Indonesian state-owned steel giant PT Krakatau Steel (Persero) Tbk (IDX: KRAS, hereinafter referred to as "Krakatau") released its 2025 consolidated financial statements on March 31, 2026. On the surface, the company recorded a net profit of 339.6 million USD (approximately 5.68 trillion IDR), its best performance since 2019. However, unpacking the core steel business reveals that the steel segment's operating loss in 2025 actually widened from 40.79 million USD in 2024 to 102.5 million USD. Despite the HSM #1 hot strip mill resuming production after years of stoppage due to a fire—driving a 29% year-on-year increase in steel sales volume to 944,562 tonnes—the blended Average Selling Price (ASP) per ton plummeted by about 30% during the same period. The gross profit per ton flipped from +100 USD/tonne to -32USD/tonne, and the consolidated rolling capacity utilization rate remained at only about 22.5%.

Overall Financial Portrait: Core Steel Business Drags Down Overall Performance

Consolidated revenue in 2025 was 959.8 million USD, largely flat compared to 954.6 million USD in 2024. Gross profit dropped from 106.9 million USD to 50.74 million USD, and the gross margin fell from 11.2% to 5.3%. Operating profit swung from a profit of 26.69 million USD in 2024 to a loss of 82.71 million USD. The "turnaround to profit" with a book net profit of 339.6 million USD primarily stemmed from a one-off accounting gain related to loan restructuring (see Note 38, pages 98 and 126 of the financial report). Excluding this, the normalized figure remains a loss of approximately 246.6 million USD, expanding 66% compared to the normalized loss of 148.4 million USD in 2024.

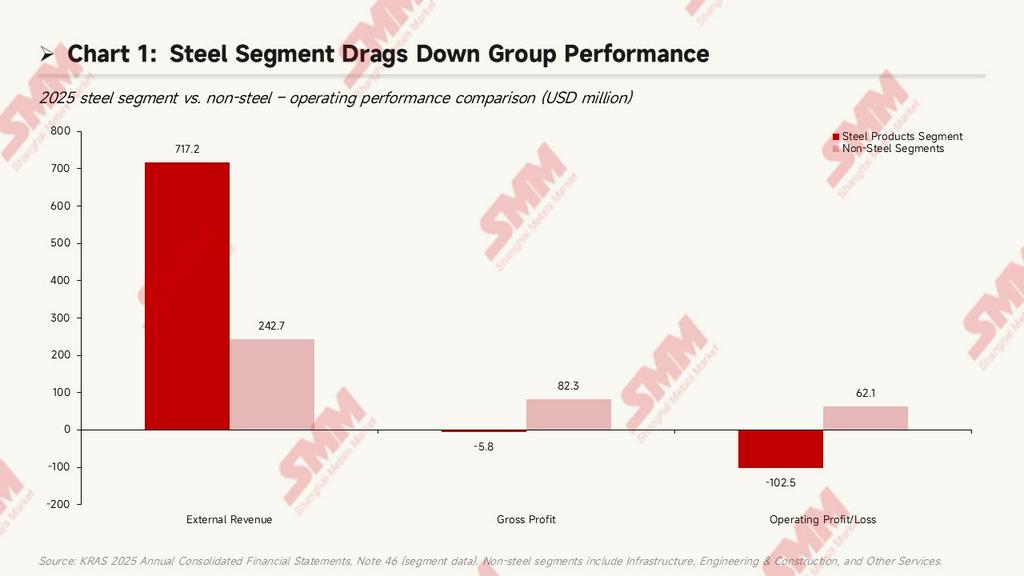

According to segment data in Note 46, external revenue from the steel products segment was 717.2 million USD, accounting for about 74.7% of consolidated external revenue. However, the segment's gross profit swung from a profit of 47.48 million USD in 2024 to a loss of 5.76 million USD, and the segment's operating loss expanded from 40.79 million USD in 2024 to 102.5 million USD in 2025—an increase in loss size of about 2.5 times. During the same period, the infrastructure segment (including ports, real estate, power, and water) recorded an operating profit of 51.24 million USD, serving as the group's sole profit pillar. The engineering, construction, and other services segments contributed a combined operating profit of approximately 10.82 million USD. The conclusion is clear: Krakatau is listed as a "steel company," but its actual profits in 2025 were entirely supported by non-steel businesses.

