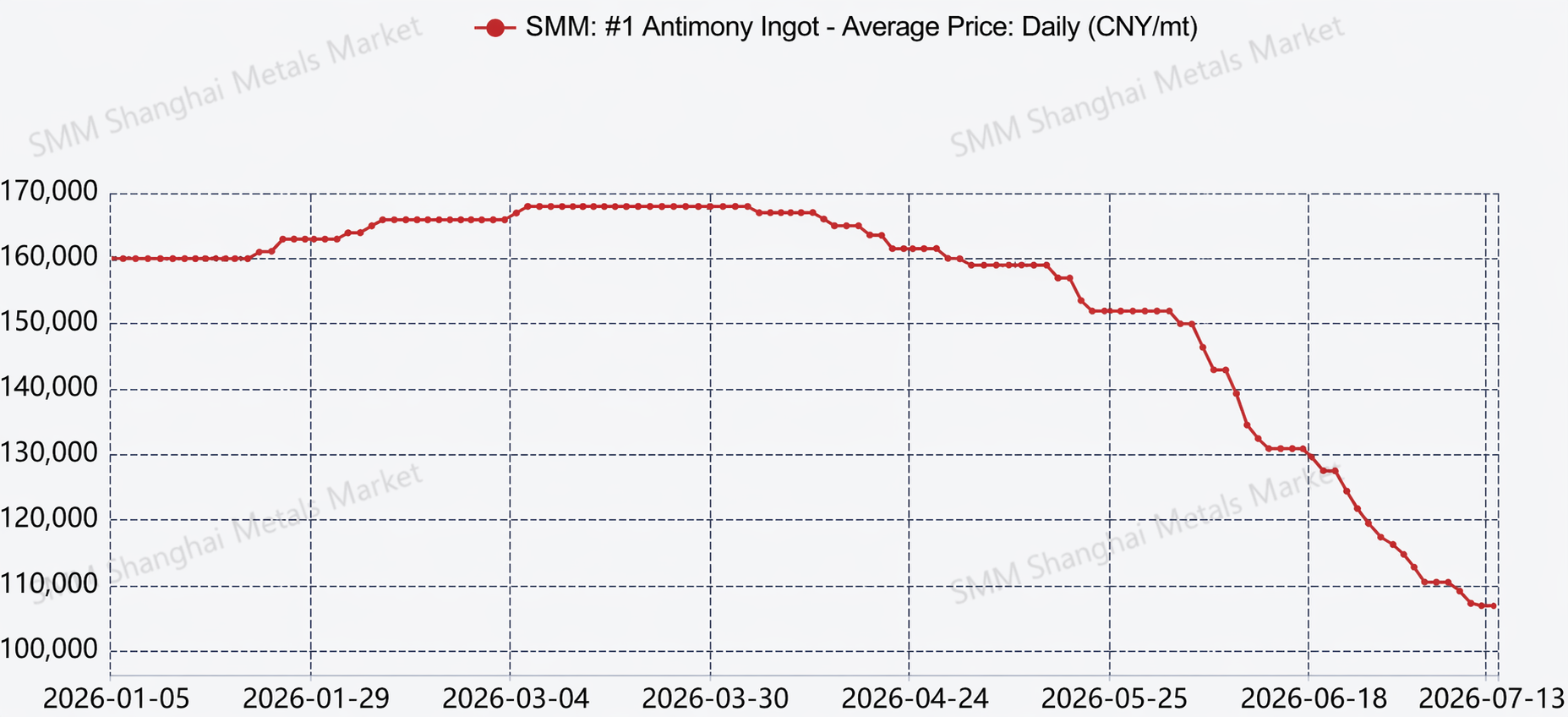

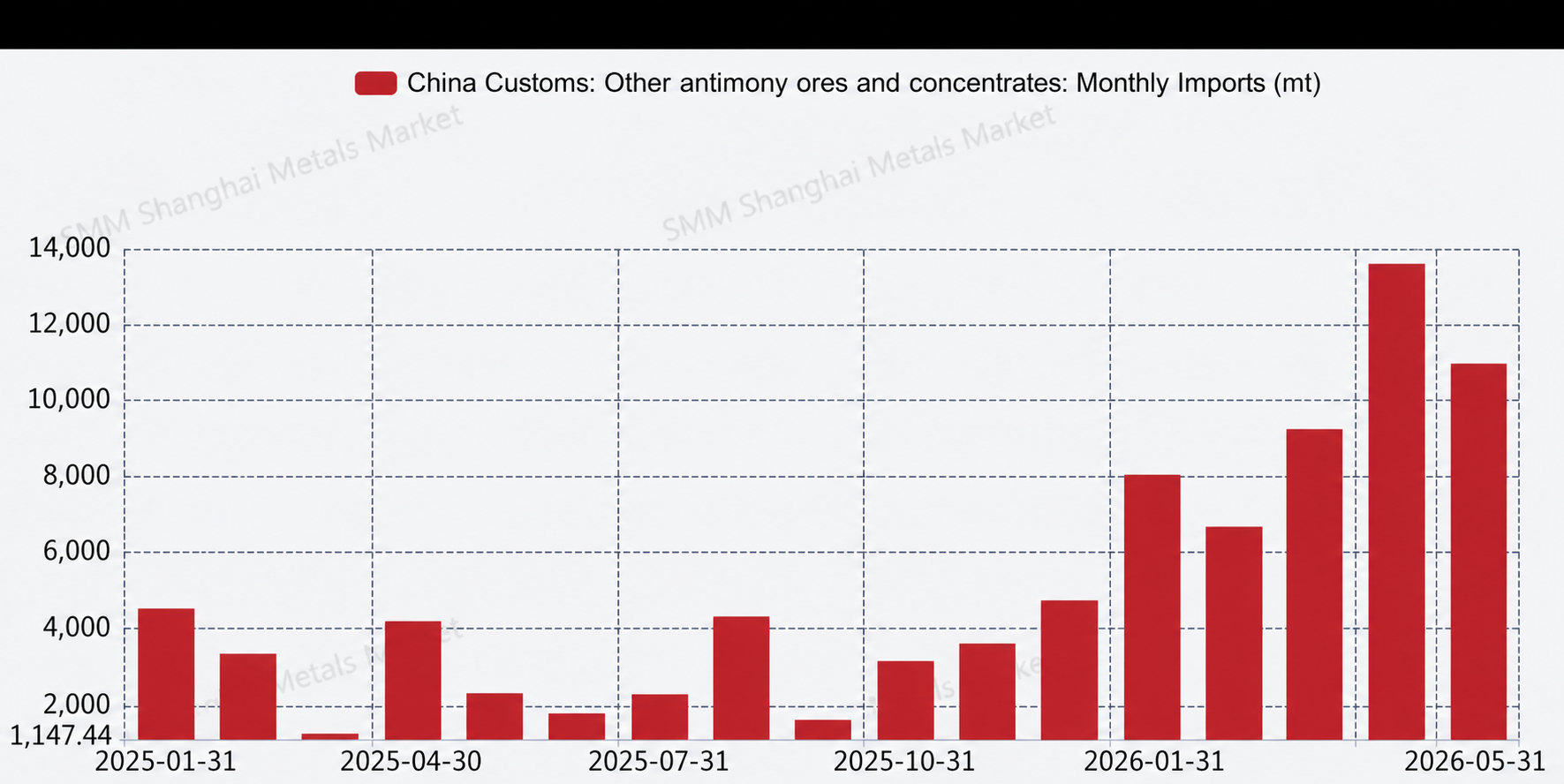

In H1 2026, the antimony market was generally weak and underwent a sustained sharp decline. During H1, cumulative antimony production from January to June was slightly lower than the same period last year, down around 8% YoY; however, imports of other antimony ores and concentrates from January to May amounted to about 48,658 mt, surging 209% YoY. A large volume of antimony raw materials entered China, which will gradually be converted into production supply in the coming period, and as a result, it is expected that the likelihood of higher domestic production in the months ahead may be amplified. Taking domestic #1 antimony ingot as an example, the average spot price is currently about 110,000 yuan/mt, a steep drop of roughly 50,000 yuan/mt from the spot price at the beginning of the year.

Supply side, production has not changed much, mainly because the industry's operating rate situation has not shifted significantly. Some enterprises facing tight antimony resources have continued to maintain low operating rates or remain shut down. Over the past six months, as prices kept trending lower, the risk of buying high-priced raw materials and selling products at low prices may arise, further reducing these producers' appetite for buying antimony raw materials and making it difficult for operating rates to improve. Demand side, downstream major consumption sectors such as the flame retardant industry and PV glass industry continued to show mediocre stockpiling sentiment and sluggish buying