SMM News Release, June 22

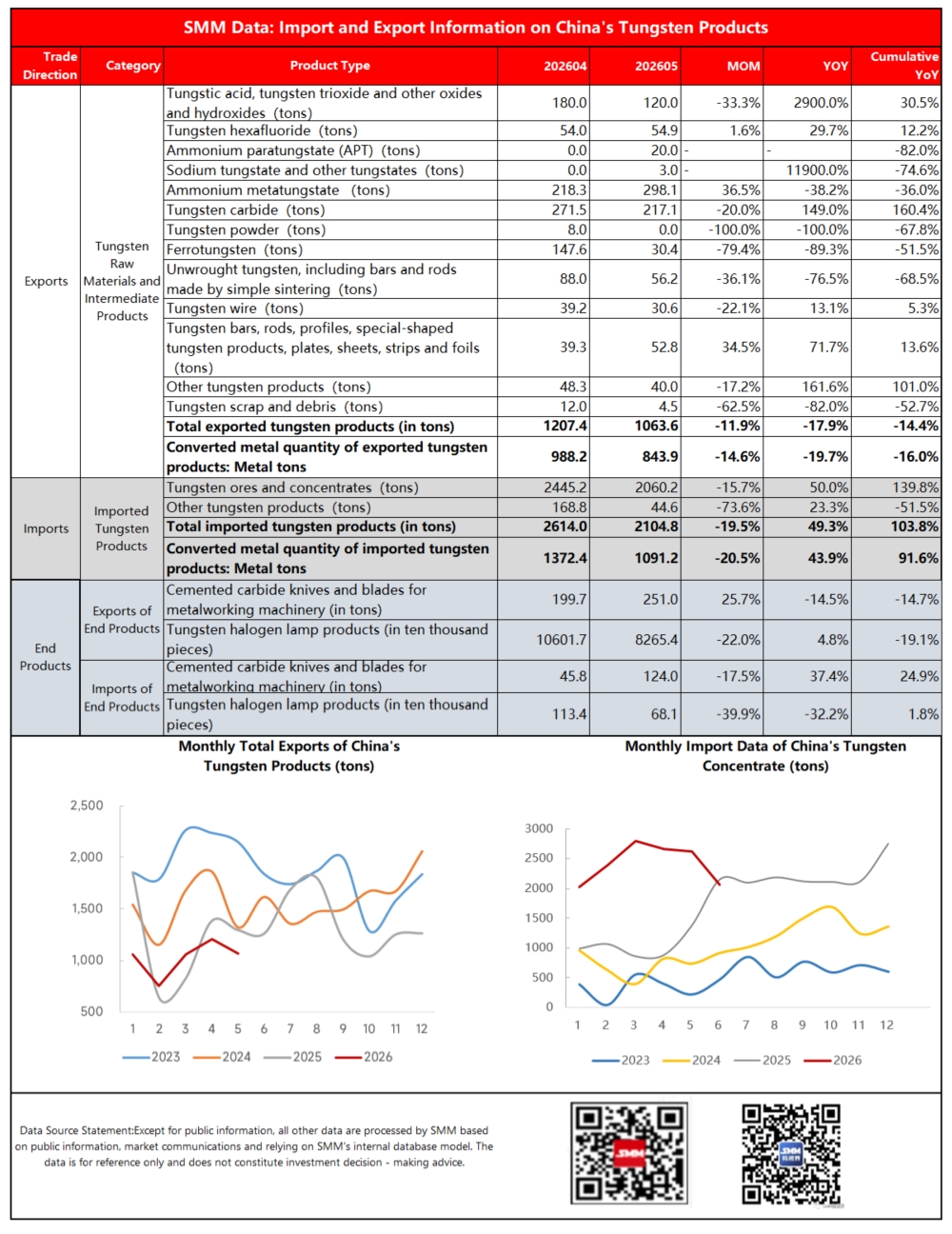

According to customs data, China’s total exports of tungsten smelting products and tungsten materials reached approximately 1,063.6 tons in May 2026, down 11.9% month-on-month and 17.9% year-on-year. Total imports of tungsten concentrates in May stood at around 2,060.2 tons, falling 15.7% month-on-month but surging 50.0% year-on-year. Aggregate imports of all tungsten products totalled roughly 2,104.8 tons, a year-on-year increase of 49.3%.

