I.AI Computing Power Expansion Opens Growth Space for Copper

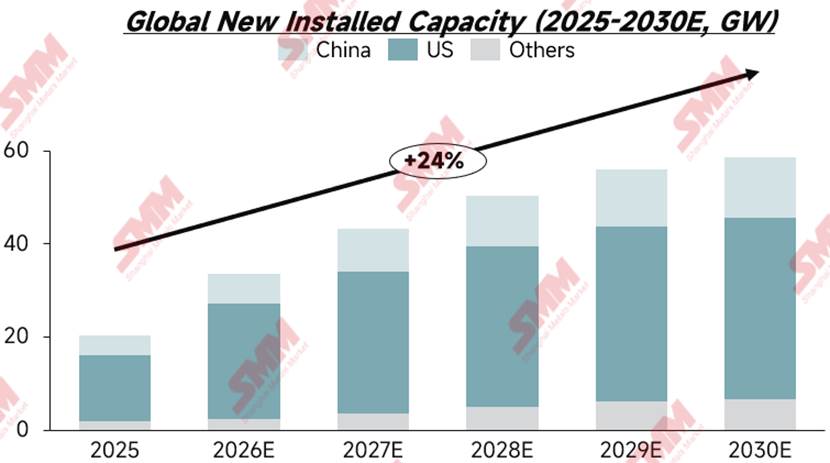

Global computing power infrastructure and data center construction have seen simultaneous explosive growth, with intensive commissioning of intelligent computing and supercomputing projects across regions, generating an entirely new incremental demand curve for copper semis. According to SMM projections, global new installations is expected to achieve a CAGR of 24% from 2025 to 2030, with the fastest pace of new deployment occurring in 2025 and 2026. New installations in 2026 are expected to grow 65% MoM, and by 2027, the growth rate of new installations is projected to pull back to 28.77%, followed by a year-by-year deceleration in 2028-2030.

By region, global new installations of computing power are mainly concentrated in two major markets: the US and China. Leveraging its scale-leading cloud operators, highly efficient facility operation systems, and a well-established global AI industry ecosystem, the US continues to lead in deployment scale. In China, leading cloud producers such as Alibaba and Tencent continue to increase capital expenditure on computing power infrastructure, while the national computing power network is formally incorporated into the top-level planning of the "Six Networks" and the "East Data, West Computing" projects are being rolled out and commissioned in batches, leading to a steady rise in the market share of domestic intelligent computing centers.

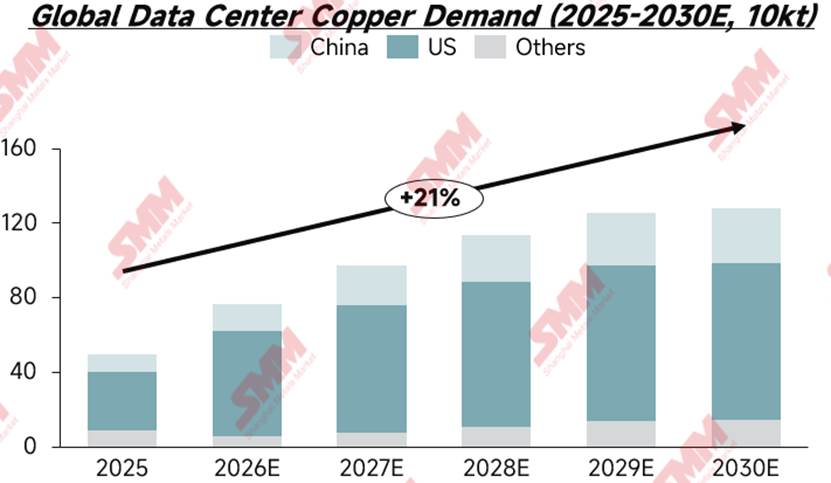

SMM analysis indicates that the CAGR of new copper consumption for global computing power from 2025 to 2030 is 21%, slightly lower than the growth rate of new installations. The core reason is the gradual release of medium and long-term technological effects that reduce copper usage. Looking at individual years, copper consumption growth is 54.94% in 2026, pulling back to 27.58% in 2027, and the growth of new copper consumption is also expected to exhibit a gradual slowdown trend from 2028 to 2030.