interest. The main reasons were, on one hand, reduced order volumes due to the relatively sluggish conditions of these industries themselves; more importantly, under the persistent expectation of weak antimony prices, end-user purchases were always made on a hand-to-mouth basis, anticipating further price declines, and a mentality of delaying stockpiling as long as possible prevailed. Meanwhile, speculative forces that were previously active in the market also showed a loss of confidence and temporarily withdrew to the sidelines. On the import and export front, mainly affected by narrowing overseas price spreads, imported antimony ore began to flow into the Chinese market to be monetized quickly. The main import source countries were Southeast Asian nations such as Myanmar and Thailand.

Looking ahead to H2, full-year production is expected to exceed 80,000 mt, up more than 5% YoY. If antimony prices manage to stop falling, stabilize, and rebound in H2, the full-year average price is expected to be around 140,000 yuan/mt. Close attention should be paid to trends in imported antimony ore, demand-side variables, and potential policy changes regarding exports that may impact the market. In addition, if antimony market prices stabilize and rebound, with current prices having returned to the low platform near levels from three years ago, special attention should be given to the impact of speculative stockpiling purchases on antimony market prices.

![Antimony Prices Continue Downward Trend [SMM Antimony Spot Market Weekly Review]](https://imgqn.smm.cn/usercenter/TdoSs20251217171724.jpeg)