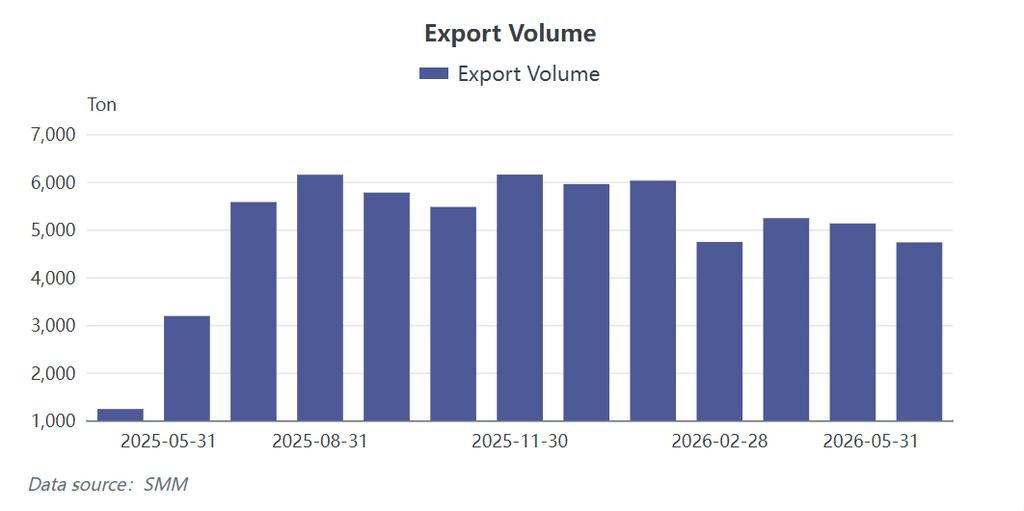

【Data Overview】

According to SMM statistics, China’s exports of NdFeB magnets totaled 4,730 tons in May 2026, marking a month-on-month decline of 7.72%. However, volumes surged by 281.84% year-on-year. The sharp YoY increase is primarily attributed to a low base effect caused by export controls in May 2025. The MoM drop, meanwhile, reflects both seasonal weakness in overseas demand and tangible changes in domestic export licensing procedures.

【May Data Breakdown: Falling Demand Meets Slower Clearance】

The pullback in May exports was driven by two main factors.

First, the market entered a typical seasonal lull. As Europe is a major destination for Chinese NdFeB exports, demand from downstream sectors—particularly automotive and industrial motor manufacturers—usually slows down ahead of the summer shutdown period. This led to a reduction in new procurement orders from European buyers.

More critically, clearance processes at ports became less efficient. Although high-level Sino-U.S. meetings in May signaled a constructive tone, regulatory scrutiny over products containing heavy rare earths—such as dysprosium and terbium—has not eased in practice. License issuance for these magnet grades by the Ministry of Commerce has lengthened noticeably. Some shipments originally scheduled for May departure were held at port pending final approval, resulting in lower reported export volumes compared to factory production schedules. Additionally, the release of inventories that had been stockpiled at ports during last year’s control measures contributed to the distorted YoY comparison.

【June Outlook: Escalating Frictions Further Constrain Approvals】

Entering June, export pressures have intensified amid renewed trade frictions between China and the U.S. Based on SMM’s surveys of major magnet producers, export volumes are expected to decline further and are unlikely to reach the previously forecast level of 5,500 tons.

This expectation is largely due to a marked slowdown in the approval process. Recent updates to U.S. military procurement lists and related export restrictions have prompted a cautious response from Chinese authorities regarding strategic material exports. Industry feedback indicates that applications for export licenses covering heavy rare earth-containing magnets now face longer review cycles and greater uncertainty. While overseas inquiries have increased—partly driven by concerns over future supply security—the actual ratio of inquiries converting into approved shipments remains low.

Supply chain adjustments are also influencing the data. Due to ongoing uncertainties surrounding raw material availability, some overseas processors are revising their procurement strategies, either by reducing inventory levels or exploring capacity shifts to regions such as Southeast Asia. These localized adjustments are reflected in the declining export figures for certain feedstocks and semi-finished magnetic products.

【Market Feedback and Corporate Response】

Feedback from manufacturers highlights growing challenges related to delivery lead times. Approval processes that previously took two weeks may now extend beyond a month. This not only increases working capital requirements but also makes companies more cautious when committing to long-term orders.

Notably, while exports of raw material-intensive products are softening, shipments of downstream finished goods—such as motors and automotive components—have remained relatively stable. This suggests global supply chains are adapting by increasing inventory buffers at the finished-goods level to hedge against upstream volatility.

【Outlook】

In the near term, reported NdFeB export volumes are likely to remain under pressure. Market participants should focus less on the volume of overseas inquiries and more closely monitor the actual pace of export license approvals, which has become the primary bottleneck. Companies are advised to enhance communication with relevant authorities, ensure thorough documentation for material traceability, and adjust production and logistics planning to accommodate extended approval timelines.

![Energy Fuels' Acquisition of VAC and US International Mature Rare Earth Asset Acquisition Landscape [SMM Analysis]](https://imgqn.smm.cn/usercenter/ecUwF20251217171745.jpg)

![This week, rare earth prices outside China remained stable, while the US continued to acquire mature rare earth enterprises outside China [SMM Rare Earth Ex-China Weekly Review].](https://imgqn.smm.cn/usercenter/OJvHl20251217171744.jpeg)