Shanghai Metals Market (SMM) is thrilled to announce that we will hold the 2026 SMM ASEAN Ferrous Metals Summit from November 26-27, 2026 in Kuala Lumpur, Malaysia. This event is the premium platform in the ASEAN ferrous metals market that converge 400+ decision-makers from mines, mills, trading houses, processors, equipment and technology providers, and logistics operators at the same table — precisely when the regional order is being rewritten.

The ASEAN steel industry is undergoing profound transformation, driven by strong demand growth, capacity expansion, shifting trade flows, and increasingly complex trade policies. Steel apparent consumption across the six major ASEAN economies exceeded 81 million tonnes in 2024 and is projected to reach 87.9 million tonnes in 2026, up 2.6% from 2025 and 8.2% from 2024. Vietnam was the region’s fastestgrowing market in 2024, expanding by over 21%, while Vietnam, Indonesia, and the Philippines are expected to lead incremental demand in 2026.

Demand continues to expand. In 2024, apparent steel consumption in the six major ASEAN economies exceeded 81 million mt, and is expected to reach 87.9 million mt by 2026. Vietnam posted over 21% growth in 2024 and will lead regional growth.

Capacity is expanding rapidly. In 2025, ASEAN crude steel production surpassed 60 million mt and is forecast to reach 90.6 million mt by 2030, making it the fastest-growing region globally. However, the import penetration rate remains above 60%, and steel imports rose by 5 million mt in 2025. The capacity structure is undergoing profound transformation: the BF-BOF share rose from 6% in 2011 to 30% in 2020, Indonesia and Vietnam jointly control 74% of crude steel production, and Chinese steelmakers’ overseas investments are mainly concentrated in these two countries.

Trade flows are being reshaped. In 2024, China exported 28.219 million mt of steel to ASEAN, up 29.3% YoY; in H1 2025, steel billet exports surged to 5.89 million mt, up 300.3% YoY. In March 2026, Vietnam suspended slab exports, and the ASEAN supply gap is estimated at 2.3 million mt. Price stratification has emerged: Vietnam became the regional low-price zone ($482/mt), Japan and South Korea dominate the high-end market, Malaysia recorded a cumulative 78.9% increase over three years, absorbing spillover demand, while Indonesia’s average price bucked the trend, rising to $522/mt, with imports clearly focusing on high-end products.

Expanded supply and demand, capacity iteration, trade restructuring, and price spread divergence—multiple variables are intertwining. The industry urgently needs a high-level dialogue platform to identify pain points and uncover business opportunities.

Conference Highlights

1. ASEAN Steel Market Outlook

An in-depth analysis of regional steel demand, with consumption expected to reach 87.9 million mt in 2026, driven primarily by Vietnam, Indonesia, and the Philippines.

2. China—ASEAN Trade and Supply Chain Restructuring

Exploring shifting flows of HRC, billet, slab, and other steel products amid changing supply patterns, trade remedies, and regional market dynamics.

3. Capacity Expansion and Production Transition

Examining ASEAN’s evolving steelmaking landscape, including BF-BOF capacity growth, EAF development, overseas investment, and new regional production hubs.

4. Trade Policies and Market Access

Assessing anti-dumping measures, tariffs, RCEP-related opportunities, and regulatory changes reshaping steel trade across ASEAN.

5. High-Growth Demand and Product Opportunities

Identifying opportunities from infrastructure, construction, automotive, and advanced steel applications, with a focus on Indonesia, Vietnam, and other emerging markets.

6. Executive Networking and Regional Cooperation

Connecting leading producers, traders, buyers, investors, associations, policymakers, and industry experts across ASEAN, China, and global markets.

Scenes from Past Conferences

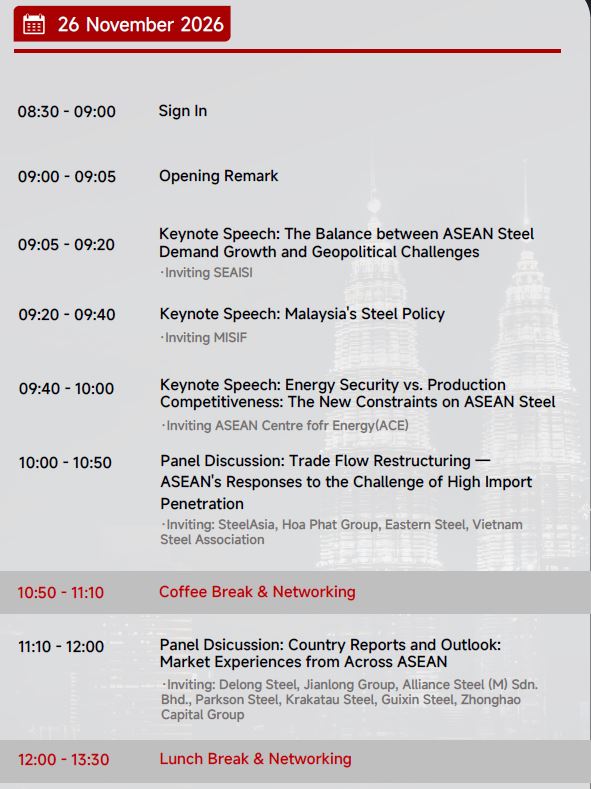

Conference Agenda

Companies to Be Invited

The companies we will invite for this conference cover various segments of the ferrous metals value chain, indluding

- Steel Mills/Smelters (42)

- Trader / Steel Processing & Trading(12)

- Metallurgical Equipment / Engineering Technology(5)

- Refractory Materials / Auxiliary Materials(2)

- Electrodes / Carbon Products(3)

- Associations / Institutions(9)

- International(1)