Calculated on a tungsten metal content basis, China imported 1,091.2 metric tons of tungsten metal in May, up 43.9% year-on-year, while tungsten metal exports totalled 843.9 metric tons, declining 19.7% year-on-year. China posted a net tungsten metal import of 247.3 metric tons in May, compared with a net export of around 293 metric tons in the same period last year.

Since China introduced tungsten export controls in February 2025, coupled with tightened dual-use item regulations targeting Japan effective January 2026, exports of certain domestic tungsten smelting products and tungsten materials have trended downward overall. May exports recorded another year-on-year decline, remaining markedly below pre-control levels. Meanwhile, sustained growth in tungsten ore supplies from Kazakhstan, Myanmar, the DPRK and other sources kept tungsten imports robust in May, forming a market landscape of strong imports, weak exports. Nevertheless, breakdowns of May customs data signal emerging shifts: growth momentum for imported tungsten raw materials may have peaked, while exports could be poised for a recovery.

Import Market Overview

Total tungsten product imports hit 2,104.8 tons in May, down 19.5% month-on-month yet jumping 49.3% year-on-year. Cumulative tungsten product imports over the first five months of 2026 reached 12,930.2 tons, rising 103.8% year-on-year.

Tungsten Ores and Concentrates (2,060.2 tons)

Tungsten ores and concentrates remained the dominant import category, with May volumes climbing 50.0% year-on-year. Total import value of tungsten concentrates in May amounted to USD 90.31 million, translating to an approximate average import price of RMB 309,000 per physical ton. Cumulative imports from January to May 2026 reached 12,350.9 tons, up roughly 140% year-on-year, marking an all-time high expansion. Major sources of May tungsten concentrate imports included Myanmar, Kazakhstan, the DPRK and other regions.

- Myanmar-sourced tungsten concentrates: Imports totalled approximately 880 tons with a total value of USD 31.05 million, equivalent to an untaxed price of around RMB 240,000 per physical ton.

- Kazakhstan-sourced tungsten ores: Imports stood at roughly 550 tons, plunging 47.2% month-on-month. The drop stemmed from annual maintenance at major Kazakh mines that curbed output, with import volumes expected to rebound gradually afterward. May import value for Kazakh tungsten ores reached USD 30.96 million, corresponding to an untaxed unit price of approximately RMB 429,000 per physical ton. Cumulative imports from Kazakhstan over Jan–May 2026 hit 4,295 tons, an increase of 4,121 tons year-on-year, accounting for 35.4% of China’s total tungsten concentrate imports.

Export Market: Raw Materials & Intermediate Products Face Headwinds with Clear Structural Divergence

Total tungsten product exports in May came to 1,063.6 tons, falling 11.9% month-on-month and 17.9% year-on-year, equivalent to 843.9 metric tons of tungsten metal, down 14.6% month-on-month and 19.7% year-on-year. Exports remained on a contractionary track, with cumulative Jan–May exports down 14.4% year-on-year, pointing to persistent export weakness since the start of 2026.

Breakdown by product reveals stark divergences across key varieties:

-

Tungsten Carbide (217.1 tons) Volumes dropped 20.0% month-on-month but surged 149.0% year-on-year. Cumulative 2026 exports reached 1,007 tons, making it China’s top exported processed tungsten product. As a regulated dual-use item, tungsten carbide faces lengthy export approval cycles, with shipments largely fulfilled against orders secured in prior periods. Following a price rebound in China’s tungsten market in June and a surge in overseas inquiries, tungsten carbide exports are projected to post month-on-month growth in June.

-

Ammonium Metatungstate (AMT, 298.1 tons) One of the few products to record month-on-month growth in May, with shipments rising 35.5%, though volumes fell 38.2% year-on-year. Sluggish petroleum industry operations across the Middle East weighed on year-on-year AMT demand. May export prices for AMT averaged USD 255,000 per ton, jumping 660% month-on-month. Amid domestic tungsten export controls and elevated smelting costs, Chinese smelters have strengthened pricing power, keeping export offers firm.