Steel Core Business Operations Level

Group Structure and Subsidiary Division of Labor

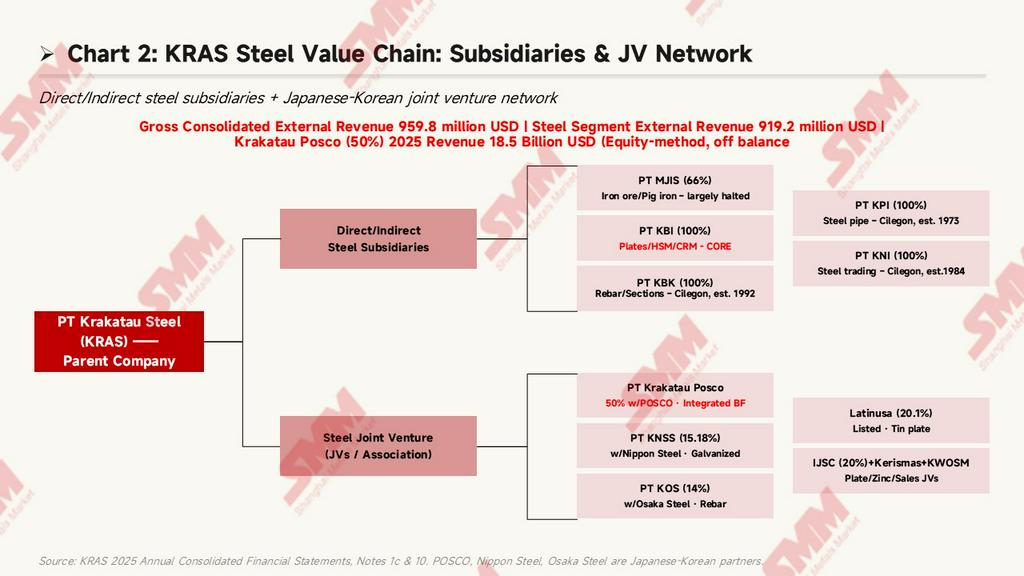

Krakatau's headquarters and core production base are located in Cilegon, Banten Province, Indonesia, having commenced commercial operations in 1971. The group adopts a parent + multi-tier subsidiary architecture. The steel industry chain involves five directly held steel subsidiaries, several indirectly held subsidiaries, and a number of Japanese and Korean joint ventures (for details, see Note 1c and Note 10, pages 15–17, 20, and the subsidiary summary table on page 91).

Several core operating entities in the steel business:

- PT Krakatau Baja Industri (KBI, 100%): A newly established steel subsidiary in 2023, responsible for producing flat products such as hot-rolled and cold-rolled coils. It is the core operating platform that the company announced will operate "independently" in 2026. Ending assets: 50.8 million USD.

- PT Krakatau Baja Konstruksi (KBK, 100%): Operating in Cilegon since 1992, producing rebar and profiles, and selling through its subsidiary PT Krakatau Wajatama Osaka Steel Marketing (KWOSM, 67% owned by KBK). Ending assets: 188.6 million USD.

- PT Krakatau Pipe Industries (KPI, 100%): A steel pipe plant operating since 1973. Ending assets: 148.2 million USD.

- PT Meratus Jaya Iron & Steel (MJIS, 66%): An iron ore smelting subsidiary operating in Jakarta since 2012. Ending assets are only 260,000 USD, and it is basically suspended—its plant assets have been fully impaired (see below).

- PT Krakatau Niaga Indonesia (KNI, 100%): A steel trading subsidiary operating since 1984. Ending assets: 43.86 million USD.

The group also has numerous non-steel subsidiaries supporting its profits: PT Krakatau Sarana Infrastruktur (KSI, 100%, real estate and hotels, ending assets 615.1 million USD, the largest in the group), PT Krakatau Bandar Samudera (KBS, 100%, port services, ending assets 198.0 million USD), PT Krakatau Tirta Industri (KTI, 51%, water), among others.

