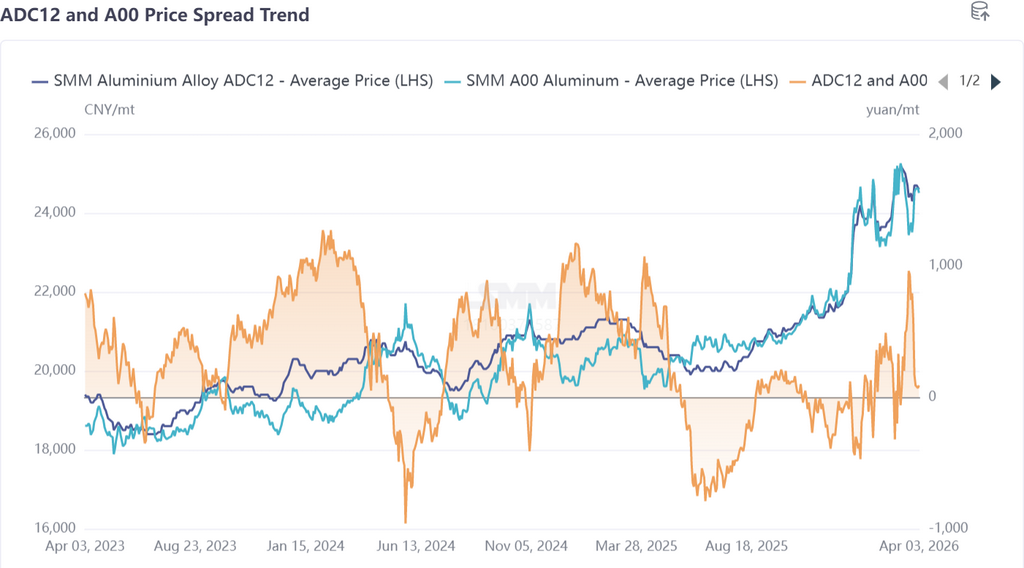

First, a review of the price trend of secondary aluminum alloy in March: Futures market: The most-traded cast aluminum alloy contract showed pronounced volatility in March—surging sharply in early March to a high of 24,565 yuan/mt; retreating from highs from mid-March, with a low of 22,230 yuan/mt; and rebounding again at month-end, forming an overall "N"-shaped pattern. Entering April, the market shifted to moving sideways, with prices trading in the 23,500–24,000 yuan/mt range.

Spot market: Strength in aluminum prices in early March drove ADC12 sharply higher, while in mid-to-late March it fluctuated downward under pressure from pulling back aluminum prices and weakening demand, before rebounding slightly at month-end. As of April 3, SMM ADC12 was quoted at 24,600 yuan/mt, up a cumulative 700 yuan/mt from early March. Price spread: After mid-March, A00 aluminum prices pulled back, while ADC12, supported by costs, saw relatively limited declines, and the price spread widened for a time; at month-end, A00 rebounded on Middle East disruptions, but weakening ADC12 demand caused it to struggle to catch up, and the price spread narrowed rapidly. It has now pulled back to within 100 yuan/mt, at a relatively low level for the same period.

