SMM, July 14:

In H1 2026, the zinc calcine market was characterized by persistently tight raw material supply, gradually shrinking supply, and TCs that rose first and then pulled back.

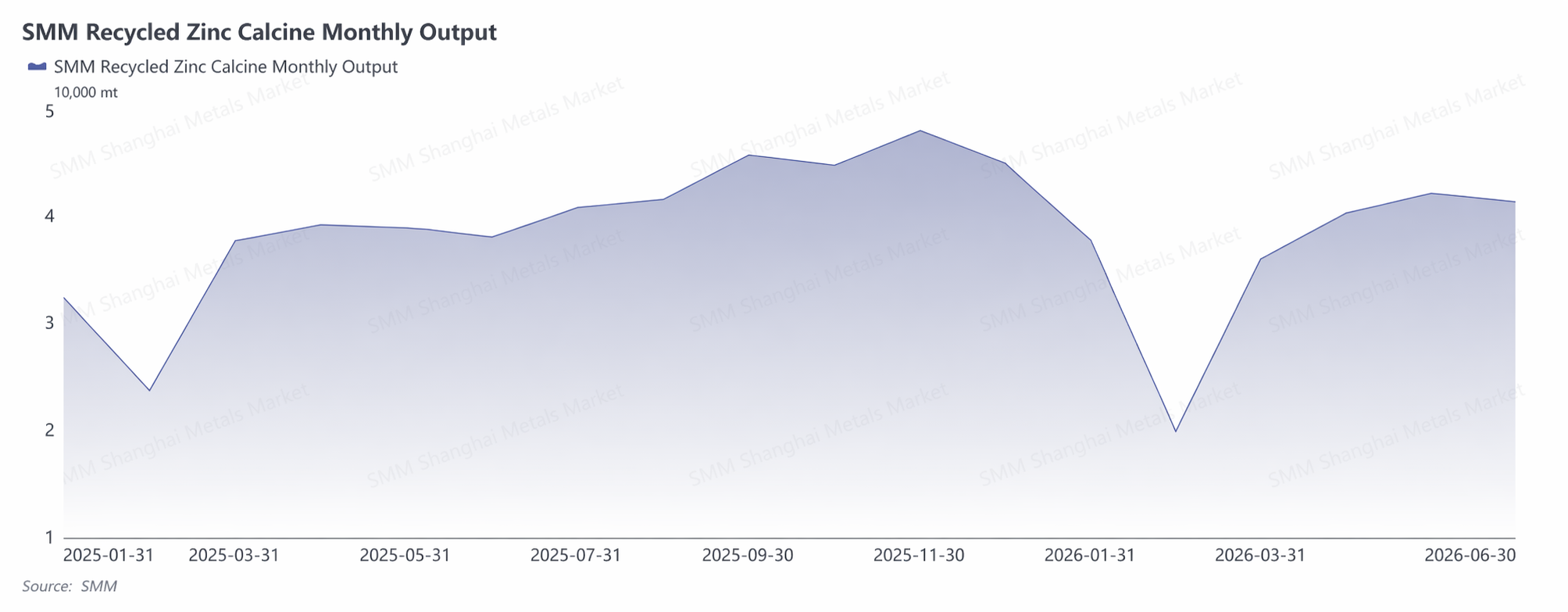

Production side, output fell first and then rose in Q1 due to the Chinese New Year holiday, with supply recovering notably in March-April as enterprises resumed production. From May to June, invoice issues reduced the circulation of recycled raw materials, and coupled with rising energy costs such as coal, enterprise profits remained under pressure and production schedule willingness declined. June production pulled back to 41,300 mt, tightening market supply again.