Steel Joint Venture Network

Beyond consolidated subsidiaries, Krakatau holds stakes in multiple steel joint ventures via the equity method, with a combined book investment value of approximately 401.9 million USD (Note 10, page 91):

- PT Krakatau Posco (KP, 50%): Indonesia's only integrated blast furnace steel plant, held 50/50 by Krakatau and South Korea's POSCO. In 2025, its 100%-basis revenue was 1.8477 billion USD (about 2.7 times the revenue of KRAS's steel segment), but it recorded a net loss of 39.8 millionUSD. Krakatau's book investment value in KP dropped from 274.5 million USD at the end of 2024 to 260.9 million USD at the end of 2025. KP is the main supplier of steel billets (slabs) to Krakatau's HSM plant.

- PT Krakatau Nippon Steel Synergy (KNSS, 15.18%): A partnership with Nippon Steel, producing galvanized and annealed sheets.

- PT Krakatau Osaka Steel (KOS, 14%): A partnership with Japan's Osaka Steel, producing rebar and profiles.

- Latinusa (20.10%): A listed company and tinplate producer.

- PT Indo Japan Steel Center (IJSC, 20%): Steel plate and coil processing.

- PT Kerismas Witikco Makmur (29.31%): Zinc product production.

The group's combined share of profits and losses from joint ventures was a loss of 9.34 million USD, narrowing from a 49.68 million USD loss in 2024, largely driven by the shrinking loss at KP (which narrowed from a net loss of 124.6 million USD in 2024 to 39.8 million USD in 2025).

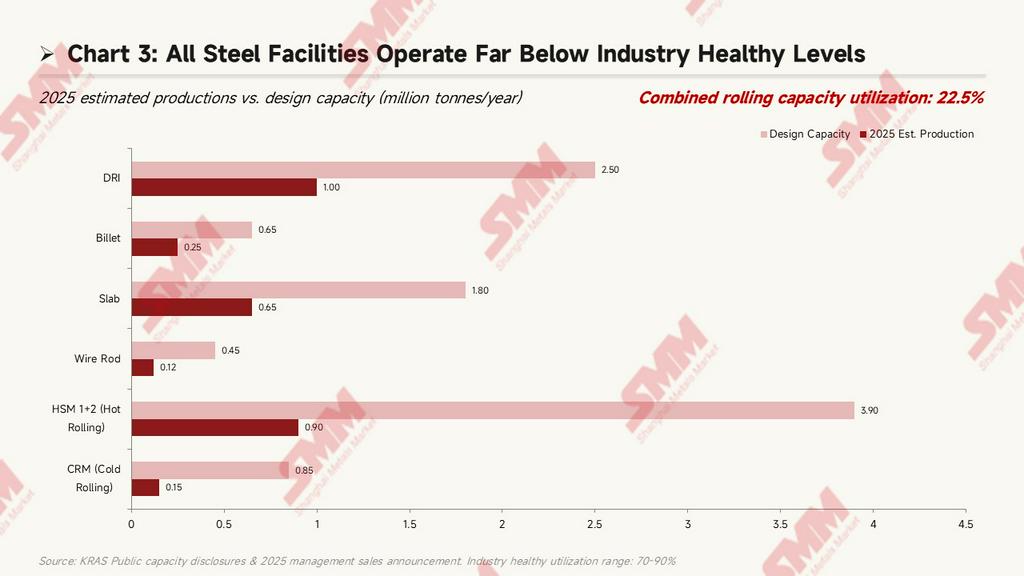

Capacity and Utilization: Severe Underutilization Across Facilities

The Krakatau Group's consolidated rolling capacity is approximately 5.2 million tonnes/year, covering the complete process from direct reduced iron (DRI) -> billet -> hot rolled/cold rolled/wire rod (capacity data sourced from management's public disclosures and the Q1 production and sales announcement on March 31, 2026):

Estimated 2025 capacity utilization rates for each facility:

-

DRI (Sponge Iron): Design capacity 2.5 million tonnes/year, 2025 output approx. 1 million tonnes, utilization 40.0%.

