I. Market Review of the First Half

Supply Side: Lower Year-on-Year Operating Rates, Extended Spring Festival Holiday Restricting Capacity Output

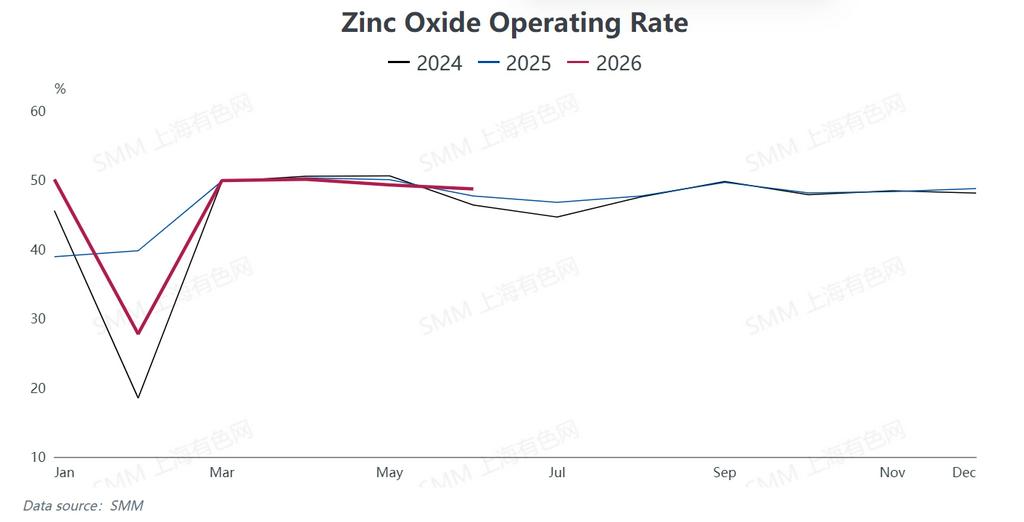

The overall supply of the zinc oxide industry in H1 2026 was characterized by "shrinking output and weak operating rates". Zinc prices surged far beyond expectations around the Spring Festival, prompting downstream end-users to stay on the sidelines due to high price concerns. The average industry holiday break lasted 21.35 days, 1.25 days longer than the same period last year, curbing capacity release at the start of the year.

Post-holiday production resumption lagged. The industry operating rate rebounded briefly to above 50.43% in March. The second quarter marked the traditional off-season for consumption. Coupled with sustained high raw material costs squeezing production margins, the operating rate edged down from 49.95% in April to 47.96% in June.

Overall, the industry operating rate in H1 followed a trajectory of "a slump amid the Spring Festival period, a temporary recovery after the holiday, and another decline in the off-season". The average operating rate for the first half dipped 0.11 percentage points year-on-year.

Demand Side: Uneven Performance of End Markets with Obvious Divergence Among Downstream Segments

The terminal demand for zinc oxide saw prominent structural divergence in the first half of the year amid sluggish overall market trading, with bright spots only emerging in a few niche segments.

Demand for rubber-grade zinc oxide, the core consumption product of the sector, remained under pressure. Domestic automobile production and sales fell year-on-year in H1, while dealer inventory levels climbed simultaneously. In addition, geopolitical conflicts in the Middle East drove up prices of rubber raw materials, leading downstream tire manufacturers to cut purchases, which severely weighed on buying interest for rubber-grade zinc oxide.

Orders for feed-grade zinc oxide stayed weak due to the prolonged downturn in the hog breeding industry. Demand growth for ceramic-grade zinc oxide was limited by the sluggish real estate sector. Only electronic-grade zinc oxide delivered resilient demand, yet its overall market consumption volume was too small to offset the weak demand across the whole industry.

