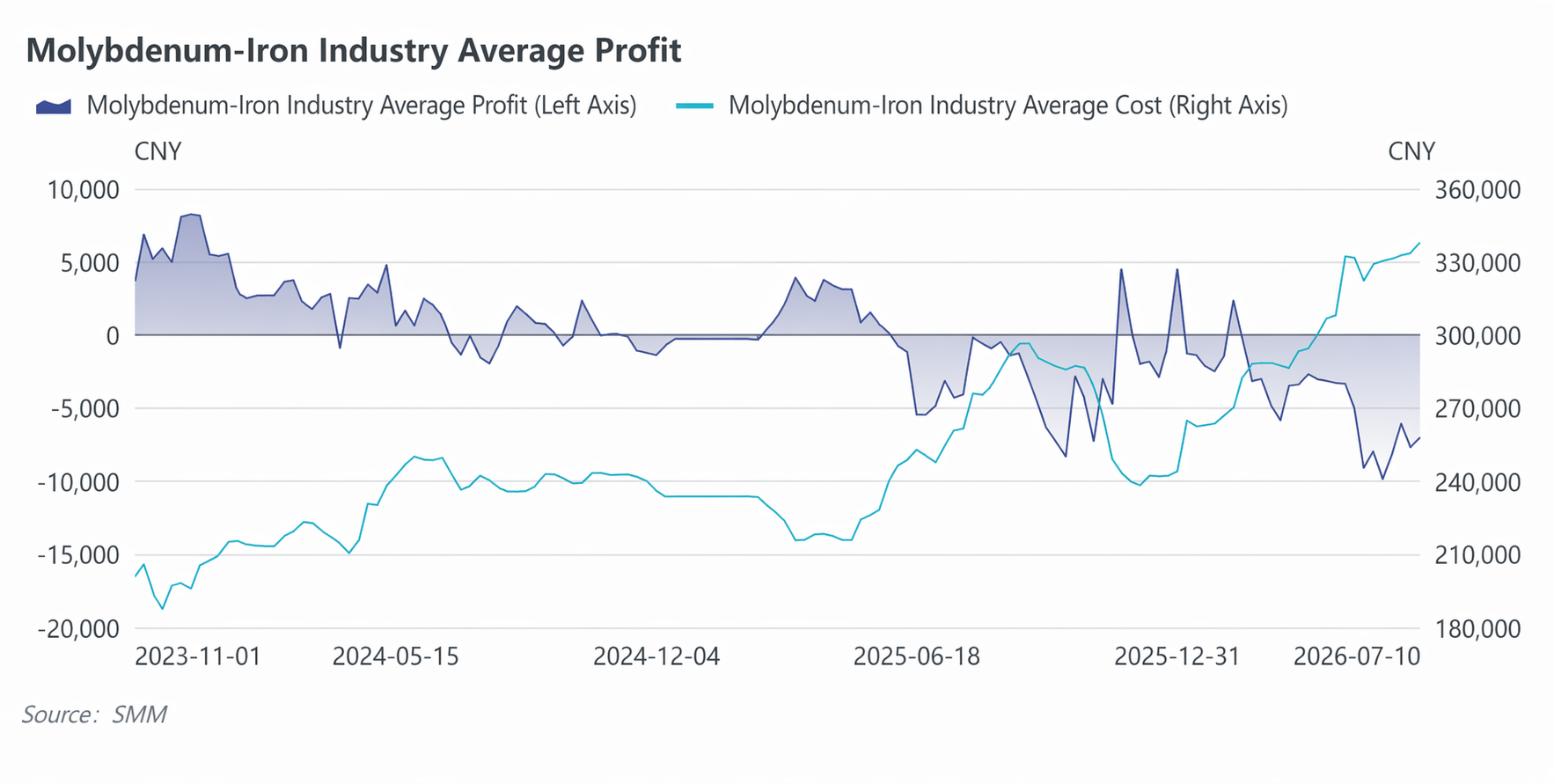

Support on the demand side is also strengthening, with upstream and downstream prices rising in tandem. Both molybdenum concentrates and ferro-molybdenum moved up together, lifting the broader industry chain’s prosperity. Core downstream product ferro-molybdenum saw quotations rise again today, with mainstream domestic spot offers concentrated at 330,000-338,000 yuan/mt . Producers generally raised quotations to levels above 335,000 yuan/mt. Steel mill tender prices moved up steadily, with recent steel mill tender transaction prices holding at high levels of 328,500-329,000 yuan/mt, fully supporting just-in-time procurement. Downstream steel mills and molybdenum smelters have largely depleted the low-priced inventories built earlier, and the restocking pace continues to accelerate. The high transaction prices for molybdenum concentrates are being transmitted directly to the ferro-molybdenum segment, with smelting costs providing strong support. This, combined with the approach of the traditional peak season for stainless steel and special steel in Q3, has heightened end-user pre-stocking sentiment, allowing them to fully accept high-priced upstream concentrates without any resistance or weak transaction activity. The two-way support from both upstream and downstream has laid a solid foundation for further price increases. As of today, SMM ferromolybdenum closed at 334,500 yuan/mt, up 2,500 yuan/mt from yesterday, with a year-to-date cumulative increase of 30.4%, underperforming the molybdenum concentrates raw material market. Based on the current transaction prices in steel tenders, the industry remained in a severe inverted state.

Overall, the molybdenum industry chain was set to continue thepattern of dual strength in concentrates and ferromolybdenum, consolidating on a strong note at elevated levels.Upstream mines saw tight spot cargo supply and unchanged sentiment to hold back from selling, with high-priced premium transactions for concentrates becoming the norm; downstream ferromolybdenum was supported by both rising costs and rigid demand from steel mills, leaving prices with ample resilience. Absent negative macro and policy shocks, prices of both products were expected to remain firmly at high levels in the short term; as end-users advanced concentrated restocking, there was still upside room for a slight rise

![[SMM Chromium Daily Review] Ore Prices Rebound Slightly, Ferrochrome Remains Stable for Now](https://imgqn.smm.cn/usercenter/pAOxy20251217171725.jpg)

![Aluminum alloy futures move sideways, spot demand insufficient, prices held steady awaiting market direction [ADC12 Price Daily Review]](https://imgqn.smm.cn/usercenter/ZVhtl20251217171724.jpeg)