- Slab: Design capacity 1.8 million tonnes/year, output approx. 650,000 tonnes, utilization 36.1%.

- Billet: Design capacity 650,000 tonnes/year, output approx. 250,000 tonnes, utilization 38.5%.

- Hot Strip Mill 1+2 (HSM): Combined design capacity 3.9 million tonnes/year, output approx. 900,000 tonnes, utilization only 23.1%.

- Cold Rolling Mill (CRM): Design capacity 850,000 tonnes/year, output approx. 150,000 tonnes, utilization 17.6%—the lowest among all facilities.

- Wire Rod: Design capacity 450,000 tonnes/year, output approx. 120,000 tonnes, utilization 26.7%.

The consolidated total rolling capacity utilization rate was approximately 22.5%, far below the healthy level of 70-90% generally seen among Asian peers. Low utilization typically prevents fixed costs from being diluted by production volume, but the situation improved somewhat in 2025—HSM #1 had halted production for all of 2024 due to a fire, began Hot Commissioning in December 2024, and officially resumed production in Q1 2025. This is the crucial context behind the 29% year-on-year sales growth in 2025 (detailed in the next section); prior to the HSM #1 restart, the 2024 sales base was only about 730,000 tonnes.

Sales Volume Trends and Per-Ton Economics

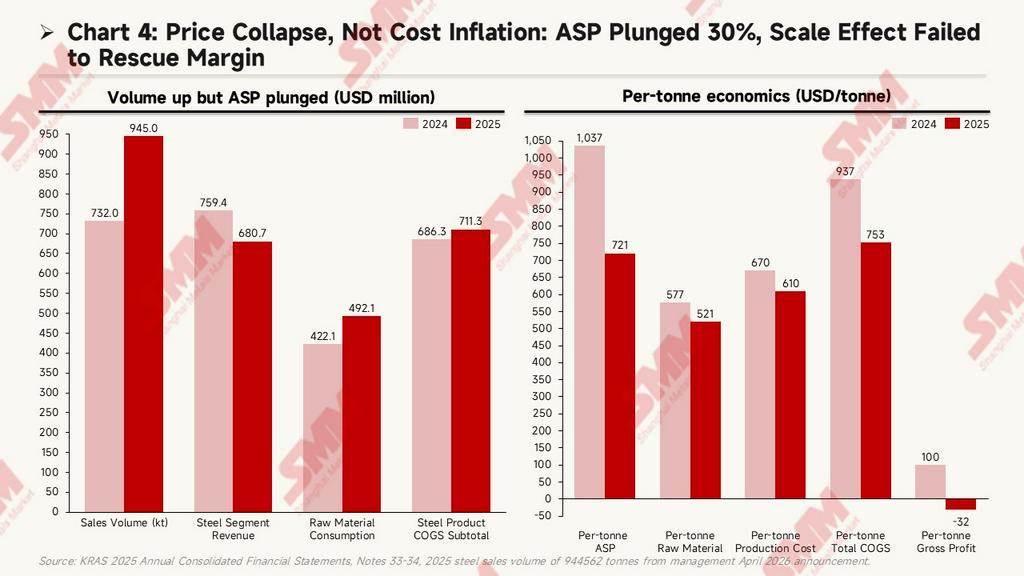

Krakatau's steel sales volume in 2025 was 944,562 tonnes (from management's April 2026 announcement), a 29.1% increase compared to approximately 732,000 tonnes in 2024. The primary driver was the resumption of production at the HSM #1 hot strip mill starting in December 2024 (previously halted due to fire). However, despite the massive surge in volume, the steel segment's gross profit still swung from positive to negative. The root cause was not cost inflation, but severe pressure on pricing:

Absolute Costs: Volume +29% but Revenue -10%

Steel segment sales volume grew from roughly 732,000 tonnes in 2024 to 945,000 tonnes in 2025 (+29.1%), but during the same period:

- Steel Segment Revenue: Dropped from 759.4 million USD to 680.7 million USD, an inverse decline of 10.4%. A significant increase in volume coupled with declining revenue implies a sharp drop in the underlying Average Selling Price (ASP) per ton.

