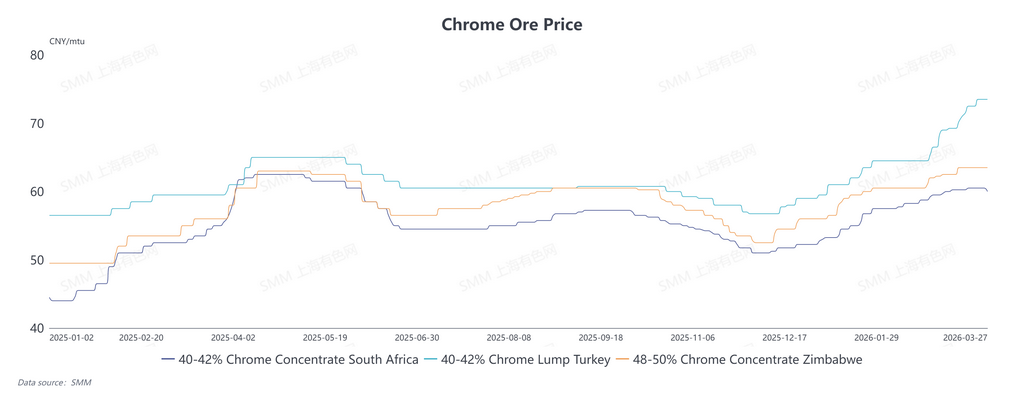

1. Divergence Between Futures and Spot Prices

In the spot market, high-priced long-term contracted cargoes arrived at ports in the early stage with high cargo receiving costs. Domestic traders showed a strong willingness to prop up prices, driving continuous hikes in chromite quotations. However, downstream demand remained sluggish. Coupled with persistently high shipments and a notable inventory build-up, selling pressure intensified, slowing the upward momentum of spot chromite prices.

Current quotations at Tianjin Port:

- 40-42% South African chromite fine: 59.5 - 60.5 RMB per dry metric ton unit

- 40-42% Turkish chromite lumpy ore: 73 - 75 RMB per dry metric ton unit

- 48-50% Zimbabwean chromite fine: 63 - 64 RMB per dry metric ton unit

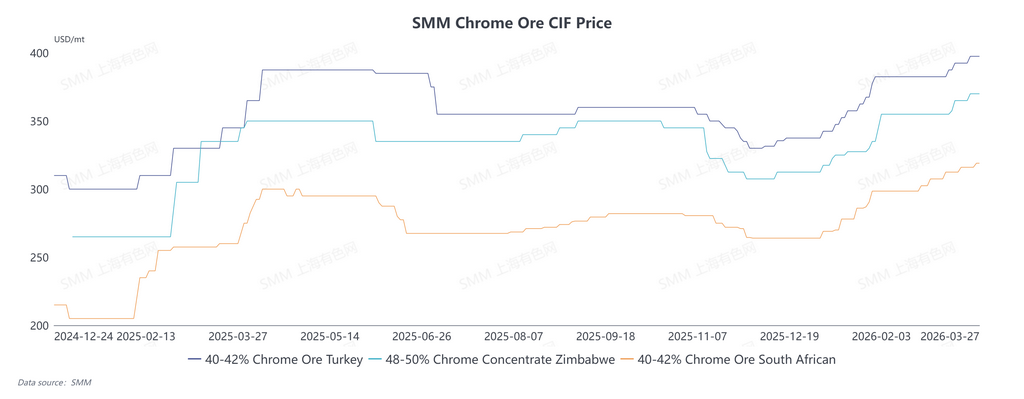

In the futures market, geopolitical conflicts in the Middle East pushed up fuel prices and sharply increased ocean freight costs, underpinning continuous rises in overseas chromite quotations.

- South African chromite fine: risen to 318 USD/ton

- Zimbabwean chromite fine: stable at 375 USD/ton

- Turkish chromite fine: breaking through 400 USD/ton

With costs staying at elevated levels, overseas chromite prices are expected to maintain a firm trend in the short term.

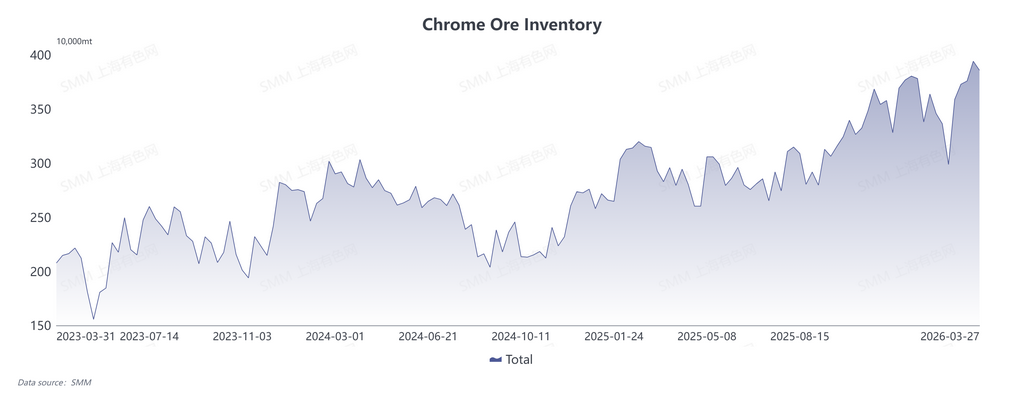

2. Sustained High Shipments

According to SMM statistics, as of March 28, global bulk chromite shipments reached 2.2577 million tons, and the estimated port arrivals stood at 1.772 million tons, a month-on-month increase of 17.59%.

Overall global chromite shipments have not declined significantly, maintaining a high and stable level. The rising arrivals have directly driven up port inventories of chromite. SMM data showed national chromite port inventories totaled 3.8583 million tons this week, including 3.075 million tons at Tianjin Port.

Overall, the average chromite inventory in March was 3.8218 million tons, up 15.33% month-on-month. Post-holiday chromite inventories have climbed to a multi-year historical high. Meanwhile, ferrochrome tender procurement fell short of market expectations, weakening market sentiment, and putting downward pressure on chromite offers.

3. Insufficient Downstream Demand

Recently, major steel mills announced that the April procurement tender price of high-carbon ferrochrome would be raised by 150 RMB per 50-base ton, yet the increase was lower than anticipated, squeezing profit margins.

Rising chromite prices have substantially lifted production costs, exposing ferrochrome producers to the risk of cost inversion and losses. Most manufacturers plan equipment maintenance and production cuts, which is expected to weaken their procurement demand for chromite going forward.

In addition, ferrochrome producers built sufficient raw material inventories before the holiday. They are mainly consuming existing stocks currently, with sluggish inquiry and procurement activity. Transactions are limited to small-volume rigid demand, curbing further gains in chromite prices.