Cost Side: Accumulated Multiple Pressures and Persistent Tight Supply of Raw Materials

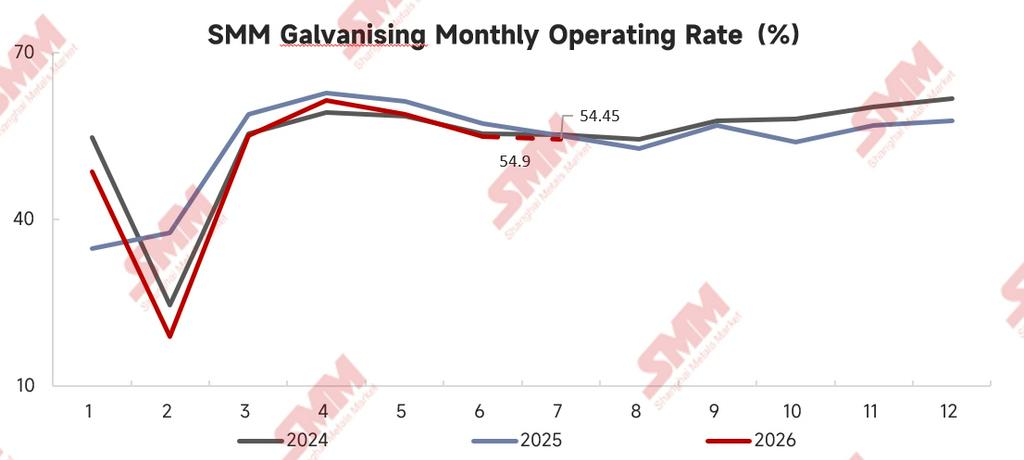

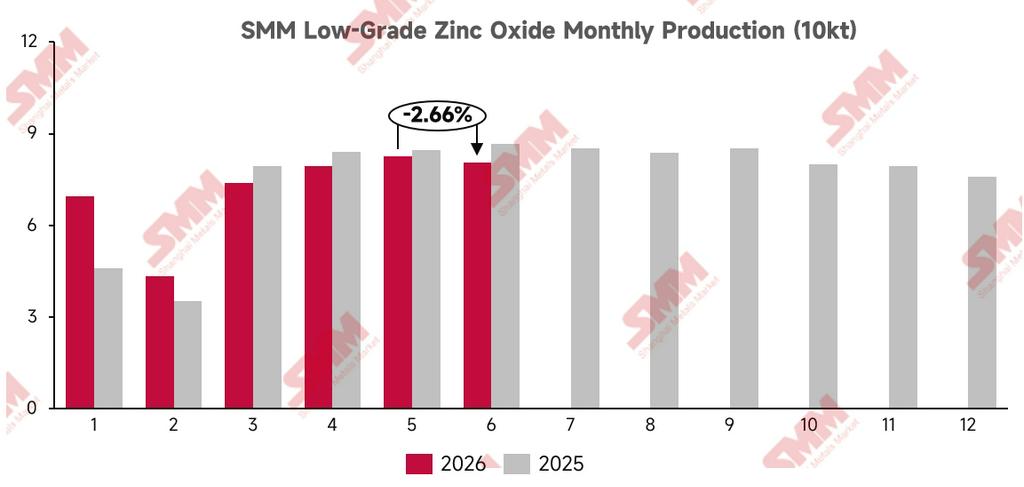

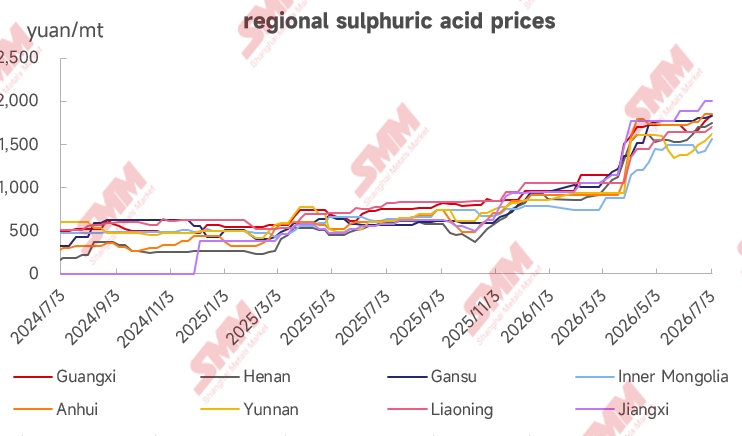

Domestic galvanizing operating rates declined year-on-year in H1, resulting in continuous falling output of secondary zinc oxide. Prices of raw materials and auxiliary supplies including zinc slag, secondary zinc oxide and sulfuric acid rose broadly, pushing up production costs for some zinc oxide manufacturers.