- Raw Material Consumption: Increased from 422.1 million USD to 492.1 million USD, an absolute rise of 16.6%. This is much milder than the 29% volume growth, indicating that the raw material cost per ton actually decreased.

- Steel Products COGS Subtotal: Rose slightly from 686.3 million USD to 711.3 million USD, up only 3.6%. This further proves that inflation did not occur on the cost side; rather, costs were diluted by economies of scale.

The absolute value story is clear: Volume surged (HSM #1 restart), absolute costs rose moderately, but revenue fell instead—all the pressure came from the pricing side.

Per-Tonne Economics: ASP Plummets 30%, Per-Ton Cost Drops 20% Due to Scale Effects

The per-tonne metrics (USD/tonne) converted by sales volume trend in the exact opposite direction of what is seen on the surface:

- Average Selling Price (ASP) per tonne: Plummeted from 1037 USD/tonne to 721 USD/tonne, a 30.5% drop. This is the core contradiction.

- Raw Material Consumption per tonne: Fell from 577 USD/tonne to 521 USD/tonne, a 9.7% drop.

- Production Cost per tonne (including labor + other manufacturing overhead): Fell from 670 USD/tonne to 610 USD/tonne, a 9.0% drop.

- Comprehensive COGS per tonne: Plummeted from 937 USD/tonne to 753 USD/tonne, a 19.6% drop.

- Gross Profit per tonne: Dropped from 100 USD/tonne to -32 USD/tonne, swinging from profit to loss.

The sharp decline in per-tonne costs due to scale effects theoretically should have improved gross profit. However, the magnitude of the ASP drop (316 USD/tonne) far exceeded the drop in COGS (184 USD/tonne), causing the per-ton gross profit to flip from 100 USD/tonne to -32 USD/tonne.

Analysis of the 30% ASP Drop

The 30% crash in ASP stems from two compounding factors:

- Product Mix Downgrade (Structural Effect): During the HSM #1 shutdown in 2024, the steel pipe subsidiary KPI's sales hit a record high (+45% YoY, with management announcing 17,238 tonnes in December 2024 alone). High value-added steel pipes accounted for a larger proportion of revenue, pulling up the average ASP. When HSM #1 resumed in 2025, the proportion of flat steel (HRC/CRC) rebounded, structurally dragging down the average price.

- Market Price Pressure (Cyclical Effect): Chinese low-priced steel impacted the Indonesian market. In October 2025, Indonesian DPR member Adisatrya publicly stated that "cheap Chinese steel is flooding Indonesia at unreasonable prices." KRAS Chairman Akbar Djohan also repeatedly mentioned the pressure of competing with imported Chinese steel. Additionally, the Indonesian Rupiah depreciated by about 4-5% against the US dollar during the same period, further squeezing local-currency-denominated margin space.

Overall, the fundamental reason for the steel segment's gross margin swinging to a loss in 2025 was "price collapse," not "cost inflation." The volume boost from the HSM #1 restart should have been favorable, but it was offset by rapidly declining steel prices. This structural issue was not directly addressed in the "five plans" listed by management in Note 48—continuing to scale up volume cannot solve pricing pressure unless accompanied by policy protection, export expansion, or product mix upgrades (such as increasing the share of high value-added varieties like automotive sheets).

