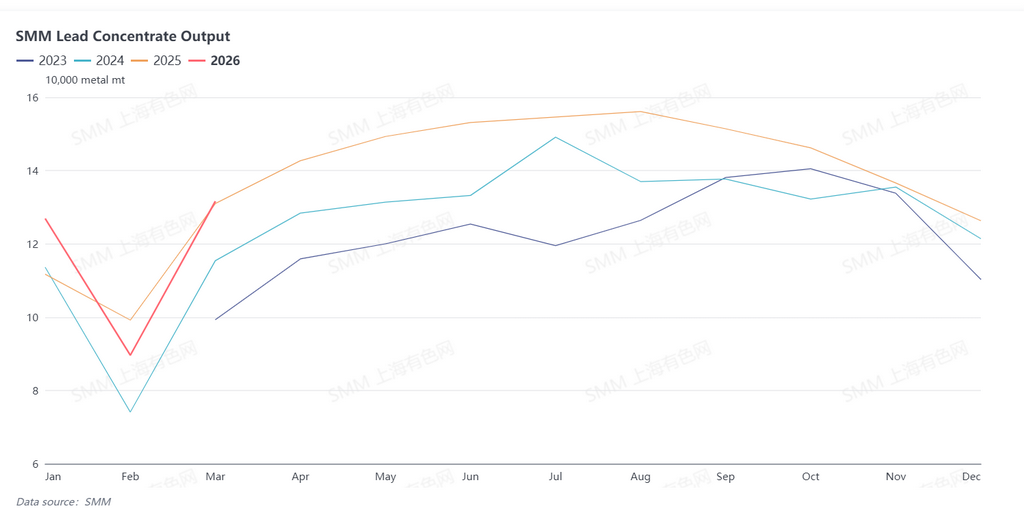

Supply Side: Seasonal Production Resumptions Advance, Marginal Increases Are Expected from March to April

According to SMM data, affected by the traditional winter break, production at lead-zinc mines in China’s colder regions declined starting in January. After the Chinese New Year holiday in February, mines gradually began preparations to resume production, but had not yet returned to full capacity. Lead concentrate supply in north China is expected to continue improving from March to April.

In terms of production, February lead concentrate production fell by about 37,300 mt in metal content MoM. In addition to fewer calendar days, mine shutdowns during the Chinese New Year holiday usually lasted 7-30 days. Mines that resumed production after the holiday gradually stabilized, forming the main source of incremental supply in March; some mines remained under winter break until late March and will not return to normal production until mid-April, while a few small and medium-sized mines are still waiting for operating permits from regulators.

SMM expects lead concentrate production in March to recover to about 130,000 mt in metal content, an increase of nearly 40,000 mt in metal content from February.

Market Side: Delayed Inventory Release, Diverging Procurement Strategies

In terms of transactions, due to unstable mine production in February, most enterprises temporarily delayed sales offers, and lead concentrate inventory generally did not enter the market until production stabilized in March. Although the tight supply pattern is unlikely to change in the short term, volatility in precious metal prices has intensified wait-and-see sentiment among smelters, and the earlier phenomenon of “panic buying” silver-bearing lead concentrates at the cost of suppressing TCs had already faded by early March.

Regional divergence has emerged: some small-scale smelters in Hunan, Yunnan, and other regions were concerned that weaker precious metal prices would leave by-product revenue insufficient to cover processing losses, and have cut primary lead production plans or extended maintenance cycles. Meanwhile, smelters’ tolerance for extremely low TCs has declined significantly, narrowing room for market negotiation.

Import and Price Outlook

In Q1 2026, China’s silver prices unusually generated import arbitrage, and expanding import profits for silver-bearing lead concentrates drove imports of lead concentrates and lead-bearing silver concentrates in January-February above the same period in previous years. As imported raw materials gradually arrived at plants, some producers postponed their demand for domestic spot procurement.

In terms of prices, silver prices have not yet fallen below the key support level of 20,000 yuan/kg, and the payable indicator for silver content in silver-lead ore has remained stable in the short term after multiple rounds of increases. If silver prices weaken sharply and remain weak, the payable indicator for silver content may edge down slightly, and lead concentrate TC quotes may rebound as demand for precious metals weakens.

![On the Eve of Delivery, Pressure From Rising China Refined Lead Inventory Remained Undiminished, and Lead Prices Continued to Be in the Doldrums [SMM Lead Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/riosq20251217171722.jpg)

![Overnight Lead Futures Consolidated, LME Lead Fell First and Then Rose While SHFE Lead Closed Slightly Lower [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/hrxHx20251217171721.jpeg)

![SMM March 10 EV Battery Market Overview [SMM Evening News]](https://imgqn.smm.cn/usercenter/ojSqv20251217171720.jpeg)