Nevertheless, plagued by industrial overcapacity and tepid end-user demand, product quotations failed to rise in tandem. Producers could not pass cost pressures downstream effectively, squeezing industrial margins continuously.

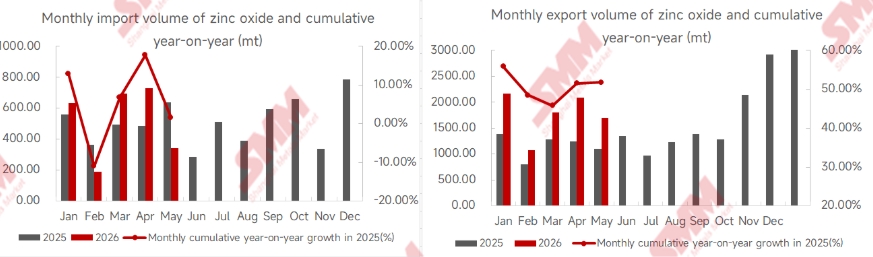

Import & Export: Exports Maintain Robust Growth While Imports Edge Up Slightly

China’s zinc oxide import and export market posted a pattern of "strong exports and moderate imports" in the first half of 2026.

From January to May, cumulative exports of domestic zinc oxide reached 8,831.86 tons, surging 51.82% year-on-year. The sharp export growth was backed by two major factors: first, the low SHFE/LME zinc price ratio rendered domestically produced zinc oxide remarkably price-competitive; second, continuous relocation of downstream industries such as tire manufacturing to Southeast Asia fueled synchronized overseas shipments of supporting zinc oxide products. As a result, overseas exports partially offset the sluggish domestic demand.

On the import front, cumulative imports hit 2,592.66 tons from January to May, edging up by a mild 1.70% year-on-year. At present, China boasts sufficient zinc oxide production capacity while overseas zinc prices stay elevated, which should have curbed import demand for ordinary industrial-grade zinc oxide. The slight uptick in total imports mainly stemmed from reliance on overseas supplies for small volumes of high-purity electronic-grade zinc oxide, pushing the overall import figure marginally higher.

Import & Export: Exports Maintain Robust Growth While Imports Edge Up Slightly

China’s zinc oxide import and export market posted a pattern of "strong exports and moderate imports" in the first half of 2026.

From January to May, cumulative exports of domestic zinc oxide reached 8,831.86 tons, surging 51.82% year-on-year. The sharp export growth was backed by two major factors: first, the low SHFE/LME zinc price ratio rendered domestically produced zinc oxide remarkably price-competitive; second, continuous relocation of downstream industries such as tire manufacturing to Southeast Asia fueled synchronized overseas shipments of supporting zinc oxide products. As a result, overseas exports partially offset the sluggish domestic demand.

On the import front, cumulative imports hit 2,592.66 tons from January to May, edging up by a mild 1.70% year-on-year. At present, China boasts sufficient zinc oxide production capacity while overseas zinc prices stay elevated, which should have curbed import demand for ordinary industrial-grade zinc oxide. The slight uptick in total imports mainly stemmed from reliance on overseas supplies for small volumes of high-purity electronic-grade zinc oxide, pushing the overall import figure marginally higher.

![Guangdong Zinc: Futures Consolidate at Highs, Market Just-in-Time Procurement [SMM Midday Comment]](https://imgqn.smm.cn/usercenter/PEqzX20251217171755.jpg)

![Shanghai Zinc: Zinc futures prices edged down, some traders raised spot zinc offers [SMM Midday Review]](https://imgqn.smm.cn/usercenter/tAyyp20251217171754.jpg)