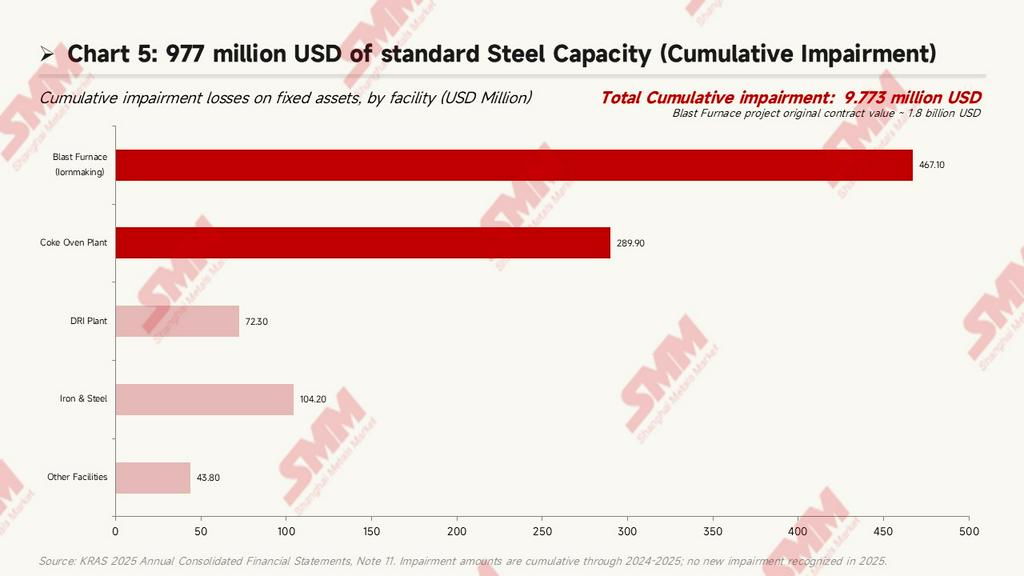

Stranded Assets: 977 Million USD in Impaired Steel Capacity

Note 11 discloses that Krakatau's accumulated fixed asset impairment losses have reached 977 million USD, entirely concentrated in upstream ironmaking/reduction facilities:

Specific breakdown:

- Blast Furnace Ironmaking: Accumulated impairment of 467.1 million USD, the largest single item. The original contract value for this project was approximately 1.8 billion USD, signed as an EPC contract with subsidiary PT Krakatau Engineering (KE), and is currently substantially abandoned.

- Coke Oven Gas: Accumulated impairment of 289.9 million USD.

- DRI Plant (Sponge Iron): Accumulated impairment of 72.31 million USD.

- Iron Ore Smelting: Accumulated impairment of 104.2 million USD; the relevant subsidiary is basically halted.

- Other Facilities: Accumulated impairment of 43.76 million USD.

This means Krakatau's upstream layout centered around "blast furnace integration" has largely failed. Coupled with the disclosure in Note 1b (pages 19–20), the company raised funds through a Limited Public Offering (PMHMETD I) in 2016, with about 66% originally intended for the construction of Hot Strip Mill 2 (HSM 2). However, approved by the Indonesian Ministry of State-Owned Enterprises (S-535/MBU/08/2019) in August 2019, the use of proceeds was altered to "working capital for purchasing steel billets (slabs) for the HSM plant." In other words, the new HSM 2 plant planned from the 2016 fundraising is still not operational 9 years later, and the raised funds have been diverted to working capital.

Massive Employee Reduction

The group's headcount dropped from 4,087 at the end of 2024 to 3,272 at the end of 2025—a reduction of 815 employees, or a 19.9% decrease (Note 1d, page 23). This aligns with the shareholder loan agreement (PPS) signed between the company and controlling shareholder PT Danantara Asset Management in December 2025, where PPS-2 was earmarked specifically for funding "Golden Handshake" and "Lump Sum Window" employee severance programs. A layoff of this magnitude is relatively rare in the history of Indonesian SOEs.

Changes in Product Mix and Customer Structure

According to the revenue breakdown in Note 33 (pages 124–126), local sales of steel products dropped from 759.3 million USD in 2024 to 632.3 million USD (a 16.7% drop), while export sales simultaneously surged from 97,000 USD to 48.36 million USD. Although the base is small, it reflects management's attempts to explore export markets amid contracting domestic demand. By customer type, revenue from related parties dropped from 102.9 million USD to 30.57 million USD (a 70.3% drop), and revenue from government-related entities dropped from 72.13 million USD to 25.86 million USD (a 64.1% drop). Together, state procurement channels shrank by approximately 119.3 million USD. Third-party revenue increased from 779.6 millionUSD to 903.4 million USD (a 15.9% increase), with its share rising to 94.1%. Krakatau is increasingly being forced out from under the "state umbrella" and into more intense market-driven competition.