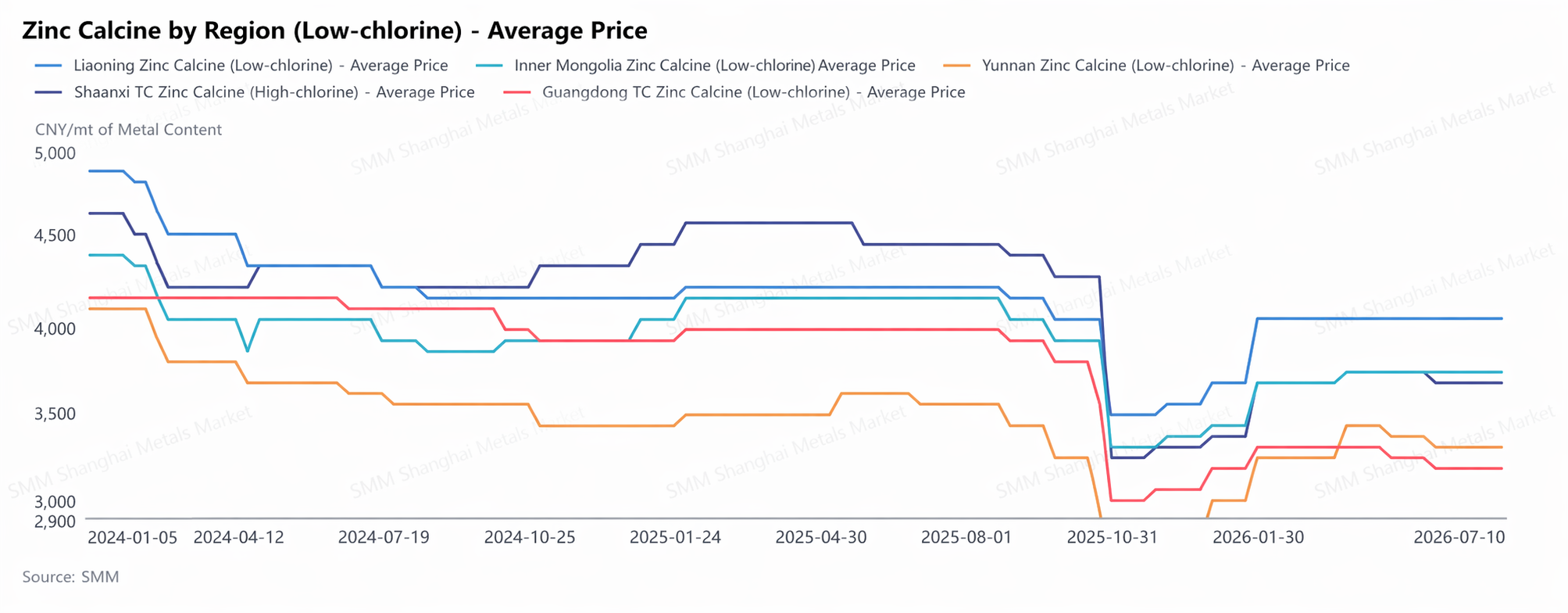

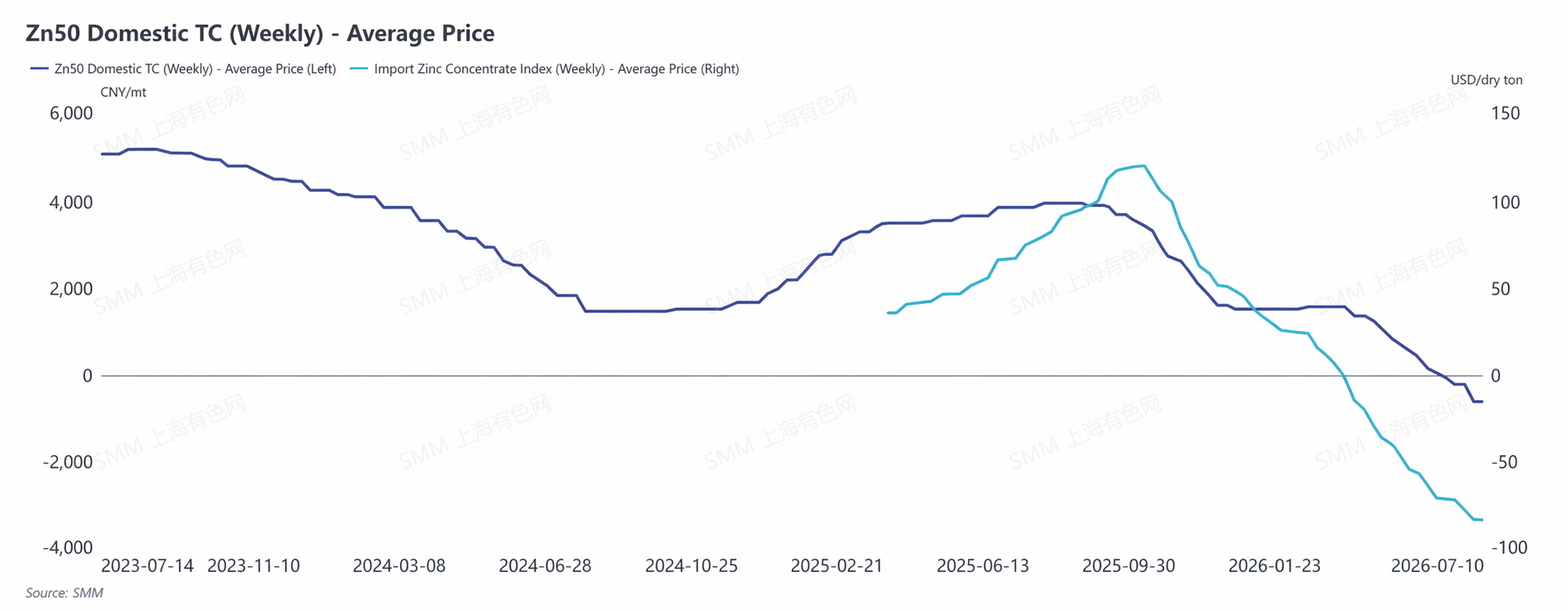

Price side, at the start of the year, demand weakened as secondary zinc enterprises halted production during the Chinese New Year, leading to a temporary rise in zinc calcine TCs. As downstream operations resumed in March-April, secondary zinc enterprises and some smelters restocked, boosting zinc calcine demand and TCs gradually stabilized. After May-June, invoice issues drove procurement costs higher, market liquidity decreased, and domestic zinc concentrate TCs remained persistently low. Some smelters increased zinc calcine purchases, supporting stronger zinc calcine prices and a slight decline in TCs. However, low profits and increased production cuts at secondary zinc enterprises limited further TC decline, capping the overall drop.

H2 outlook: the invoice issue is expected to remain difficult to resolve in the short term, and lower operating rates at steel mills will further tighten raw material supply. Zinc calcine enterprises will continue to face cost and profit pressures, and production schedule is expected to remain below the year-ago period.

Demand side, while the traditional consumption off-season will weaken demand from secondary zinc enterprises, domestic zinc concentrate TCs remain low, so some smelters still need to procure zinc calcine as supplemental raw material, providing some market support.

Overall, the tight raw material supply pattern is expected to persist in H2, zinc calcine prices should still have some support, and TCs are likely to edge down slightly. However, restricted by downstream enterprise profitability, room for further sharp drops is limited, and the market is expected to maintain a slow downtrend with sideways fluctuations.

(The above information is based on market data collection and comprehensive assessment by the SMM research team and is for reference only. This article does not constitute direct investment research advice. Clients should make cautious decisions and not replace independent judgment with this information. Any decisions made by clients are unrelated to SMM.)

![H1 2026 Zinc Calcine Review[SMM Analysis]](https://imgqn.smm.cn/usercenter/PEqzX20251217171755.jpg)

![Guangdong Zinc: Market Has Certain Wait-and-See Sentiment, Spot Premiums Consolidate at Lows [SMM Midday Review]](https://imgqn.smm.cn/usercenter/Txorc20251217171755.jpg)