II. Unit Copper Consumption in Computing Power Centers Shows a Phased Trend of First Increasing then Decreasing

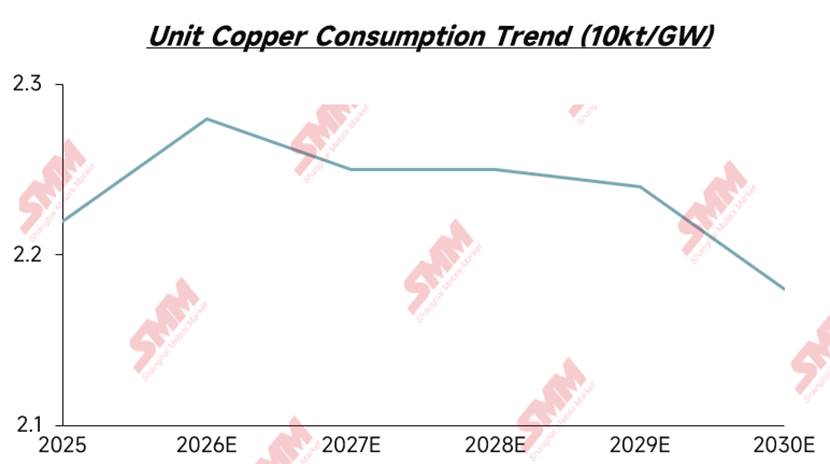

SMM's calculation by region shows that the comprehensive copper consumption per unit of global computing power centers will present a characteristic of first increasing then decreasing from 2025 to 2030. In the short term, new computing power is mainly through the construction of entirely new campuses, with supporting power, grounding, and other infrastructure built from scratch, coupled with high-density cabinets driving a rapid rise in the penetration rate of liquid cooling systems. Multiple factors jointly push comprehensive unit consumption upwards in 2025-2026. In the medium and long term, as 800V high-voltage DC power distribution is popularized at scale, the required thickness and cross-section of copper conductors under equivalent power scenarios will decrease significantly.Meanwhile, high-speed NVLink copper cables will face substitution by fiber optic interconnects. Coupled with the iteration of liquid cooling heat dissipation materials and technological breakthroughs in aluminum as a substitute for copper processes, the industry's comprehensive unit consumption will enter a downward trajectory. However, constrained by the pace of industrial technology penetration, SMM's calculations show no significant decline in unit consumption in 2027-2028, as consumption reduction and copper-increase factors offset each other, keeping unit consumption stable. The downward trend will only become significantly prominent after 2029. It is worth noting that comprehensive unit consumption is a weighted average calculated by SMM based on the deployment scale of computing power in the US, China, and the rest of the world. There is clear differentiation in unit consumption among data centers in different regions, with the unit copper consumption ranked as: Rest of the World > China > US, where the scale effect of large clusters effectively lowers unit copper intensity.

III. Breakdown of Core Copper Usage in Computing Power Centers

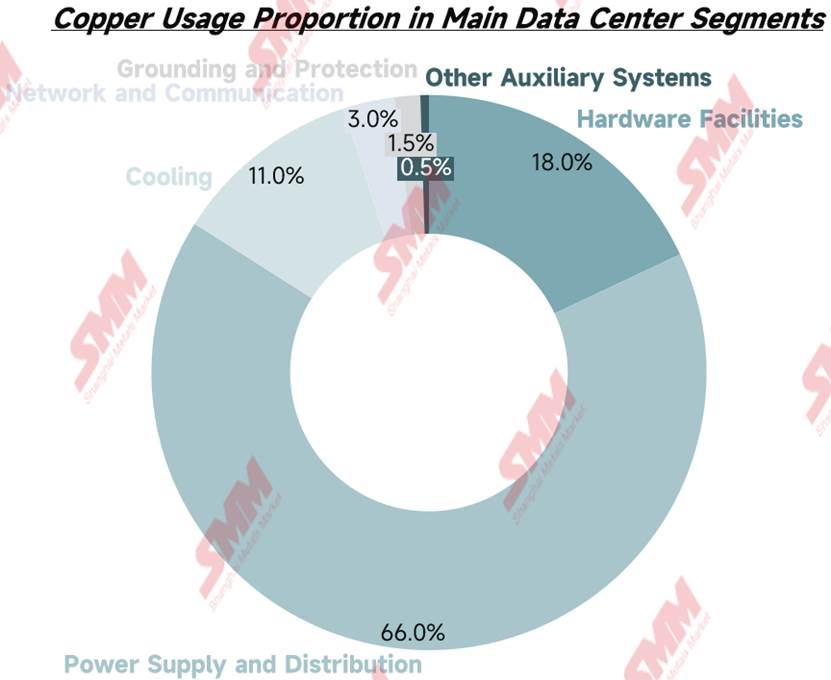

Computing centers fall into three categories: general-purpose IDCs, intelligent computing centers, and supercomputing centers. This article uses intelligent computing centers, which currently hold the highest market share and fastest growth rate, as the calculation sample to break down the copper consumption structure:

The power supply and distribution system is the largest copper-consuming segment in a computing center, accounting for 66% of total copper consumption according to SMM calculations. It primarily handles medium- and high-voltage power conversion and ensures uninterrupted power supply for equipment rooms. Medium- and low-voltage distribution cabinets, UPS, and busways are the core copper-consuming equipment. In the short term, high-power cabinets continue to boost demand for copper semis in power distribution, while in the medium and long term, after the popularization of lithium battery UPS and high-voltage DC solutions, unit copper consumption in the distribution segment will trend steadily downward.

SMM estimates that AI server hardware infrastructure accounts for 18% of copper consumption, undertaking all tasks of computing power, storage, and network interaction. It integrates core components such as GPUs, motherboards, and server power supplies, and the stable operation of the hardware directly determines the computing power output of the cluster. High-end AI server PCBs and internal interconnection copper wires are the main sources of copper consumption in this segment.