Future Steel Direction: Management's Public Plans

Note 48, "Going Concern" (page 148), explicitly points out that as of December 31, 2025, the group's accumulated losses reached 2.0105 billion USD, current liabilities exceeded current assets by 214.7 million USD, and operating cash flow remained a net outflow of 1.75 million USD, creating "material uncertainty regarding the going concern assumption." Management outlined five core response plans in this note, which are highly indicative of the future direction for the steel business:

-

Production Asset Optimization (rencana optimalisasi aset produksi): This implies operational revamps of core rolling facilities like HSM/CRM/wire rod mills, potentially involving production line consolidation and energy efficiency improvements, though specific projects and investment scales have not yet been disclosed.

- Efficiency Improvement: This includes operational measures such as lowering unit energy consumption, reducing downtime, and optimizing procurement.

- Business Cooperation with Strategic Partners (kerjasama bisnis dengan partner strategis): This is the most notable point. Combined with the "divestment of subsidiaries or joint ventures" clause attached to the Tranche B and Tranche C loans in MRA 2024, a "strategic partner" likely means bringing external investors into the core steel subsidiaries. Given that existing JV partners include top-tier Asian steelmakers like POSCO, Nippon Steel, and Osaka Steel, the possibility of introducing new strategic shareholders going forward is worth tracking.

- Collection of Overdue Receivables: Note 47 reveals that accounts receivable turnover days improved from 53 to 49 days, and inventory turnover days dropped from 104 to 86 days, but a large amount of historical receivables still exists.

- Maximize Sales: Considering the capacity utilization rate is only 22.5%, there is theoretically massive room for volume upside, but the prerequisite is a recovery in market demand or an expansion of market share.

It is worth noting that Chairman Akbar Djohan mentioned in the Extraordinary General Meeting announcement on December 23, 2025, that the company will "independently operate" the HSM and CRM facilities through PT Krakatau Baja Industri (KBI) in 2026. This implies that in the event of joint ventures terminating or adjusting, KBI will take on the direct operational responsibilities for the core rolling business. How this structural adjustment will align with the specific format of the "strategic partner" plan will be a major highlight to watch in the 2026 financial reports.

Conclusion: The Paradox of the Core Steel Business

Krakatau's 2025 financial report presents a clear paradox: The "best performance" of 340 million USD in book profit is built upon a foundation of deteriorating operations in its core steel business. The 29% YoY sales volume growth driven by the HSM #1 restart should have been a tailwind, but it was neutralized by a 30% collapse in per-ton ASP over the same period, causing the per-ton gross profit to flip from 100 USD/tonne to -32 USD/tonne, and widening the steel segment's operating loss by 2.5 times. Layered with a mere 22.5% capacity utilization rate, an almost 20% reduction in workforce, and 977 million USD in stranded upstream capacity, a one-off accounting gain masks the fundamental problems. The core contradiction of the steel business is not "cost inflation," but rather the "price collapse under the impact of imported Chinese steel." Among the "five plans" listed by management in Note 48, "production asset optimization" and "efficiency improvement" alone can hardly solve the pricing side of the equation. The highly substantive "introduction of strategic partners" may well be the critical path for the Indonesian state to find a new operational paradigm after 50 years of accumulation in the steel industry. The Q1 2026 financial report (expected to be released in late April) will serve as the first key milestone to test this narrative.

Data Sources: PT Krakatau Steel (Persero) Tbk 2025 Consolidated Financial Statements (As of December 31, 2025; Released March 31, 2026); Public Company Announcements; World Steel Association 2025 Annual Report.

Note: This report is based on the analysis of public financial documents; all figures are subject to financial report disclosures. This article does not constitute investment advice.

![[SMM HRC Daily Trading] Spot Cargo Trading Continued to Pull Back](https://imgqn.smm.cn/usercenter/CrEsY20251217171716.jpg)

![[SMM steel]FHS HRC OPEN MAY 08 2026:](https://imgqn.smm.cn/usercenter/VgxkU20251217171719.jpg)