[SMM Analysis] Overseas HRC prices Declined More Than Chinese Prices; Overall Procurement Demand Continued to Weaken

- Passive Contraction in China–Foreign HRC Price Spreads and Blocked Export Channels

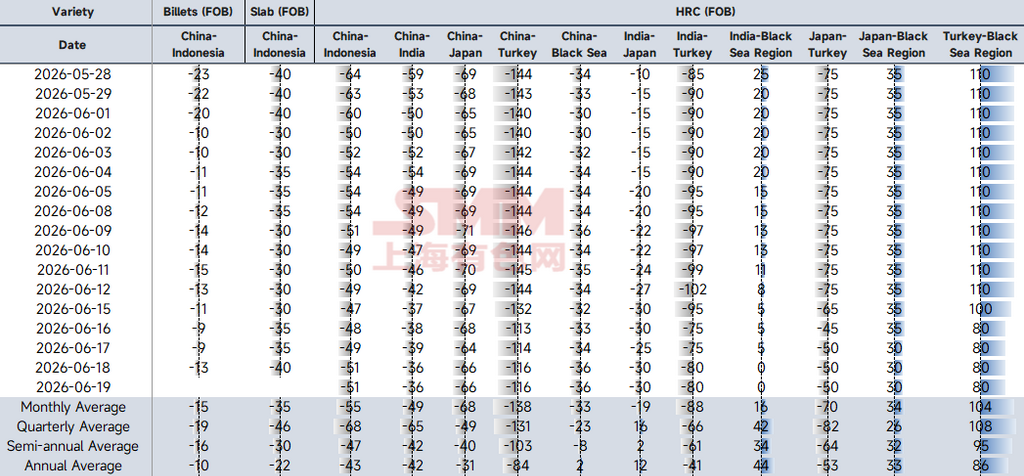

Price spread models showed entirely diverging trends. Steel billet price spreads were relatively stable, while HRC spreads continued to contract. The China–India HRC spread, after a streak of declines in mid-June, recently plunged to -36, an all-time low in the table. This figure was not only far above the quarterly average of -65, but also well below the current monthly average of -49. The root cause is not a sharp slide in Chinese export prices, but rather extremely weak Indian domestic demand. To defend their domestic market share and digest surplus production, local steel mills in India adopted a highly aggressive "defensive price-slashing" strategy. Meanwhile, given the domestic supply-demand pattern of strong supply and weak demand, there is still room for further downside in Indian domestic steel prices in the near term, and the China–India spread will hover at lows.

Data source: SMM

- Monsoon Rains Suppressed Downstream Demand; Indian Steel Market Was in the Doldrums

Weighed down by the traditional demand off-season due to the monsoon rainy season and generally very cautious purchasing attitudes among buyers, Indian long steel prices remained under pressure last week. Rebar EXW prices dropped notably to around $630/mt EXW, hitting the lowest level since May. In contrast, Raipur billet showed slightly more resilience, with prices edging up about $2/mt to around $453/mt EXW. This was mainly supported by a boost from earlier transactions and short-term support from buoyant sentiment in surrounding markets, though current spot procurement remained cautious and restrained. Notably, Chhattisgarh has planned to raise electricity prices, which is expected to push up the production cost of electric furnace billet by about $3–4/mt starting in July, providing some cost support. Overall, the Indian steel market will continue to face a mix of weak demand and cost support in the near term, and prices are expected to remain on a weak fluctuating trend.

- Off-Season Suppressed Rigid Demand and Shipping Disrupted: Southeast Asian Steel Market Stayed in the Doldrums Short-Term

Due to seasonal factors, construction activity rates in core Southeast Asian countries such as Vietnam, the Philippines, Indonesia, and Thailand have recently been low, directly limiting the release of rigid demand for long products like rebar and wire rod. Currently, major local mills' rebar EXW prices in Southeast Asia were generally weak, ranging between $520–535/mt EXW. Meanwhile, due to persistently subdued sentiment in end-user buying, destocking in the market remained relatively slow. Facing the current weak market, most buyers chose to wait and see, with purchasing strategies mostly centered on "purchasing as needed and buying just enough for immediate use." Additionally, stimulated by progress in US–Iran negotiations and news that the Strait of Hormuz may reopen, buyers in the Southeast Asian market grew more expectant of a pullback in ocean freight rates. Driven by the desire to "rush to buy amid continuous price rise and hold back amid price downturn," this expectation further amplified the market's bearish and wait-and-see sentiment. Still, the actual easing of shipping pressures stemming from geopolitical issues will take some time, and international freight rates are expected to remain mainly high and volatile in the short term.

- New Quotas Taking Effect on 1 July Prompted Full Buyer Wait-and-See; European HRC Trading Mediocre, Import Offers Weakened MoM

Last week, the overall European steel market was relatively mediocre, with sellers and buyers locked in deep standoffs ahead of the policy window period, and both spot and import markets were subdued: In Germany, mainstream transaction prices for HRC with August–September delivery remained at €680–700/mt EXW. In Italy, mainstream transaction prices for HRC with July–August delivery were at €670–680/mt EXW. Most European buyers generally chose to refrain from booking and are fully waiting for the new import quota system that will officially take effect on 1 July. End-users and traders are eager to assess the actual restrictive impact of the new policy on future import volumes in order to readjust their procurement strategies. At the same time, hit by a double blow from sluggish European domestic demand and uncertainty over the quota policy, steel import activity in Europe also dropped to a freezing point. At present, HRC offers for August shipment from Turkey and Asia to Europe have pulled back to €640–650/mt DDP. With a lack of buyer support, overseas mills' forward export offers showed clear signs of weakening on a MoM basis.

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![[SMM Iron & Steel] NMDC Awards $317 Million Contract to RVNL for 10 MTPA Iron Ore Blending Facility](https://imgqn.smm.cn/usercenter/ocJKj20251217171717.jpg)

![[SMM Iron & Steel] Nippon Steel Plans EAF Investment in Slovakia](https://imgqn.smm.cn/usercenter/NtHAJ20251217171719.jpg)