- Technology / Digitalization(6)

- Digital Platform / Green Steel(1)

- Carbon Trading / Green Finance(1)

- Consulting(1)

- Investment / Finance(1)

- Downstream Steel Application(3)

- Engineering Construction(1)

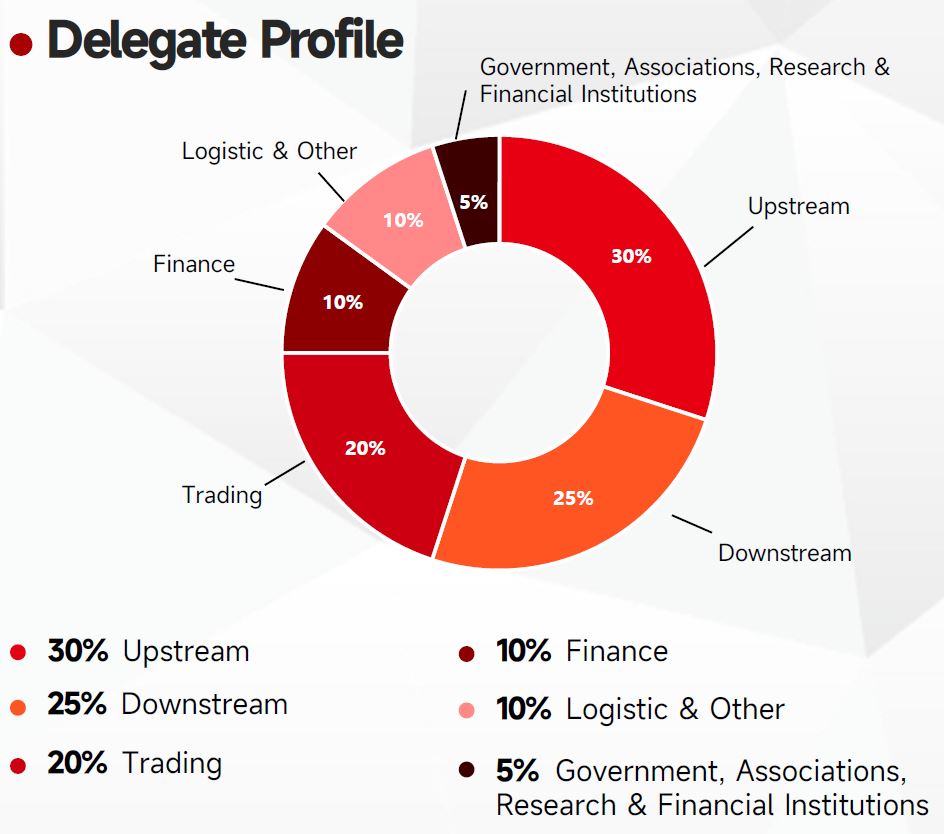

Composition Structure

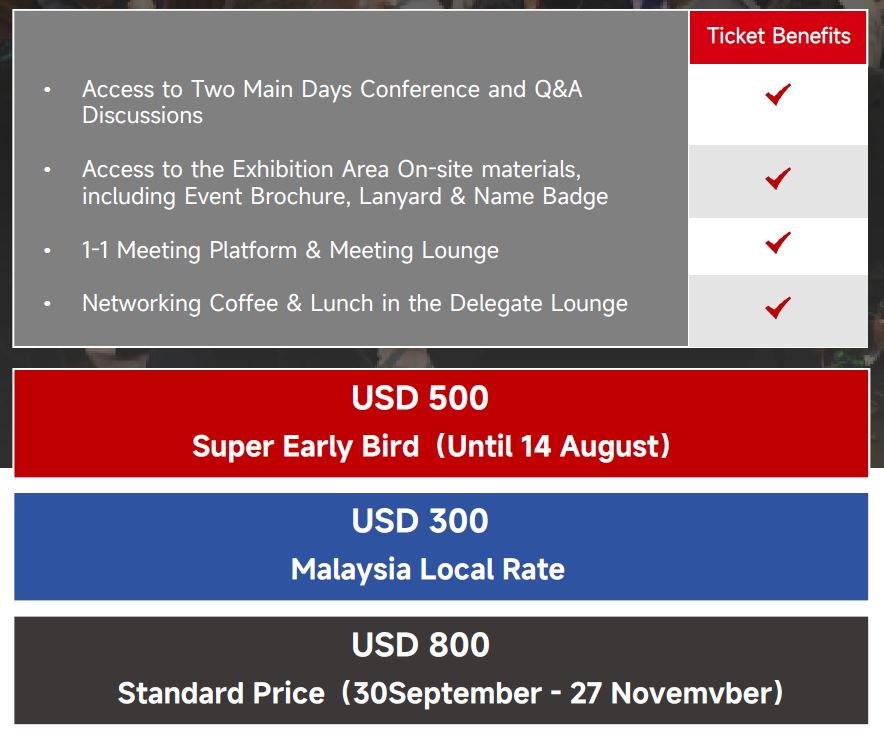

Ticket Prices

Contact: Horin Dong

WhatsApp: +8618721310824

Email: horindong@smm.cn

Scan the QR code for conference details and more discount information

![[POSCO, KB Kookmin Bank Launch Supply Chain Finance Service]](https://imgqn.smm.cn/usercenter/zbJUC20251217171718.jpg)

![[SMM Steel] Vietnam HRC Prices Ease as Buyer Bids Stay Low](https://imgqn.smm.cn/usercenter/exdqc20251217171717.jpg)

![[SMM Steel] India Alang Ship-Breaking Scrap Holds Stable on Tight Supply](https://imgqn.smm.cn/usercenter/GGaSo20251217171716.jpg)