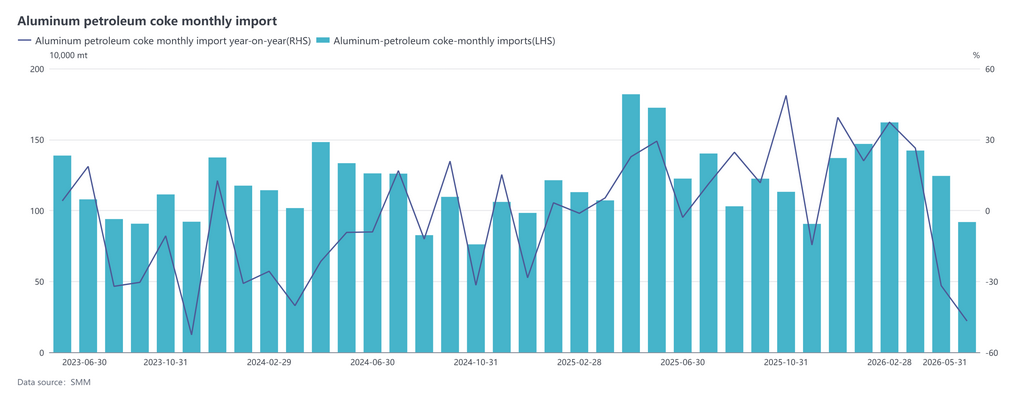

SMM, June 24:

Customs statistics showed that China’s total petroleum coke imports in May 2026 were 918,600 mt, down 26.10% MoM and down 46.84% YoY. The average import price for the month was $323.26/mt, up 32.13% MoM and up 62.96% YoY, presenting a typical pattern of contracting volumes and rising prices. In January-May, cumulative imports of petroleum coke were 6.6708 million mt, down 5.65% YoY.

By source, import origins were highly concentrated in May, with the US, Russia, and Oman as the top three suppliers, corresponding to import volumes of 305,000 mt, 118,700 mt, and 88,400 mt, accounting for 33%, 13%, and 9% of total imports for the month, respectively. On the price front, differentiation by country was pronounced. Canada, Oman, and the US led the price increases—Canada’s month-on-month price was up $270.15/mt, while both Oman and the US saw increases exceeding $100/mt. Kazakhstan, the UK, and Saudi Arabia also posted moderate price gains, collectively lifting the average import price. Only imports from Indonesia, Brazil, and Argentina saw price declines; Indonesia’s price drop exceeded $120/mt, but the overall pullback was limited and insufficient to offset the cost increases from price rises in multiple supplying countries. Tightening supply from overseas smelters, coupled with higher ocean logistics costs, was the primary driver of the sharp increase in the average CIF price this month.

By product category, the proportion of uncalcined petroleum coke imports this year was roughly 26% low-sulphur coke (sulphur <3%) and 74% medium-to-high-sulphur coke. In the first five months, cumulative imports of low-sulphur uncalcined coke were 1.748 million mt, up 26.60% YoY; imports of other uncalcined coke were 4.9227 million mt, up 24.26% YoY.

In summary, the combined impact of concentrated maintenance and production cuts at overseas smelters and persistently rising ocean freight rates significantly tightened available overseas coke supply, sharply raising traders’ external purchase costs and prompting Chinese buyers to actively slow their purchasing pace. This directly resulted in a sharp pullback in May port arrivals and a simultaneous surge in prices. Currently, the maintenance cycle at major overseas producing regions has yet to conclude, making it difficult to reverse the strong overseas spot market in the short term, so China’s import costs are likely to remain high. SMM expects port arrivals of petroleum coke in June to recover slightly but unlikely to return to previous high levels. According to SMM surveys, although prices from Brazil and Argentina have pulled back slightly, overall price levels remain high. Going forward, the import market will continue to feature diversified sources and persistent differentiation in price spreads by country and product category.

![[SMM Aluminum Flash News] GeT Alloys Replaces Heavy Fuel Oil with Tyre-Derived Fuel in Aluminium Recycling](https://imgqn.smm.cn/usercenter/tYQzs20251217171653.jpg)

![[SMM Aluminum Flash News] Woodside Signs Gas Supply Agreement with Alcoa to Support Alumina Production](https://imgqn.smm.cn/usercenter/EVjRH20251217171653.jpg)

![[SMM Aluminum Flash News] Fosbel Promotes Ceramic Welding Technology for Online Aluminium Furnace Repairs](https://imgqn.smm.cn/usercenter/VTjoW20251217171653.jpg)