-

Ferrotungsten (30.4 tons) Exports plummeted 79.4% month-on-month and 89.3% year-on-year amid muted demand from Europe’s steel sector, leaving little room for consumption recovery.

-

Tungsten Powder (0 tons) Exports fell to zero in May, representing a 100% decline both month-on-month and year-on-year. The complete export halt may stem from robust domestic demand from China’s powder metallurgy sector absorbing all local output, or potential adjustments to customs declaration categorization standards.

-

Ammonium Paratungstate (APT, 20 tons) After zero exports in April, APT recorded shipments of 20 tons in May under a processing supplied-materials contract bound for Germany. Cumulative Jan–May exports still tumbled 82% year-on-year, reflecting a pronounced shift of domestic APT output toward downstream deep processing such as tungsten carbide, sharply shrinking standalone APT export volumes.

-

Tungsten Bars, Rods, Profiles, Sheets, Strips and Foils (52.8 tons) A rare category posting double growth both month-on-month (+34.5%) and year-on-year (+71.6%). Certain deep-processed tungsten materials maintain solid competitiveness in overseas markets with steady external demand.

China’s export volume threshold for tungsten raw materials and intermediates hit a four-year high at the start of 2026, before sliding markedly in April and May to near multi-year lows, subjecting exporters to substantial pressure.

End Products: Cutting Tool Exports Rise Steadily; Tungsten Lamp Shipments Up with Stable Prices

-

Cemented Carbide Cutting Tools and Blades for Metalworking Machinery (251.0 tons exported) Shipments rose 25.7% month-on-month yet fell 14.5% year-on-year. Persistent wide price spreads between overseas and domestic tungsten prices create upside potential for China’s cemented carbide exports in the long run.

-

Halogen Tungsten Lamps (82.654 million units exported) Volumes declined 22.0% month-on-month but edged up 4.8% year-on-year, with cumulative Jan–May exports hitting 410 million units. The massive shipment scale confirms China’s position as the world’s primary exporter of tungsten lamps.

Import Side for End Products

Imports of cemented carbide blades and halogen tungsten lamps both declined. A 37.4% year-on-year rise in imports of special precision cutting tools underscores lingering reliance on foreign suppliers for high-end variants. However, narrowing overseas price advantages are expected to lift the substitution rate of domestically manufactured cutting tools.

Comprehensive Market Outlook

China’s tungsten trade maintained a strong imports, weak exports pattern in May 2026. Robust import volumes of tungsten concentrates were driven by restocking among domestic processors, signalling strong raw material demand from local downstream manufacturers. Exports, by contrast, remained suppressed by slowing global manufacturing activity, elevated domestic tungsten prices and diminished export cost competitiveness.

Key monitoring factors ahead include:

- The pull effect of recovering global manufacturing PMI on tungsten product exports;

- Potential disruptions to import rhythms stemming from supply stability of tungsten concentrates in Southeast Asia;

- Adjustments to national dual-use item export policies impacting tungsten-related product shipments.

On June 22, the Ministry of Commerce issued Announcement No. 23 of 2026, adding 10 U.S. military-linked entities including Aveox, Red Cat Holdings, Tier 1 Unmanned, Ball Aerospace, Oshkosh Defense, L3Harris Maritime, MP Materials and USA Rare Earth to its export control list, banning shipments of dual-use items to these entities with immediate effect. As tungsten is classified as a strategic resource covered under dual-use item regulations, export channels to the U.S. have further narrowed.

In the short term, the new ruling reinforces expectations of further tungsten export contraction, with direct U.S. exports of tungsten carbide, tungsten powder and other military-relevant varieties likely to drop to zero. Customs data show China exported roughly 472 tons of tungsten intermediates to the U.S. from January to May, mostly ammonium metatungstate, which is temporarily exempt from the dual-use item controls. Marginal changes in this segment require ongoing tracking.

Over the medium to long term, China’s tungsten export controls are set to remain tight. Tightening overseas tungsten raw material supplies will keep international tungsten prices elevated and volatile, sustaining wide cross-border price differentials. This dynamic is projected to boost export volumes of China’s finished tungsten end products over the long run.