The liquid cooling system accounts for 11% of copper consumption. The closed-loop liquid cooling cycle meets the heat dissipation demands of high-power AI chips, with cold plates, CDU heat exchange units, and circulating copper pipe & tube serving as the main copper-consuming components. Liquid cooling penetration during 2025-2026 will boost demand for copper pipe & tube and copper plate/sheet and strip, and once copper-aluminum composite heat dissipation materials mature, the copper intensity for heat dissipation will gradually decline.

Network communication, grounding protection, and supporting auxiliary systems together occupy the remaining 5% of copper consumption, covering sub-scenarios such as high-speed interconnection cabling and equipment room grounding and lightning protection copper grids. The current optical fiber interconnection industry chain continues to expand production, with optical fiber enterprises seeing simultaneous improvements in orders and profitability, indirectly confirming the overall high prosperity of AI computing power construction. In the long term, optical fiber will also continue to divert demand from high-speed copper cables.

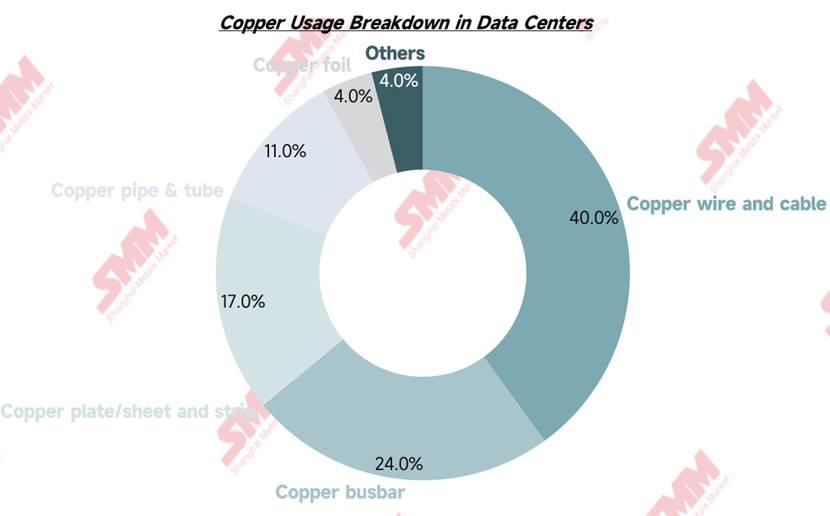

IV. Comprehensive Analysis of the Proportions of Different Copper Semis

Breaking down the copper consumption structure of computing centers comprehensively by semi-finished copper product category, cables and copper busbars are the core consumables throughout the construction process. SMM analysis shows that cables account for 40% of the total copper consumption in a computing center, acting as the “blood vessels” permeating every link, with core applications in high-voltage access, low-voltage distribution, power transmission, high-speed communication copper cables, building wiring, as well as grounding and lightning protection cables. Copper busbar (24% of total copper consumption), the "backbone" for high-current power distribution in data centers, is mainly used in high- and low-voltage power distribution cabinets, transformer copper busbars, UPS systems, etc.Copper plate/sheet and strip (17%) is mostly used in transformer windings and liquid cooling cold plate substrates, performing dual functions of power transformation and heat dissipation.

Copper pipe & tube (11% of total copper consumption) is a dedicated consumable for liquid cooling systems, mostly used in circulation piping, CDU heat exchange units, and precision air conditioning heat exchange pipes. The large-scale expansion of liquid cooling will boost demand for copper pipe & tube in the short term. Copper foil (4%) covers application scenarios including servers, switches, and various PCB circuit boards. Industry demand is concentrated on HVLP ultra-low profile high-end copper foil. Although the copper consumption per GW is relatively small, the incremental elasticity driven by AI computing power expansion is extremely strong. Currently, copper foil enterprises are accelerating the switch of capacity from ordinary electronic copper foil to high-end HVLP capacity, while copper clad laminate (CCL) producers have full order books and processing fees are being raised continuously, indicating that the prosperity of computing hardware demand has been verified across the entire industry chain.

In summary, the rapid expansion of computing centers directly drives the growth in demand for related copper semis. At the same time, high-density AI computing clusters significantly raise the requirements for power supply supporting facilities, and the overall electricity consumption scale of the industry surges simultaneously. The demand for power infrastructure construction derived from computing expansion has become a key focus for long-term tracking and research in the future.

While computing demand expands, the industry's development also faces external constraints. Currently, the grid connection approval process has a relatively long queuing period, and the market is generally concerned that transmission, distribution, and generation-side capacity bottlenecks may drag down the implementation pace of computing projects. However, according to SMM forecasts, no substantial power supply gap risk is expected for the industry over the next five years. It will still be necessary to closely track the approval progress and commissioning pace of various transmission and distribution supporting projects. SMM will also continue to follow the relevant industry dynamics and copper demand changes.

For detailed data, please contact Cynthia Wang of the SMM Copper Research Team at 15762822325.