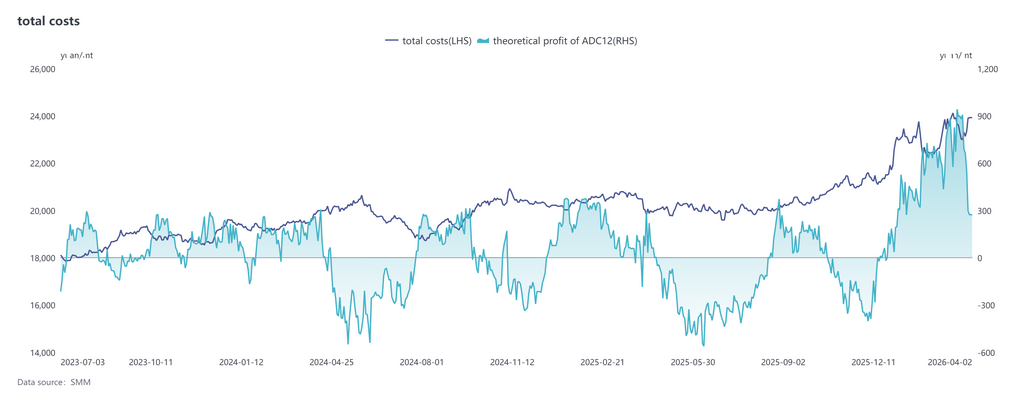

Cost side, according to the latest SMM data, the theoretical total cost of the ADC12 industry rose to 23,560 yuan/mt in March, up 4.7 percentage points MoM from February. By cost structure, aluminum scrap cost per mt rose to 21,344 yuan, with its share edging up to 90.6%, remaining the absolutely dominant cost component; affected by the lower center of copper prices, copper cost per mt pulled back to 826 yuan, with its share falling to 3.5%; silicon cost per mt also slipped slightly to 484 yuan, accounting for 2.1%. Overall, driven by higher aluminum prices and rising prices of compliant supply, aluminum scrap prices followed the gains quickly, further lifting its share in total costs. During the same period, the industry's theoretical ADC12 profit was about 694 yuan/mt, and the industry as a whole remained in the profitable range. Entering April, aluminum scrap will still be the core factor driving ADC12 cost fluctuations, and its price trend will closely track the primary aluminum market. At the same time, affected by constraints on compliant supply, industry costs are expected to likely remain elevated and move sideways in April.

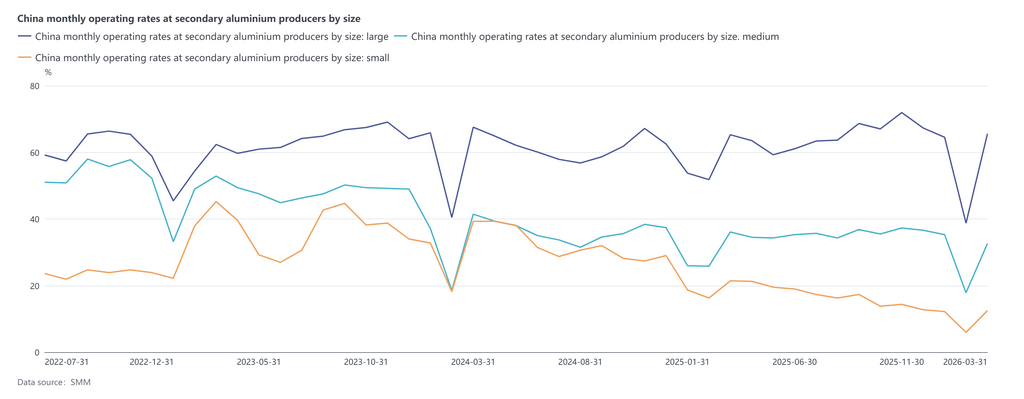

Supply side, the operating rate of the secondary aluminum alloy industry came in at 53.8% in March, rebounding sharply by 22.4 percentage points MoM and edging down by 1.3 percentage points YoY. After the Lantern Festival, enterprises generally resumed work and production, while the simultaneous recovery in downstream demand and the continued improvement in new orders significantly lifted the operating rate. However, the rebound was still constrained by multiple factors: cost pressure is expected to remain difficult to ease in the short term in April, the strength of the recovery in end-use demand remains uncertain, industry orders are expected to weaken somewhat, and the operating rate will likely pull back slightly from March while remaining broadly stable.

Demand side, although downstream enterprises gradually resumed work and production in March, order recovery in end-use sectors such as automobiles fell short of expectations, and the traditional peak-season effect of "Golden March" failed to fully materialize. Downstream profit margins were already limited, leaving buyers highly sensitive to raw material prices. Acceptance of high-priced ADC12 declined markedly, price transmission remained sluggish, and negative market feedback gradually emerged—transactions failed to keep pace during the price upswing, while restocking willingness also remained cautious during the price pullback, with overall procurement mainly focused on small-lot purchases for immediate needs. In addition, some die-casting enterprises reliant on the Middle East market saw export orders decline due to hindered transportation, further weighing on demand performance. Overall, demand in March was weaker than in the same period last year, market wait-and-see sentiment was relatively strong, and prices lacked effective support.

Entering April, recovery on the consumption side remained slow, downstream profits stayed under pressure, and although just-in-time procurement continued, the suppressive effect of high prices gradually emerged. Some enterprises may respond by cutting production, and overall demand is expected to be generally stable with slight fall. On the supply side, some small and medium-sized enterprises suspended production temporarily at the beginning of the month, and the operating rate dropped back slightly, leaving limited short-term incremental supply. Overall, the market’s primary contradiction has shifted to insufficient consumption momentum, with a lack of upward impetus, making it difficult for prices to sustain the uptrend. Going forward, attention should focus on the recovery of actual post-holiday orders, aluminum price trends, and changes in macro sentiment: if demand remains weak, the price center is expected to edge lower slightly; if downstream demand improves at the margin or aluminum prices strengthen, prices are likely to receive temporary support.